(Bloomberg Opinion) -- According to the Thundering Herd, the herd is thundering back into risk-taking. And the greatest spur leading it on has little to do with politics, or the economy, or the corporate sector. Instead, it is driven by that most basic human emotion: fear of missing out.

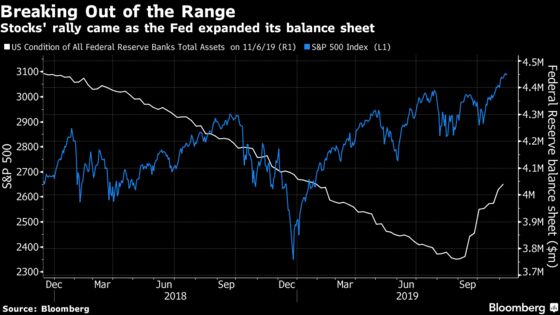

President Donald Trump’s much-heralded New York speech on Tuesday provided almost nothing that was newsworthy, but it did give him an opportunity to gloat — quite accurately — about the state of the stock markets. They have been on a tear, with most of the key U.S. benchmarks breaking out of the ranges in which they have been stuck since early last year, to set new highs. They have done this even though, as the president never ceases to complain, the Federal Reserve raised rates repeatedly last year, before reversing much of that move over the last three months.

The problem is to identify just why stock markets have suddenly strengthened. It isn’t because of an end to the trade war. Despite hopes, Trump failed to roll back any tariffs in his speech, or offer any promises on when a deal with China might be signed. His surprise announcement of new tariffs on Aug. 1 plainly forced the S&P 500 Index lower; nothing that has happened on the trade front since then would justify the 9% rally in stocks since markets troughed after that news hit.

It is also hard to attribute the rally to the economy. When stocks took a dive late last year, they did so against a background of nasty surprises in the U.S. data, as measured by Bloomberg’s U.S. economic surprise index. In the summer, that data started to surprise much more positively — but stocks were becalmed during that period. The rally has only come since the economic surprise indexes stalled, in mid-September.

The S&P’s rally also roughly coincided with the season of corporate earnings announcements for the third quarter, which came in 3.8% ahead of expectations, according to FactSet. But earnings almost always exceed expectations, thanks to the games played by corporate investor relations departments. Over the last five years, they have on average beaten forecasts by more — 4.9%. Further, third-quarter earnings were accompanied by such downbeat assessments of the future that the consensus estimate for earnings growth for the next 12 months has actually gone negative, according to SocGen Quantitative Research.

And yet, despite all of this, there is no doubt that market sentiment has turned on a dime. In mid-summer, the U.S. yield curve inverted, a classic recession signal, and many braced for an economic downturn. That’s over. According to Bank of America Merrill Lynch’s latest global survey of fund managers, we have just witnessed the greatest month-on-month improvement in economic sentiment since the survey began in 1994. A month ago, a net 37% of fund managers expected the global economy to deteriorate over the next 12 months; now, a net 6% expect an improvement.

What could possibly be behind this? The president may have at least nodded at the answer with his claim that that the U.S. indexes would be 25% higher now if the Fed had negative rates. This is a dubious assertion, as only disastrous economic conditions would prompt the U.S. central bank to take such desperate measures.

But that sudden improvement in investors’ sentiment did indeed come as the Fed reversed its policy of five years, and started to expand its balance sheet again. It did this to restore liquidity to the repo market, where banks raise their short-term funding, and the Fed has protested repeatedly that this is not a return to “QE” asset purchases to boost the economy. For all these protestations, the market has treated it as a turning point.

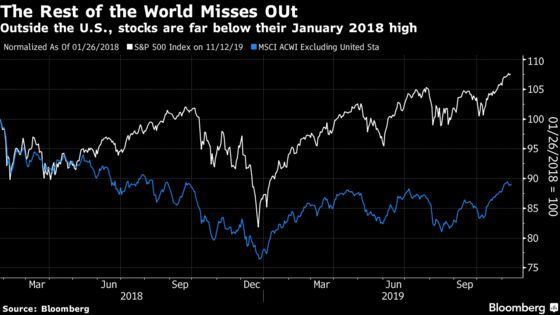

Added to this, as mentioned, there is the age-old fear of missing out. The end of the year is coming, when investment managers will be judged on their performance. Those who are behind have an incentive to clamber into the market now, while there is still time. And the rally has been unbalanced, with most gains going to a small group of large U.S. stocks. If the stars align for a broad recovery, there is ample potential for big rallies by smaller companies, and by stocks outside the U.S. The rest of the world has joined in this rally, but there is still a long way to go before they catch up — and nervous investment managers are conscious of this.

It is tempting to fit a narrative of economic and trade optimism to the rebound in appetite for risk. But sadly, this looks a lot like a return to the pathology that has dominated throughout the post-crisis decade: markets await free money from central banks, and fear missing out when that money arrives.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2019 Bloomberg L.P.