(Bloomberg Opinion) -- The S&P 500 Index spent most of Monday higher, thanks in part to a couple of second-tier reports on manufacturing that showed the U.S. economy may not be getting any worse. But with equities already up about 20% for the year and price-to-earnings ratios more in line with a roaring economy than one in slowdown mode, the latest data is hardly enough to quell the feeling that the market may be due for a reckoning.

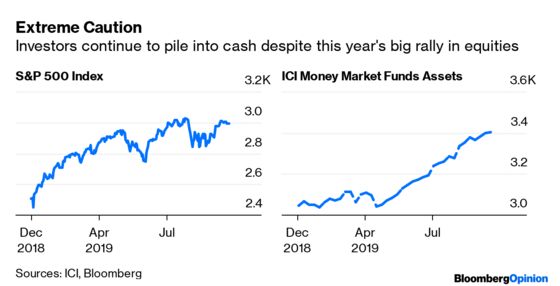

Such a view would make sense if not for one thing, which may come as a surprise to some: Stock investors are actually a lot more downbeat than the indexes indicate, and that can only be seen as a bullish signal. Some $1.1 trillion shifted out of equities and into bonds and money market funds during the last year, marking the biggest asset-class rotation in history, according to research from quantitative strategists at Sanford C. Bernstein. “If history is a guide then such periods of outflows tend to see somewhat better equity returns over the following six months,” analysts including global head of quantitative strategy Inigo Fraser-Jenkins wrote in a report dated Sept. 23. It’s true: Assets in money market funds have surged by $363.3 billion this year to $3.40 trillion, already making 2019 the biggest year for inflows since 2008, when huge losses in equities, credit and other markets following Lehman Brothers Holdings Inc.’s bankruptcy sent investors fleeing to cash. The State Street Global Markets monthly index shows investors are less confident in the outlook for equities than during the financial crisis. The abundance of pessimism shows that anybody who wanted to reduce their exposure to equities has already done so, limiting the downside. The rebounds from the sell-offs in May and August provide evidence of that. It also suggests that it would probably only take a small amount of optimism on the economy or earnings to get a big chunk of that cash that’s currently sitting on the sidelines to flow back into the market.

“This clear lack of demand” for equities “throws cold water on theories of excess exuberance for stocks,” Bloomberg Intelligence equity strategists Gina Martin Adams and Michael Casper, wrote in a research note Monday. The stock market’s “primary vulnerability would be an unlikely spike in interest rates that constrains profit and buybacks.”

BANKS SPEND BIG ON BONDS

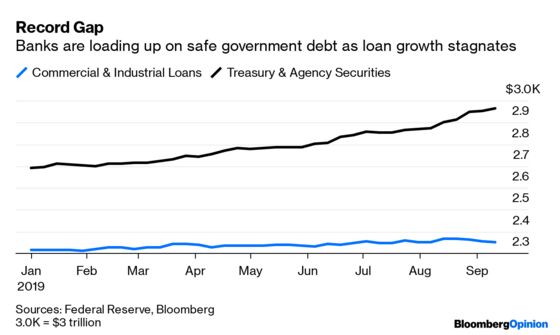

Bond traders weren’t impressed with the economic data, as the yield on the benchmark 10-year U.S. Treasury ended flat on the day. At one point Monday, the yield was as low as 1.66%, down from a six-week of high of 1.90% on Sept. 13. Bankers also don’t seem impressed with the data in recent weeks showing the economy may be firming. That is seen in their weekly holdings of super-safe government and agency-related debt, both on an absolute basis and relative to their commercial and industrial loans. Weekly Federal Reserve data released late Friday showed that banks continue to scoop up bonds, owning a total of $2.965 trillion, up about $300 million for the year. Their outstanding commercial and industrial loans, though, have fallen for three straight weeks, to $2.35 trillion. The gap between the two has never been greater, and in most years before the financial crisis, loans exceeded bond holdings. As for the slowdown in loan growth, it may not be due entirely to banks retrenching. Minutes of the Fed’s late July monetary policy meeting noted how banks were, on net, easing standards and terms on commercial and industrial loans, with many citing aggressive competition as the reason for doing so. This suggests that borrowers are pulling back.

LIQUIDITY CONCERNS ARE OVERBLOWN

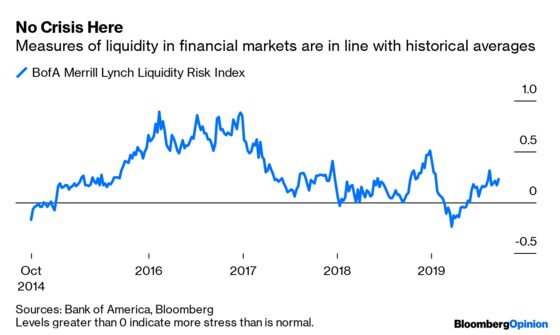

Last week’s turmoil in the repo market seems to be rapidly fading. Money market rates held steady on Monday, while a daily Fed operation aimed at keeping funding markets on an even keel was undersubscribed for the first time since Tuesday, according to Bloomberg News’s Alexandra Harris. Given the repo market’s reputation as the essential “plumbing” for financial markets, the recent events sparked concern that some type of liquidity crisis is looming. After all, a sudden shortage of available safe collateral assets such as Treasuries that are used for lending and borrowing in the repo market had been a primary source for the liquidity crisis during the Great Recession as well as in 2011 during the euro zone sovereign debt crisis. But this time, there is little evidence that the ructions in repo are suggesting that anything is systemically wrong in the financial markets. The Bank of America Merrill Lynch Liquidity Risk Indicator has been above zero – a level that indicates less stress in the financial system – since early June, and is in line with the average over the past five years. “The question isn’t what happens over the next three to six days, it’s what happens over the next three to six months,” Gennadiy Goldberg, senior U.S. rates strategist at TD Securities, told Bloomberg News.

INDIA STOCKS SOAR

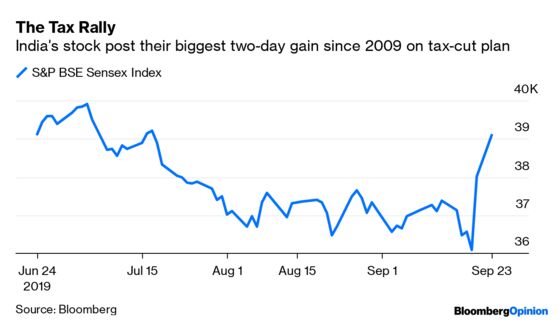

Anyone who doubts that fiscal stimulus isn’t the cure for what ails slowing global economic growth need look no further than India. After falling on Thursday to its lowest level since early March, the nation’s the benchmark S&P BSE Sensex has strung together its biggest two-day gain since 2009 by rising 8.30%. The spark for the rally was a decision by the government to unveil a $20 billion plan that entails cutting tax rates on businesses to one of the lowest levels in Asia, a move intended to supplement the central bank’s interest-rate reductions and help bolster economic growth from a six-year-low, according to Bloomberg News. Developed-market governments have largely been hesitant to embark on deficit spending to boost their economies despite rumbling from central banks that monetary policy has largely done all that it can, with interest rates in many places near or below zero. The flip side is that such fiscal stimulus tends to weigh on the bond market, boosting borrowing costs. And on Monday, two Indian state-owned lenders withdrew rupee-denominated debt sales amid fears of additional government borrowing to pay for the fiscal spending. The average yield on top-rated 10-year corporate bonds jumped 15 basis points Friday to 7.94%, the biggest one-day gain since January, data compiled by Bloomberg show. The surge mirrored a spike in sovereign bond yields.

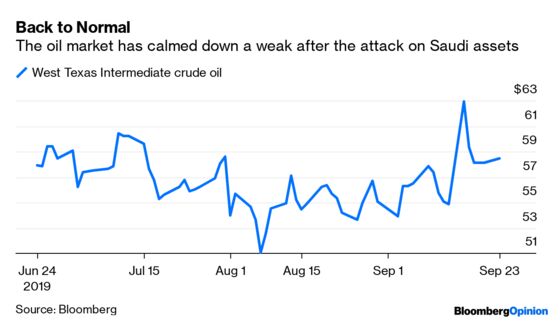

WHAT OIL RISK? I WANT YIELD

This time last week there was a general sense of fear in global markets, as oil futures soared by the most on record following an aerial attack that cut off almost six million barrels of Saudi Arabian daily production. Now, the oil market has calmed down enough that Abu Dhabi went ahead and sold $10 billion of bonds in its first international offering in two years. The offering is a clear bet by the oil-rich Middle Eastern nation that investors will look past the rising geopolitical risk in the Middle East for an opportunity to grab what is likely to be debt from a quality issuer at attractive relative yields. Its credit ratings are among the highest in the Middle East and Africa, and the cost to insure its debt against default is the lowest in the region, according to Bloomberg News. The new securities will likely be rated Aa2 by Moody’s Investors Service and AA by S&P Global Ratings and Fitch Ratings. “With a fortress-like balance sheet, they can afford to come to market at minimal or no concession,” Patrick Wacker, a fund manager for emerging-market fixed income at UOB Asset Management Ltd. in Singapore, told Bloomberg News.

TEA LEAVES

U.S. economic data last week showed the big drop in mortgage rates that resulted from the plunge in U.S. Treasury yields is having a positive effect on the housing market. Housing starts in August rose at the fastest pace since mid-2007. Existing home sales rose to the highest in more than a year. Good news, no doubt. But on Tuesday, we will find out whether any of this is doing much to real estate values. The Federal Housing Finance Agency is forecast to say that its house price index rose 0.3% in July, less than the 0.5% average monthly gain the past five years. Also on Tuesday, the S&P CoreLogic Case-Shiller National Home Price index is estimated to show a 2.10% increase in July from a year earlier, marking the 16th straight month during which gains have slowed. The muted action in prices is actually a good sign for the economy, as it shows consumers may be – for once - showing some disciple, which should help soften the blow when the next economic downturn arrives.

DON’T MISS

U.S. Data's Beating Forecasts. Hold the Applause: Robert Burgess

When Fed Fixes Repo Markets, Don’t Call It QE: Brian Chappatta

The World's Oil Security Blanket Has Been Torched: Julian Lee

National Health Care Might Be Good for Capitalism: Noah Smith

India Sends Up the Money Helicopter With Tax Cut: Andy Mukherjee

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.