Central Banks Should Build Post-SWIFT Highways

Even without the war in Ukraine, correspondent banking using the SWIFT messaging system was going downhill.

(Bloomberg Opinion) -- Even without the war in Ukraine, correspondent banking using the SWIFT messaging system was going downhill. By cutting off some Russian lenders’ access to the communication channel, politicians have put central banks on notice. They need to find a safer alternative for companies and individuals to send funds across borders.

Monetary authorities know that the status quo is riddled with high fees and uneven speed, ranging from less than five minutes on the fastest routes to more than two days on several of the slowest, according to a recent study of SWIFT’s new global payments standard. But the threat of being suddenly unplugged from the network poses a much bigger problem: Russian-style financial instability. To deal with it, central banks need to come together and forge an alternative digital-money expressway.

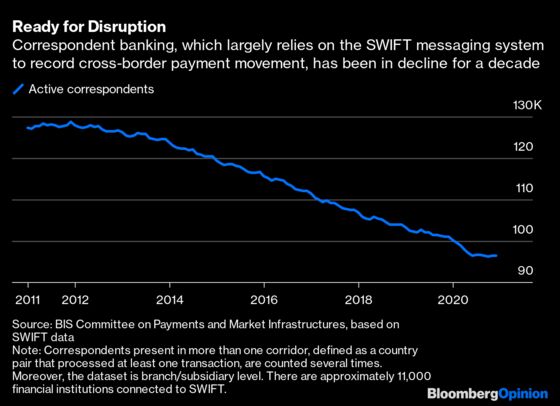

Correspondent banking, in which a lender provides a local account to banks based overseas, goes back to the late 1800s. In 1935, there were 4,000 banks offering the service, with 80% of them concentrated in the U.K. and the U.S. — which wasn’t surprising, given the role of London and New York as money centers. Nowadays, approximately 11,000 institutions use SWIFT, which went live in 1977 and replaced the Telex. But active correspondent relationships have declined by roughly 25% over the last decade. Banks have exited unprofitable payment corridors.

China can potentially move away from correspondent banking — and the SWIFT network — by letting its buyers and sellers pay and receive digital yuan, or the e-CNY. While such a unilateral approach might work for the world’s second-largest economy, the best bet for smaller nations may still be cooperation. Like-minded trading partners could form an international platform for cross-border payments and settlements.

Suppose a Malaysian bank on this platform needs to pay Australian dollars on behalf of a customer, but it doesn’t have an account at the Reserve Bank of Australia to debit. This is a situation where a correspondent bank in Australia would typically step in. However, it’s entirely possible for Singapore’s DBS Group Holdings Ltd., which does have a branch in Sydney and is sharing the same common platform, to give the Malaysian lender a tokenized version of Australian dollars, in exchange for a digital representation of the ringgit.

Putting multiple central bank digital currencies, or CBDCs, on a single system can dispense with time-consuming messaging and complete cross-border payments in real time. This isn’t just a theoretical construct. The monetary authorities of Singapore, Malaysia, Australia and South Africa have come together to successfully test prototypes of such a common platform under the Bank for International Settlements’ Project Dunbar.

Most of the delays currently occur after the beneficiary bank has received the payment instruction and before it credits the end-user’s account, according to Thomas Nilsson at the secretariat for the BIS Committee on Payments and Market Infrastructures and other researchers. Sending money to lower- and middle-income economies is especially slow and expensive because of batch processing and extra compliance related to capital controls. But these are exactly the countries that export their surplus labor to the world and can’t afford to lose 6.3% on a $200 inward remittance. (And that’s just the average; fees can be much higher.)

The CBDCs that are issued on a cross-country platform need not be available to the general public for use in the domestic economy. These tokens could remain purely wholesale, existing in the wallets of financial institutions. The important thing is to think creatively and eliminate the prolonged processing times at the beneficiary banks — or make the delay irrelevant.

Richard G. Brown, the U.K.-based chief technology officer at R3, whose Corda blockchain sandbox is being used to test Project Dunbar, calls it the “check is in the post” problem. How does the buyer convince the seller in another country that it has actually paid? The latter can’t see the money in its account, and may not believe the buyer if it produces a confirmation from its own bank: “It’s just a message. I could have faked it.”

But what if the message the buyer got from its bank was digitally signed by the seller’s central bank — a trusted institution — to say that “not only did the transfer happen but I promise that it happened?” Brown asks. This message can then be relayed to the seller’s back-office, so that it automatically updates its records, removing a source of perennial friction from global trade.

The common expressway on which many central banks will put their wholesale digital money in motion is not yet a reality. We don’t know how many may eventually take shape; and who’ll own them. But one thing is clear. The SWIFT-related sanctions against Russian banks could just be the trigger that finally retires correspondent banking and puts it in a money museum. Payments that take days to conclude have no place in 21st-century trade and finance.

More From This Writer and Others at Bloomberg Opinion:

-

China Can Bypass SWIFT by Going Digital: Andy Mukherjee

-

West Uses Russia’s Central Bank Against Putin: Timothy O'Brien

- Market's Plumbing Bends But Doesn't Break – Yet: Robert Burgess

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2022 Bloomberg L.P.