Of Course Stocks Reached a New Record: It’s Oct. 28.

(Bloomberg Opinion) -- There’s a very good reason why the S&P 500 Index rallied to close at a record high on Monday: It was the 28th of October. LPL Financial crunched the data going back to 1950 and found that Oct. 28 is historically the best day of the year for stocks, with equities rising 0.54% on average.

Crediting the jump in stocks to a day on the calendar may be intellectually flimsy, but you sure can’t pin it on the fundamentals. The move higher came on the same day that the National Association for Business Economics released a survey saying that more American companies are reporting negative impacts from U.S. tariffs, especially among goods producers. The Federal Reserve Bank of Atlanta said Monday that its GDPNow index – which attempts to gauge economic growth in real time – has dropped to 1.675, its lowest level since early September. And there’s more: the Chicago Fed said its National Activity Index for September contracted, while the Dallas Fed said its regional manufacturing index fell back below zero.

Sure, corporate earnings are doing slightly better than expected, but that’s not saying much. Third-quarter earnings are tracking at a 3% decline from a year earlier versus the 4% drop that was forecast. But that’s all in the past. The problem is that the outlook is deteriorating. Forecasts for the fourth quarter have been cut to a gain of 1.2% from the 5.4% increase that was seen at the end of July, according to Cantor Fitzgerald. The one positive for stocks was a statement from President Donald Trump, who said the U.S. was ahead of schedule to sign part of a trade deal with China. But there’s been so many false starts when it comes to a trade agreement that it’s surprising traders wouldn’t demand to see a signed document before getting too bullish. The truth is that this year’s deteriorating fundamentals have supported the bearish narrative, but the 20% gain in the S&P 500 shows how the market doesn’t always act rationally.

Perhaps the reason stocks have done so well is because the bears are throwing in the towel, finding it increasingly expensive to finance positions that would profit from a drop in equities. Goldman Sachs Group Inc. says the outflow from U.S. equity funds this year has been the biggest since 2008, relative to the flood of money into cash and bonds. As for what’s ahead, LPL has something that should add even more misery to the bears: Not only is Oct. 28 the best day of the year for stocks, it also markets the start for what has historically been the best six-month period for equities.

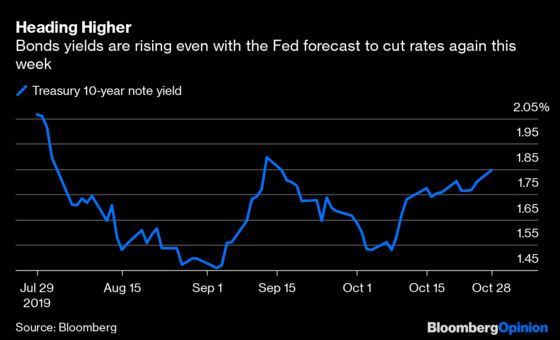

BONDS TAKE A HIT

All that cash Goldman Sachs says is flowing out of stocks and into bonds didn’t help the government debt market on Monday. Yields on benchmark 10-year Treasury notes rose to their highest since mid-September, reaching 1.86%, even though the Federal Reserve is forecast on Wednesday to cut interest rates for the third time since July. There are two big-picture things working against the bond market at the moment. The first is that in the U.S., traders expect the Treasury Department this week to provide an update on how it plans to f inance a growing budget deficit that has reached about $1 trillion. Not only is it likely that the U.S. will soon be boosting its borrowing, it’s also possible officials will introduce a 20-year security for the first time. Such speculation may be a reason long-term yields have risen more than short-term ones in recent weeks. The second is more of a global issue, with more major central banks — including those in the euro zone, Sweden and Japan — signaling that ever lower rates are no longer the answer to getting the worldwide economy going again. “The August lows in global bond yields, of which $17 trillion were yielding below zero, will be the lows for a while to come,” Bleakley Financial Group Chief Investment Officer Peter Boockvar wrote in a note to clients Monday.

DOLLAR DOWNSIDE

The Bloomberg Dollar Spot Index fell on Monday, and is heading for a monthly loss in October. This should be a good thing for the U.S. economy, because we’re seeing just how much of an impediment the measure’s 2.69% surge in the third quarter was for corporate earnings, especially exporters. TS Lombard is out with a new report finding that of the companies that have posted third-quarter results, the average currency impact on earnings ranged from about negative $20 million to about negative $80 million, depending on the sector. The drag from a stronger dollar is worse now than it was in 2015, even though the currency’s appreciation has been far tamer. Back then, the dollar was recovering from an extended period of underperformance and wasn’t deemed to be overvalued. Now, it is seen as too strong. “We have been arguing that for the (dollar) to weaken we need better data in the rest of the world, which effectively means we need trade deals,” the foreign-exchange strategists at Bank of America Merrill Lynch wrote in a research note Monday. “But we are skeptical that the (dollar) pullback can extend. Within the context of a fragile global economy, there has been lack of progress on structural policy matters needed to reduce the elevated state of global uncertainty, which has disproportionately affected more trade and manufacturing-exposed countries outside of the U.S. If and when this happens, the dollar can start weakening, but at this time we have not seen a catalyst.”

PALLADIUM CHARGES AHEAD

In an otherwise middling year for the commodities market, palladium is anything but. The metal reached another milestone Monday, surging past $1,800 an ounce to set another high. That brings its gain in 2019 to 43%, compared with 2.61% for the broader Bloomberg Commodity Index. Palladium is a key component in car making. But while auto production has been sluggish this year, demand for palladium has only increased due to stricter air-quality rules worldwide, given the metal’s use in vehicle pollution-control devices, according to Bloomberg News’s Joe Richter and Yvonne Yue Li. Palladium’s latest move higher is also partly due to concern that supplies are getting tighter. Production of platinum-group metals in South Africa shrank the most in 18 months in August, while growth in Russia stalled last month, government data show. Power outages in South Africa have helped cloud the supply outlook for palladium. Bloomberg News points out that automakers may seek lower-cost alternatives to palladium, with platinum often mentioned as a possible option. Research, though, has shown that technological advances are needed before it can match the performance of palladium-based catalytic converters, according to Johnson Matthey, which makes the devices. That bodes well for further gains in palladium.

ON A ROLL

Barring a last-minute disaster, October will turn out to be a banner month for emerging-market assets in as good a sign as any that perhaps the global synchronized slowdown might be about to reverse. The MSCI EM Index of equities is up 4.19% this month, topping the 2.57% gain in the broader MSCI All-Country World Index for the first time since January. An MSCI index of EM currencies has a good chance of posting its best month since January, and a Bloomberg Barclays index of local currency bonds is one of the better performers in the global debt market, having risen 1.83% in October through Friday. BlackRock Inc., one of the world’s largest investment firms, says now isn’t the time to cull some profits. It’s especially attracted to emerging-market debt. BlackRock favors local-currency markets, which could rally more as 2019 winds down amid a range-bound dollar and possible monetary easing in many emerging markets amid benign inflation, according to Bloomberg News’s Sydney Maki. Some of the best opportunities are in Latin American nations such as Brazil and Mexico, and in countries not directly exposed to U.S.-China tensions, such as India. Regardless of whether anyone agrees with BlackRock, the fact is that emerging-markets are becoming a much bigger part of the global economy and financial system. BNY Mellon says that emerging-markets now account for 43% of global gross domestic product, up from 39% in 2011.

TEA LEAVES

The strong American consumer has been credited with propping up the economy as global growth slows and the U.S-China trade war drags on. Lately, though, there are signs that cracks are beginning to form. Serious delinquencies on credit cards and auto debt have been creeping up in recent quarters, leading some banks to set aside more money to cover bad loans and tighten lending standards, according to Bloomberg News’s Claire Boston and Elizabeth Rembert. Adding to the concerns, they report, was an unexpected drop in retail sales in September, the first decline in seven months. The Conference Board will provide a monthly update on the state of consumers on Tuesday when it releases its measure of confidence for October. The median estimate of economists surveyed by Bloomberg is for a reading of 128, up from 125.1 in September. An increase is certainly a positive, but that would only put it around is average level for the year, with the index ranging between the low of 121.70 in January and the high of 135.8 in July.

DON’T MISS

Thank These Five Stocks as S&P 500 Hits Record: Robert Burgess

Don’t Let the U.S. Economy Hit Stall Speed: Bill Dudley

Expect the Fed to Put Conditions on Further Rate Cuts: Tim Duy

Trillion-Dollar Deficit May Be What Economy Needs: Karl Smith

Slinging Mud Won't Secure the World's Oil Supply: Julian Lee

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.