(Bloomberg Opinion) -- After posting the biggest back-to-back weekly advance since early June for a total gain of 4.58%, the rally in the S&P 500 Index stalled as a new week dawned. Perhaps it’s because the increases were more about things not getting any worse, rather than any new reason for optimism about such fundamentals as economic growth, earnings and U.S.-China trade relations. The fact is, the risks around all three of those things aren’t going away anytime soon, as traders realized Monday.

The Federal Reserve Bank of Atlanta’s GDPNow index – which attempts to gauge economic growth in real time – took another leg lower, falling to a below-trend rate of 1.467%. On the geopolitical front, the U.S. appears no closer to reaching a trade agreement with China, with the two sides only agreeing to talks next month in an effort to set up the parameters for further discussions. “Will there be a deal between China and the U.S.? I have my doubts,” Steve Eisman, the Neuberger Berman Group money manager whose bets against the housing market before the financial crisis were chronicled in Michael Lewis’s 2010 book “The Big Short,” said Monday on Bloomberg TV. “My impression is that China is not backing down on anything,” so to get a deal “Trump basically has to give in.” And when it comes to earnings, strategists are quickly downgrading their forecasts. The latest to do so is LPL Financial Chief Investment Strategist John Lynch, Citing the escalating trade war, he cut his 2019 earnings-per-share forecast for the S&P 500 to $165 from a prior estimate of $170, representing a paltry 2% to 3% growth rate for the year. “Slower economic growth hampers revenue, while paying tariffs and dealing with supply chain disruptions hurt profit margins,” Lynch wrote in a research note. “In addition, business uncertainty around future trade actions weighs on capital investments, which limits opportunities for companies to grow revenue, particularly industrial and technology companies, and caps gains in productivity” that “could boost profit margin.”

A MILE WIDE AND AN INCH DEEP

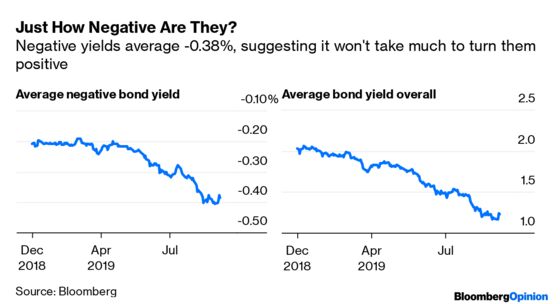

The upside - if there is one – to the recent “correction” in the global government bond market is that it has shrunk the universe of debt with negative yields pretty significantly, to $15.6 trillion as of Friday from a peak of just over $17 trillion on Aug. 29. For those readers without calculators, that amounts to $1.4 trillion. This is good news for two reasons. The first is that the rapidly expanding universe of negative-yielding debt has raised concern that it could pose a systemic risk to the global financial system. After all, getting paid to borrow money isn’t natural. So, any decrease is a positive. The second is that the recent move shows it doesn’t take much of a market move to turn negative-yielding bonds into positive-yielding ones, mainly because those negative yields are relatively slim at an average of minus 0.38%, according to the Bloomberg Barclays indexes. That compares with an average of 1.23% for the global bond market. Holding a bond – especially a government bond – with a yield below zero percent isn’t much different than paying a bank for a safe deposit box to hold one’s valuables. You might not make any money, but you know the money you do have is safe, and paying 38 basis point for that peace of mind doesn’t seem too onerous in today’s environment.

OIL JOINS THE PARTY

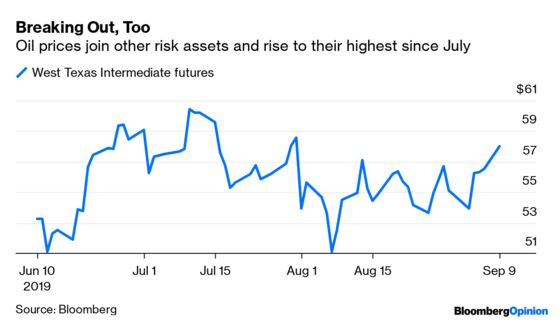

Many riskier assets such as equities have broken through the top end of their recent trading range in a sign of optimism. Oil, though, was conspicuous by its absence. That changed on Monday as West Texas Intermediate crude futures surged as much as $1.64, or 2.90%, to $58.16 a barrel, the highest since July 31 on a closing basis. The move in crude had nothing to do with rising demand eroding a glut of supply and ratifying the idea seen in equities that perhaps the broader economy isn’t as bad as envisioned. Instead, the surge higher was all about an attempt by OPEC and its allies to reassert their control over the global oil market. That was demonstrated in comments by newly-appointed Saudi Energy Minister Prince Abdulaziz bin Salman, who said there won’t be radical change in the policy of the group referred to OPEC+. The group, which includes Russia, has cut crude production this year to prevent a glut and shore up prices. Meanwhile, the United Arab Emirates energy minister promised a push to get all members committed to curbs, but said there’s no recommendation to make deeper reductions, according to Bloomberg News Sheela Tobben. The answer to the question of whether the global economy is strong enough to withstand higher prices for such key raw materials as oil may soon be answered.

REVERSING, BUT IN A GOOD WAY

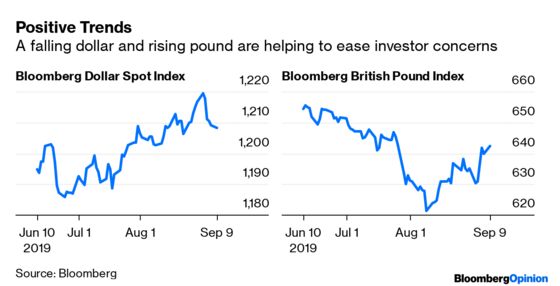

No list of the many risks confronting the global economy and markets would be complete without mentioning a strong dollar getting stronger and a collapsing British pound. But recent moves in the currency market are starting to alleviate some of those concerns. The Bloomberg Dollar Spot Index has fallen for five straight days, its longest slump since June and mitigating some of the pressure on big, U.S. multinational exporters. It’s probably no coincidence that the S&P 500 Index jumped 1.79% last week as the dollar fell. S&P Global Ratings figures that 30% of the revenue of S&P 500 companies comes from outside the U.S. The Bloomberg British Pound Index jumped on Monday to its highest since July 26, bringing its gain to 3.34% since closing at a low for the year on Aug. 9. The move higher in sterling is a reflection of growing speculation that the U.K. will avoid crashing out of the European Union at the end of October without an exit deal that would potentially throw the global economy and markets into turmoil. The latest bit of optimism comes with Prime Minister Boris Johnson seemingly softening his stance on leaving the EU on Oct. 31 with our without a deal. There’s also the latest data showing the U.K. economy is holding up, growing at its fastest pace in six months in July. At least to currency traders, the world is looking like a less dangerous place, with the JPMorgan Global FX Volatility Index posting its biggest four-day decline since August 2011.

THE LURE OF EMERGING MARKETS

The weakness in the dollar has given emerging markets a boost, with the MSCI Emerging Markets Index of equities rising on Monday to its highest level since Aug. 1. That’s because every time the greenback lurches higher, there are doubts that emerging-market borrowers will have the ability repay the trillions of dollar-denominated debt taken out in recent years. In a sign of confidence, investors have added money to exchange-traded funds that buy emerging-market stocks and bonds for two straight weeks. Inflows to U.S.-listed emerging-market ETFs that invest across developing nations as well as those that target specific countries totaled $74.9 million in the week ended Sept. 6, compared with gains of $69.4 million in the previous week, according to data compiled by Bloomberg. Inflows total $381.9 million this year, meaning the past two weeks accounted for large chunk, or 38%, of all money that have poured into these funds in 2019. Now, many investors are saying that further gains in emerging-market assets may depend on what the European Central Bank does at its monetary policy meeting Thursday. A dovish decision that includes further monetary stimulus would likely keep demand for emerging-market assets strong. “The ECB meeting on Thursday will be crucial for setting the tone of sentiment in emerging markets,” Paul Greer, a London-based money manager at Fidelity International, whose emerging-market debt fund has outperformed 97% of peers this year, told Bloomberg News.

TEA LEAVES

The best word to describe sentiment among small U.S. business owners may be “sticky.” Despite evidence of a slowing economy, the National Federation of Independent Business’s monthly index of sentiment among this group has risen in five of the past six months. At a reading of 104.7 in July, the gauge is closer to its record high of 108.8 in August 2018 than its average of 98.3 since 1975. But could the report for August due to be released on Tuesday finally show that confidence is starting to wane? Unlikely, according to economists, who expect only a slight pullback to 103.5, which would still be higher than all but two others months this year. But as Bloomberg Economics points out, anecdotal evidence, such as respondents’ comments in the August non-manufacturing Institute for Supply Management survey, suggests that existing trade-war tariffs “are affecting companies’ costs, particularly in the accommodation, food services and construction sectors; many small businesses are concentrated in these industries. As such, the re-escalation of trade tensions could drive small-business sentiment down.”

DON’T MISS

Fed and ECB Are Stuck in a Shrinking Corner: Mohamed A. El-Erian

Mario Draghi Is Breaking Out the Bazooka Again: Marcus Ashworth

A Stronger Yuan Is Manna for Emerging Markets: John Authers

The World's Oil Glut Is Much Worse Than It Looks: Julian Lee

Fracking Is the Bridge to a Fully Renewable Future: Noah Smith

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.