(Bloomberg Opinion) -- Of the many economic reports that the U.S. government puts out each month, the one looking at the number of homes on which builders have started construction doesn’t come close to matching the interest of investors, economists and politicians like those that dive into how many jobs employers have added or how fast consumer prices are rising. Maybe that should change.

The Commerce Department said Thursday that so-called residential starts jumped 11.8% in November to 1.68 million at an annualized rate. The increase was the biggest in eight months, which is good given the massive shortage of housing. The National Association of Realtors says it would only take about 2.4 months for the inventory of homes on the market to be depleted given current sales rates, a record low and far below the historical average of 5.6 months. Heading into the last housing crisis in 2008, the figure was around 10 months.

But the most promising news came well below the headline figures. There, you’ll find that 752,000 single-family homes are under construction, the most since 2007. Better still, 734,000 multifamily dwellings — defined as housing containing at least two units — are under development, the most since July 1974.

The reason this is important is because of the increasing role the rising cost of housing and surging rents are playing in the current high rates of inflation, which is the single biggest story of the economy right now. So much so that the Federal Reserve said this week that it no longer views the recent spike in inflation as “transitory” and that it expects to raise interest rates three times next year. In September, the central bank was anticipating perhaps one rate increase in 2022.

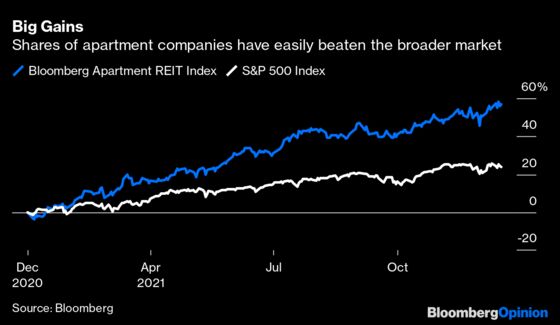

Evidence that builders are rushing to meet demand should help to temper the big gains not just in housing prices but in apartment rents as well. Real estate services firm Redfin Corp. said in late November that the average increase in monthly rents nationwide was 13%, with some areas such as southeast Florida and the New York City metro area experiencing gains of more than 30%. To understand just how unusual these gains are, just look at the performance of apartment companies. The Bloomberg Apartment REIT Index has soared 56% this year, the most since the measure was created in 1994 and about double the 23.3% gain in the S&P 500 Index.

It’s important to understand how housing costs filter into inflation. They show up in the government’s consumer price index report through a measure called owners’ equivalent rent, or OER, which accounts for a disproportionately large 24% of the headline inflation number — 6.8% in November — and 30% of the core reading — 4.9% — that strips out food and energy. The OER figure attracts a lot of criticism, with many saying it underreports housing costs. Officials basically survey homeowners and ask them “how much would your house rent for?” and then track the responses over time. The reading for November came in at an increase of 3.5%, which is the most since the surge in late 2016 but far less than the rental numbers reported by Redfin or the 19% jump in housing prices over the last year.

Nevertheless, it’s the speed of inflation that matters to markets, economists and politicians, not whether a key measure is 100% accurate or not. Which brings us back to multifamily housing starts. Given the nature of construction, with apartment complexes taking about a year to complete, the coming flood of new supply won’t arrive overnight. But we may start seeing the benefits — a more normal environment for housing costs that doesn’t add much to inflation — by mid-2022, judging by when the surge in construction started.

There is one bit of irony in all this, which is that the Fed is talking about tightening credit to contain inflation when the biggest contributor to inflation is housing costs. Perhaps policy makers would be wrong to do anything that raises the cost of capital to developers so they can continue to deliver a much-needed supply of housing as soon as possible.

More From Other Writers at Bloomberg Opinion:

- Adding in Inflation, 2021 Ends Much as 2020 Began: John Authers

- Fed Makes a Welcome Pivot But Has More to Do: Mohamed El-Erian

- Does Inflation Hurt the Poor More Than the Rich?: Tyler Cowen

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the executive editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.