(Bloomberg Opinion) -- In talking with a number of market players the last few weeks, there seems to be a broad consensus that 2022 is going to be more challenging than 2021, which almost makes me wonder if stocks won’t be up another 20% next year, defying bearish expectations yet again. But things are a little different than this time a year ago.

For starters, the Federal Reserve is beginning the process of reversing its ultra-loose monetary policy. It’s not moving fast enough relative to the inflation that was unleashed, but it’s doing so in an environment where markets are increasingly sensitive to the potential for higher interest rates, due to the vast amounts of leverage in the system and the amount of government debt incurred in the last few years. The Fed hasn’t increased rates yet, and probably won’t until March, but the yield curve has already flattened to a very slim 80 basis points, suggesting that we are moving ever-closer to a recession.

I have been through a few yield-curve flattening cycles and every one is accompanied by a raft of dumb analysis. The first is the mechanics behind the measurements. The convention is to use the difference in yields between two- and 10-year U.S. Treasury notes, but there are some annoying purists that always come out of the woodwork and say that you should really use three- or six-month Treasury bill rates instead of two-year yields. Typically it takes longer for the curve to invert when bills are used as the benchmark, which gives people hope that a recession is further in the future than they think.

The second is the speculation that this time is different, and that maybe this particular flattening of the yield curve, or even an inversion, won’t result in a recession. But the yield curve is the undisputed heavyweight champion of market indicators — an inversion always predates a recession. It’s just a matter of timing. If the Fed stays on its current path — or accelerates — then it looks probable that the yield curve will invert sometime in early 2022, right around the time that the actual rate increases are forecast to start. Then the clock starts, as a recession can happen anytime over the next 18 months, going by the relationship between inversions in the yield curve and economic contractions.

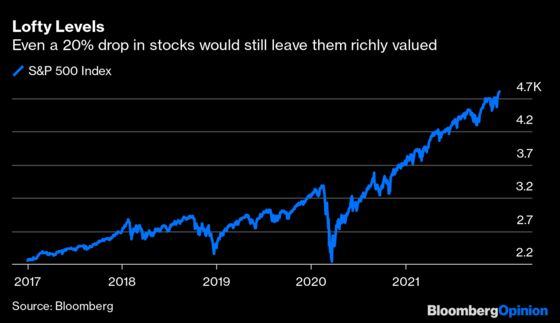

The question then becomes how much will the stock market drop? Potentially a lot. Stocks weren’t particularly cheap before the pandemic, and there has been a lot of speculation and froth over the last 18 months or so. For example, a 20% drop, the technical definition of a bear market, would only take the S&P 500 Index back to the beginning of 2021.

Investors also need to take the reaction function of the Fed into account. If the current high rates of inflation fail to recede, the Fed might panic and raise rates too far, too fast, triggering some type of crisis. The Fed already erred in believing that faster inflation was transitory, and the risk is that policy makers will make an error of the second type, overreacting and plunging the markets into chaos, is not zero.

If that wasn’t enough, 2022 will bring the midterm U.S. elections. Current polls would suggest that the Democrats are headed for a big defeat in Congress, with Republicans gaining control of the House. A lot can change between now and November, but it’s hard to see Democrats increasing their majority at this point. This has profound implications for fiscal policy. Huge Republican gains in the 1994 and 2010 midterm elections resulted in six years of relative austerity under presidents Bill Clinton and Barack Obama. The result was a budget surplus at the end of Clinton’s second term. Fiscal spending was especially lean from 2010 to 2016, as the budget deficit shrank from around 10% of GDP to about 2% of GDP. Republicans are by no means fiscally conservative, but they are reliably so when they are in the opposition.

A Republican majority in Congress would probably result in the budget deficit dwindling from $3 trillion or more to less than $1 trillion. And since much of the current deficit consists of government transfer payments, the result would be far less consumer spending and a few percentage points less in GDP growth. And since inflation has been driven mostly by loose fiscal policy, austerity has the potential to slow or stop inflation.

Next year will be tougher for the financial markets and the economy. But nobody should complain if stocks have very low or even no returns, because there is the potential for something much worse.

More From Other Writers at Bloomberg Opinion:

- Finding Cheaper Alternatives to Expensive Stocks: Nir Kaissar

- Behold the Paranoid Style in American Investing: Chris Bryant

- What Eight Charts Tell Us About 2022: Gilbert & Ashworth

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jared Dillian is the editor and publisher of The Daily Dirtnap, investment strategist at Mauldin Economics, and the author of "Street Freak" and "All the Evil of This World." He may have a stake in the areas he writes about.

©2022 Bloomberg L.P.