Our Huge Wireless Merger Won't Cost You. We Promise.

(Bloomberg Opinion) -- T-Mobile US Inc. and Sprint Corp. are in court dueling with a group of state attorneys general over whether their merger will be harmful to consumers, even though it shouldn’t even be a debate. In what possible scenario would removing a low-cost rival from an already highly concentrated industry not have a negative effect on competition?

The wireless carriers are contorting themselves into a pretzel trying to make the illogical argument that their merger will instead benefit customers — and somehow it’s working. Antitrust authorities appointed by President Donald Trump accepted this rationale with a straight face: The U.S. Federal Communications Commission, led by Ajit Pai, and the antitrust division of the Department of Justice, led by Makan Delrahim, each gave its blessing to the deal in recent months on the condition that the two companies make some painless concessions. Now, in a last line of legal defense and an unusual turn for such transactions, the matter is being tried in a case brought by plaintiffs Letitia James of New York and 13 other attorneys general. They are arguing that the remedies don’t go far enough to address the antitrust violations. They don’t, and yet there’s no telling which way this trial will go.

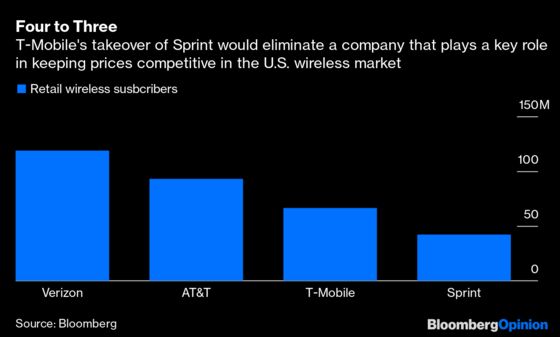

Competition between T-Mobile and Sprint during the last few years resulted in lower plan prices for wireless customers, even putting pressure on industry leaders Verizon Communications Inc. and AT&T Inc. It’s how unlimited data offerings came about. Without Sprint in the mix, this healthy competitive spirit is diminished. No acrobatics of economic modeling can camouflage this fact, and still the facts are in dispute. How very 2019.

Text messages from 2017 between Roger Sole, Sprint’s head of marketing, and its then-CEO Marcelo Claure (who is now executive chairman) were revealed on Monday, the first day of the trial. As the two companies were negotiating the deal, Sole wrote to Claure that the combined entity could generate $5 more from each subscriber per month, and that the consolidation would even provide a boon to AT&T and Verizon. Sole may have been just spit-balling, and the state attorneys have a stronger case than to put too much stock in some gotcha private texts. Still, the conversation strongly suggests that greater pricing power was absolutely a motivation for the transaction, and it’s naive of anyone to think otherwise.

T-Mobile and Sprint have agreed not to raise prices for three years, which is the blink of an eye in the business world and further demonstrates that the company’s goal is to eventually do so. Three years also conveniently brings the company to the point at which there may be little room left for cost-cutting, and so it will need to look to other ways to boost growth and margins. That’s if there aren’t loopholes in the agreement that it can exploit sooner. As well-liked as the gregarious T-Mobile CEO John Legere is — and as admirable as his track record is in fostering industry innovation — his personal promise that the company won’t take advantage of newfound pricing power should carry little weight. He won’t even be there to see it through.

There are other business benefits beyond the ability to raise prices. For one, Sprint is a financially challenged company with a tarnished brand that is struggling to compete against its larger rivals. Selling to T-Mobile, which is on far healthier footing, would be good news for frustrated shareholders, such as Masayoshi Son of SoftBank Group Corp., the Japanese conglomerate that controls Sprint. The companies would also get to combine their spectrum assets and join forces on building a nationwide 5G wireless network.

The U.S. needs to be competitive in 5G, but waving the American flag and trying to put the fear of China into regulators isn’t a legitimate defense against antitrust enforcement. Plus, it’s hard to see how blocking the merger would set the nation back — both companies are investing in 5G regardless. As for the notion that T-Mobile is preserving competition by rescuing Sprint before it potentially goes belly-up, it just doesn’t hold water because other bidders are probably out there. While companies like Comcast Corp. and Charter Communications Inc. may be seen as the Big Bad Cable Guys, either one owning Sprint would still maintain a four-carrier market, whereas T-Mobile’s deal wouldn’t.

One of the remedies sought by the DOJ was to allow satellite-TV provider Dish Network Corp. access to the T-Mobile network while Dish builds its own. But Dish is a long, long ways from ever replacing Sprint. The DOJ’s lax stance on this deal would also seem to contradict the concerns it recently raised about anti-competitive business practices in the tech world, where immense market power is wielded by so few players.

In the book “The Myth of Capitalism: Monopolies and the Death of Competition,” Jonathan Tepper and Denise Hearn make the case that the U.S. has an oligopoly problem — that is, industries have become too concentrated to the detriment of consumers and workers, in large thanks to anti-competitive mergers. My colleague John Authers, who runs the Bloomberg book club, and I will be discussing this with the authors in a live chat on Wednesday at 11 a.m. New York time. It’s a timely conversation as the T-Mobile-Sprint situation plays out. Terminal subscribers can join us at TLIV and send comments or questions to authersnotes@bloomberg.net.

There’s more to come in the trials and tribulations of Sprint’s unending quest to merge with T-Mobile. But whatever headlines emerge from the courtroom, this fact won’t change: A merger means market power will be concentrated in fewer hands.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering the business of entertainment and telecommunications, as well as broader deals. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.