(Bloomberg Opinion) -- Active equity investors, they tell us, are far better stewards of our savings when markets are volatile. Their underperformance compared with passive investment products in recent years, they explain, is down to ever-rising stock markets flattering the returns available from index trackers. So the recent surge in volatility, with equity prices exhibiting unprecedented short-term swings, would have been their time to shine, right?

Wrong.

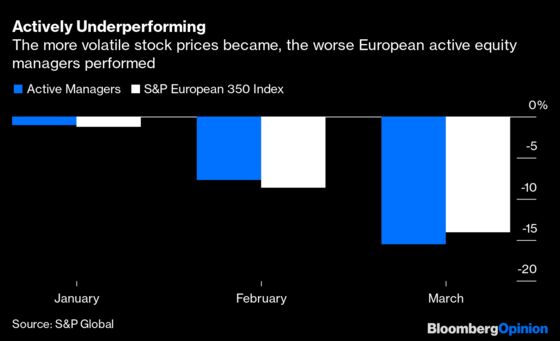

“The majority of Europe equity fund managers were unable to beat the benchmark in either March or Q1 2020 as a whole, with 66% and 57% underperforming the benchmark, respectively.” That’s the embarrassing verdict of a study just published by S&P Global Inc., which provides credit ratings and compiles market benchmarks.

March was the most volatile month on record for stocks, as measured by the Chicago Board Options Exchange Volatility Index, known as the VIX index. Equity prices swinging by as much as 5% in a day triggered stock exchange circuit breakers that paused trading in the benchmark U.S. markets several times.

So March should have presented the perfect opportunity for stock pickers to profit from their alleged superior investing skills. As it turned out, only 34% were able to deliver total returns that beat a benchmark index, according to S&P calculations.

The smaller losses suffered in January and February meant that active managers underperformed the index by a smidgeon for the quarter as a whole, losing 22.7% compared with the 22.4% decline in the benchmark. But only 43% of the managers assessed were able to beat the benchmark during the first three months of the year, S&P says. Little wonder that customers are increasingly skeptical that the higher fees charged on actively managed products are justifiable.

Both retail and institutional customers are losing faith in the fund management industry’s ability to look after their wealth – and rightly so. Earlier this month, the CFA Institute published a survey of more than 3,500 retail investors in 15 countries, as well as more than 900 institutional investors with assets of at least $50 million.

The percentage of institutional clients who regarded investment firms as well prepared to manage through a financial crisis declined to 68%, down from 80% in a 2018 survey. Among retail savers, the figure was just 49%, down from 55% two years ago.

A financial crisis is the time when trust is truly tested, the CFA said. With active managers found wanting during the recent market meltdown, they may just have blown their last chance to halt the flood of investors preferring to entrust their nest eggs to the low-cost passive crowd.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.