(Bloomberg Opinion) -- From U.S. Treasury securities to gold and the shares of utility and healthcare companies, it’s been a great time for financial assets that provide a hedge against an economic slowdown. And as the latest U.S. economic reports show, it’s too soon to abandon so-called defensive assets even though the stock market has rebounded and is back near a record high.

The most important takeaway from last week’s data, especially the drop in retail sales and industrial production, is that Main Street has joined Wall Street in anticipating the slowdown in economic growth to continue, and possibly lead to a recession. This confluence warrants a more rapid shift in allocation from higher risk assets, such as equities like those in the technology sector whose valuations are dependent on rapid growth, to more defensive holdings.

The unexpected 0.3% decline in retail sales for September is an ominous development ahead of the holidays when seasonal factors should be boosting spending and suggests consumers are increasingly concerned about the trade wars that President Donald Trump is waging with China and Europe, and how that could eventually affect U.S. workers’ employment and wages.

Retail sales often serve as a leading indicator of overall consumer spending, which accounts for around 70% of gross domestic product. Rather than an isolated event, the drop in sales last month followed declines in consumer sentiment and confidence measures. Since weak consumer spending cannot be offset by other components of aggregate expenditures such as capital spending or government outlays -- they collectively account for less than a third of GDP – it carries a lot of weight in determining economic growth.

Industrial production dropped 0.4% in September, much worse than the 0.2% increase that was forecast. Although a portion of the decline was due to a strike by General Motors Co. workers, the adverse impact on suppliers to the automaker appears to have continued in October -- as does the strike. That could have a negative impact on economic growth in the final quarter of the year.

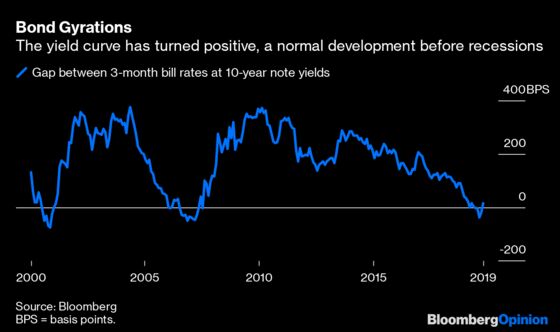

None of this is a surprise to those who deal in the market for Treasuries securities, which has been flashing yellow for some time. The difference, or spread, three-month bill rates and 10-year note yields was consistently negative from May until just recently due to speculation the Federal Reserve will aggressively lower interest rates in response to a slowing economy.

An inversion in this part of the yield curve has been a reliable predictor of recessions the past several decades. And although Larry Kudlow, Director of the National Economic Council, suggested on Thursday that the return to a positive yield spread presaged a growing economy, history suggests otherwise. An inversion of the yield curve for several months, followed by a steepening to positive spread levels before the recession begins, has been the pattern in the two most recent recessions, from March 2001 to November 2001, and from December 2007 to June 2009.

How do we explain the inversion reversing even before a recession begins? An inversion heralds a recession some nine to 12 months ahead of its inception, so the switch to a positive spread looks beyond the recession in anticipation of the subsequent recovery.

The recent steepening of the yield curve should not be a source of comfort. Rather, the focus should be on the convergence of factors from the financial and real sides of the economy that is heightening the probability that a recession is in the cards.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.