Swedish Buyout Giant EQT Wants a Blackstone Valuation

(Bloomberg Opinion) -- The stock market is getting an initial public offering of a major buyout firm after a long drought. EQT AB’s listing in Stockholm has genuine scarcity value, but a desired valuation above that of American peer Blackstone Group Inc. demands a leap of faith.

EQT has taken many portfolio companies public in its 25-year life, and it knows a recent history of profitable growth helps. The Swedish firm has certainly enjoyed a big expansion lately. It has raised 34 billion euros ($38 billion) from investment clients since the beginning of 2015, 80% more than it amassed over the preceding 20 years. Half of EQT’s 40 billion euros of assets under management are in just two funds raised in 2018 and earlier this year.

This distorts its current financial performance. Private equity firms get their revenue from management charges levied on the funds they’ve raised, and later from performance fees when their investments do well. EQT’s cash-gathering spurt means its income is now dominated by management fees of almost 500 million euros over the past 12 months. That’s more than twice their 2016 level.

There’s more to come. A jumbo EQT infrastructure fund that closed in March will make a bigger contribution to revenue in 2020. The firm will soon be ready to do another big round of fundraising. Assume this is between 10 billion euros and 15 billion euros and, with an average management levy of about 1.4%, it could add as much as 210 million euros to annual fee income.

But management fees are a function of how much money a firm can raise; performance fees show how effective it is at using those funds. EQT aims broadly to double clients’ money and has done so in the past. If it can do that on the sums amassed in the last four years, shareholders’ slice of the performance fees could be more than 2 billion euros over time.

Suppose EQT closes another big fund sometime in 2020 and performance fees tick up slightly. Revenue could then be roughly 700 million euros next year. With a 50% operating margin and 12% tax rate, earnings would be about 310 million euros. The narrow IPO market capitalization range of 5.5 billion euros to 6 billion euros is on that basis 18 to 19 times next full-year earnings.

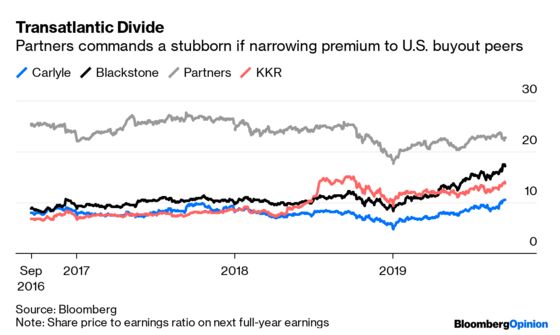

That valuation is a big discount to Swiss peer Partners Group Holding AG, which is warranted given Partners is more diversified, with many small funds invested globally and a 13-year track record on the public markets. EQT is concentrated by fund, strategy and geography.

Still, the valuation is a premium to U.S. peers Carlyle Group LP, KKR & Co. and Blackstone, which trade between 11 and 17 times. After a couple more jumbo fundraisings, EQT would actually look cheap. But IPO investors should bear in mind that sustained fundraising success would depend largely on investment performance being delivered — and EQT proving it can replicate its historic returns doing far bigger buyouts than before.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.