Bond Traders Learn Taco Bell Isn’t a Bellwether

(Bloomberg Opinion) -- Every once in a while, a single anecdotal data point captures the hearts and minds of bond traders. Often, it confirms their beliefs about the direction of the economy.

It seems one such data point was a report this week that Taco Bell, the fast-food chain that sells double-stacked tacos for $1, would soon be offering a $100,000 salary for some restaurant managers. It was interpreted as a sign that Federal Reserve officials might be wrong to think that the U.S. labor market still had ample slack and an early indication that wage growth would at long last meaningfully increase broadly across America. This, of course, would conform with mounting bets that inflation will rise faster than expected in 2020.

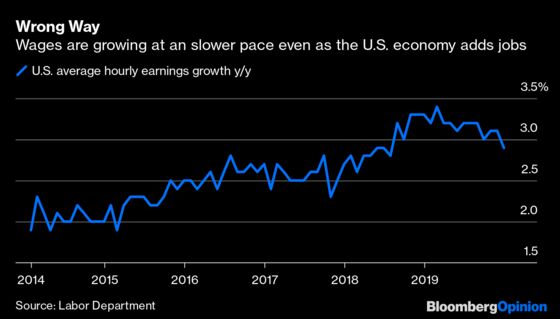

The December jobs report quickly threw cold water on that notion. Payrolls rose by a respectable 145,000, slightly missing estimates for a 160,000 gain, while the unemployment rate held steady at 3.5%. But wage growth fell far short of analysts’ expectations, with average hourly earnings increasing by just 2.9% from a year ago. It was the first reading below 3% since July 2018, and even wages for the average worker weakened.

“We’ve hired 21 million people since 2010 — how are we not lifting wages to bring people into the labor force?” Rick Rieder, BlackRock Inc.’s chief investment officer of global fixed income, asked on Bloomberg TV. On the same panel, my fellow Bloomberg Opinion columnist Mohamed El-Erian called slowing hourly earnings growth “the great puzzle.” Given how many jobs the U.S. added in the past year, in the longest economic expansion ever, “you’d think wages should be going up by more than 3%.”

Now, this conundrum is hardly new to this jobs report. The lack of meaningfully higher wage growth has long vexed economists, traders and Fed officials alike. But the feeling throughout markets seems to have been that the economy had finally turned a corner for a number of reasons. The U.S. and China had reached a preliminary trade deal, the Fed moved quickly to ease policy, and officials sent a clear signal that they would tolerate higher inflation.

Just this week on a webcast, DoubleLine Capital Chief Investment Officer Jeffrey Gundlach drew attention to the growth in average hourly earnings. It “is starting to look like a trend,” he said, and posited that a breakout above 4% was possible.

To be sure, every month’s data has quirks. In this report, for instance, Tom Simons at Jefferies LLC noted that manufacturing payrolls were the main source of weakness, falling by 12,000 compared with the estimate of a 5,000 gain. That “probably put some downward pressure on the wage data as well, as these jobs tend to be pretty high-paying,” he said in a report. But the industry should get a boost in the coming months after the U.S.-China trade deal is signed. BlackRock’s Rieder pointed to a late Thanksgiving Day holiday in the U.S. as historically leading to strong November data at the expense of December.

For now, though, bond traders have to take the report at face value. That’s why 10-year Treasury yields are lower and the yield curve has flattened after reaching its steepest level since October 2018. The “inflation is coming” narrative took a hit Friday, as pressure abates from the so-called cost-push side (when prices go up because it costs more to produce goods or deliver services). And yet there’s nothing to suggest a significant change in the economic outlook, so the Fed won’t budge anytime soon.

The 2020 inflationistas probably wish that all employers in the U.S. were a bit more like Taco Bell. It looks as if they’ll have to settle in for a longer slog.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.