Student-Loan Relief Loses Momentum in Hot U.S. Economy

(Bloomberg Opinion) -- Get ready to hear about Americans’ $1.58 trillion of student loans again.

The huge debt pile has long been a political flashpoint, with Democratic presidential hopefuls in 2020 such as Elizabeth Warren and Bernie Sanders calling for canceling the federal loans to ease the burden on younger workers. That hasn’t happened, but since March 2020, the U.S. government has cut interest rates to 0% and suspended payments and collections on defaulted debt. For millions of Americans, it has been a tremendous relief.

This emergency measure was supposed to expire on Sept. 30 but was ultimately extended until Jan. 31. Some Democrats, well aware of the political ramifications, are again calling to keep the freeze in place for longer, with Senate Majority Leader Chuck Schumer bemoaning that “horrendous interest will pile up at a time when too many are still not financially prepared to shoulder a giant monthly bill.” But with the U.S. economy in the midst of an outright boom, the arguments for “at least” one more extension are losing momentum. As unpopular as it may be, expect student-loan payments to resume soon.

Schumer’s reference point was a survey last month from the Student Debt Crisis Center, an advocacy group, and Savi, a startup that helps borrowers cut their payments. The top-line takeaway: “89% of full-time employed student loan borrowers say they’re not financially secure enough to begin making payments.” That sounds ominous, but it looks subject to selection bias: The survey was based on 33,703 responses from a group of about 2 million Student Debt Crisis Center followers.

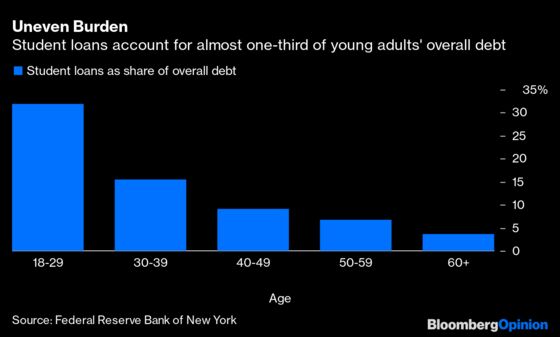

Broader economic indicators tell a more optimistic story. The student-loan burden disproportionately falls on 18- to 29-year-olds, according to Federal Reserve Bank of New York data. They have about $350 billion of the loans, or almost one-third of their overall debt. Those ages 30 to 39 have more in nominal terms, at about $510 billion, but that’s just 15.4% of their total debt because of a pickup in mortgages among that cohort.

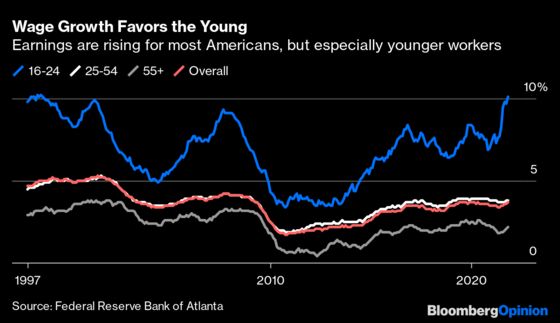

It’s these younger Americans who are benefiting from a tight labor market. According to the Atlanta Fed’s wage growth tracker, earnings for those 16 to 24 jumped 10.1% year-over-year in November, nearly matching the most on record and much higher than the broader 3.7% increase. Meanwhile, the unemployment rate for 25- to 34-year-olds has plunged in the past few months, from 6.5% in June to just 4.2% in November, a sharper drop over the period than the jobless rate for the 35 to 44, 45 to 54 or the 55-and-older cohorts. It took until early 2018 to reach such a level after the 2008 financial crisis.

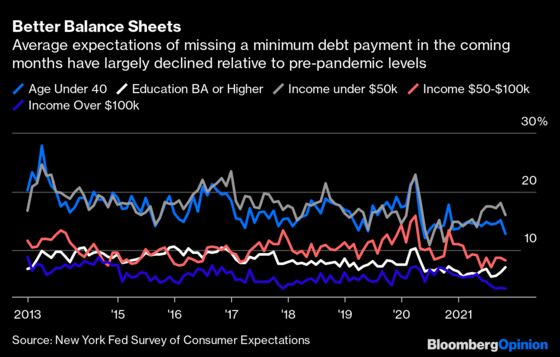

This improved financial situation is borne out in broader data on debt delinquency forecasts. According to the New York Fed’s November survey of consumer expectations released on Monday, Americans younger than 40 saw a near-record-low probability of missing a minimum debt payment over the next three months, as did those with at least a bachelor’s degree. Predictably, those with higher incomes see themselves more able to afford debt payments, but even for those making less than $50,000, the outlook is better than during most of the pre-Covid period.

The economic stimulus provided by the past 20 months of student-loan relief isn’t that different from a tax cut, as Moody’s Investors Service has pointed out previously. Instead of having to pay the U.S. government interest on their college debt, Americans could divert that money to essentials like gas or groceries, put a down payment on a house or invest it in financial markets that have roared higher since the moratorium was put into place. Some cash might have even found its way into meme stocks or crypto. It’s understandable that borrowers don’t want to give up some of that financial flexibility.

However, the persistent inflation in recent months, which caught the Biden administration and Fed Chair Jerome Powell by surprise, suggests there’s little need for extending a tax cut-like stimulus, especially one as poorly targeted as student-debt relief, which affects those with lower incomes but also wealthier individuals. The accelerating growth in consumer prices and wages already benefits debtors as their fixed interest payments become relatively less cumbersome.

That doesn’t make the decision any more politically palatable with midterm elections less than a year away. White House Press Secretary Jen Psaki said in a recent press conference that the administration wants an orderly return to loan repayment and would help borrowers make the adjustment. Meanwhile, the president is fighting to keep his “Build Back Better” plan on track as Republicans urge Democratic Senator Joe Manchin to kill the tax-and-spending bill.

Biden, Schumer and other Democratic leaders face the unenviable task of delivering on promised social programs that won them the White House and both chambers of Congress while also taming the highly unpopular inflation spike that was caused by a surge in aggregate demand at a time of constrained supply. It’s little surprise that the Fed’s hawkish pivot came just after Powell was selected by Biden to serve another four years as head of the central bank. If cooling the economy with interest-rate hikes is what’s needed to establish a paid family leave program, among other provisions in the Build Back Better legislation, that’s likely a trade-off the administration is willing to make.

The fact that there’s little interest internally at the White House about extending student loan relief reflects the reality of the red-hot economy. On top of accelerating wage growth, job openings in the U.S. remain near a record high, and Americans are voluntarily leaving their positions for better roles at a nearly unprecedented rate. For workers, including those with student debt, opportunities abound.

Of course, financial security is a highly personal topic and can’t simply be applied across the population based on macroeconomic trends. Like many Americans, I know people who are struggling with student loans more than a decade after graduation and others who sacrificed to shed the burden as quickly as possible. There’s little doubt that the explosive growth in college costs, combined with a smaller earnings premium for obtaining such a degree, will inflict still-unknown levels of harm on the millennial generation. Fortunately, judging by consumer price index data, the rapid increase in tuition and fees has slowed in recent years.

That’s of little comfort to those currently saddled with student loans, especially the most-indebted individuals with more subdued earnings potential who got a taste of what a widespread cancellation would look like. But Schumer, the Student Debt Crisis Center and others angling for extended relief no longer control the narrative in the current economy.

- What to Do About Student Debt When Covid Relief Ends: Erin Lowry

- To Curb Student Debt, Allow Bankruptcy Relief: Allison Schrager

- Student Loan Relief Should Target the Neediest: Editorial

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.