The Ugly Truth About Market Bubbles Is That Everyone Loses

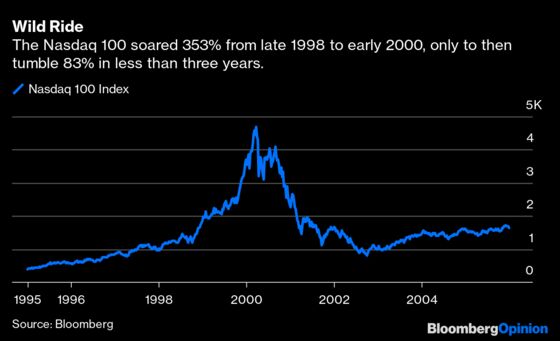

(Bloomberg Opinion) -- I was chatting a few days ago with one of the smartest hedge fund managers I know. We were talking about the recent carnage in unprofitable tech “dream” stocks, and he reminded me of a time many have forgotten. “From 1995 to 2000, I watched some of the shrewdest managers get annihilated shorting the dot-com bubble,” he said. “By the end, they all went out of business. I then watched the next five years destroy all the long managers who had ridden the euphoria to the upside, until most of the aggressive ones were also sent packing.”

In hindsight, bubbles always seem obvious and easy to trade. As someone who has experienced more of these than I care to remember, I assure you they are not. Take the mid-2000s real estate episode. With movies such as the “Big Short,” and glowing newspaper articles about hedge fund managers who made fortunes profiting from the real estate collapse, it seems like opportunity was everywhere.

What we forget is that these trades were successful because so few believed they could happen. I can’t tell you the number of times a young trader tells me, “I wish I had been around back then, ‘cause I would have made a killing!” What they don’t understand is that, in the moment, bubbles are extremely difficult to identify. They are even tougher to trade.

I’ll never forget trying to take advantage of the real estate mania in 2005. I thought the sector was wildly overpriced. That February, when it appeared the homebuilders had topped and started to roll over, I shorted a basket of homebuilder stocks. The trade worked until April. Then, much to the surprise of the bears, homebuilder shares ripped higher by 35% in the space of two months, and I got shaken out of my short positions.

The ugly truth about bubbles is that both the bears and the bulls end up losing. The bears are inevitably too early, and by the time the market rolls over, the vast majority have given up. The bulls, who have been conditioned to buy every dip, stay at the party much too late.

Bubbles used to be rare and encompass entire asset classes. But markets have evolved. Even back almost a decade ago it wasn’t hard to see how the proliferation of hedge funds had decreased the amount of available “alpha,” creating an environment prone to a series of rolling mini-bubbles. As sophisticated investors deployed capital into themes or sectors, the price action encouraged momentum-chasers. This affirmed the belief that the fundamental investors were on to something, causing more buying and resulting in a positive feedback loop.

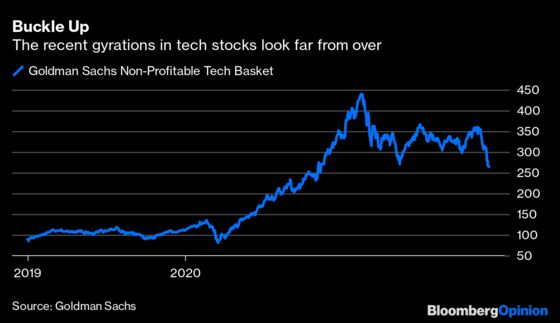

Then Covid-19 hit and mini-bubbles became perversely extreme. At the March 2020 crisis bottom, the Goldman Sachs Non-Profitable Technology Index had fallen 40%, attracting short sellers. Then, over the summer, the basket of shares rallied 38% and financial airwaves were filled with gurus like Chamath Palihapitiya and Cathie Wood espousing the virtues of these new technology marvels. And, just like previous bubbles, even the skeptics eventually feared shorting due to the violent rallies. Some 11 months later, this group of stocks had risen an astonishing 478%.

And yet, here we are. The index has declined 41% from the 2021 high. Surely, there are individual “rock star” investors who made money, but as a group, both the bulls and bears have been beaten up. Most of the vocal bears have stopped forecasting a decline, while the majority of bulls remain long even though many are now underwater on their trades.

I don’t know the direction of this sector over the short-run, but experience tells me it is a painful bear market with face-ripping rallies that lure bulls back in and forces bears to cover their bets before it resumes its relentless march lower.

Years from now, with the benefit of hindsight, it will seem obvious these stocks were wildly overvalued. The few investors smart enough to get out at the top, or lean into the short side on the way down, will be celebrated. It will all seem so easy. Yet, in the midst of the actual event, it is anything but.

More From Other Writers at Bloomberg Opinion:

- Are Hedge Fund 'Bubble' Bets Naughty or Nice?: Chris Bryant

- Really, Truly, Holistically, Stocks Are Expensive: John Authers

- Fed Ignores Key Bubble Risk for Stock Market: Brian Chappatta

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Kevin Muir is a former institutional equity derivative trader who now writes the MacroTourist newsletter.

©2021 Bloomberg L.P.