The Most Important Number of the Week Is Minus 588

There’s a lot more anxiety among investors than actual index levels and broad valuations suggest which a healthy development

(Bloomberg Opinion) -- Charlie Munger has seen it all when it comes to money and markets. At 97, he and partner Warren Buffett have built a track record that is second-to-none in the world of investing. By one calculation, they have created about $600 billion of shareholder value since the mid-1960s as the stewards of Berkshire Hathaway Inc., which works out to a 3,300,000% return. So it’s hard to take issue with comments Munger made at the Sohn Conference in Sydney, where he said that he considers “this era an even crazier era than the dot-com era” that ended in a tremendous bust. But I will.

Munger is certainly right that values are hard to justify in some esoteric corners of the financial markets, namely cryptocurrencies and non-fungible tokens. There, prices are based more on hopes and dreams than any semblance of fundamentals.

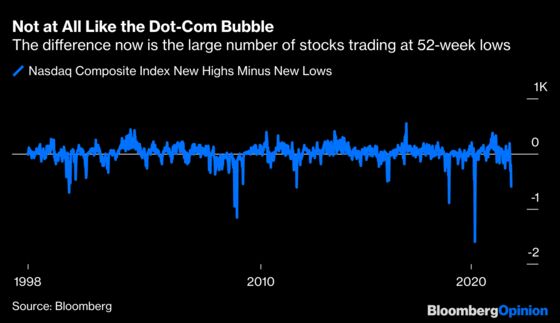

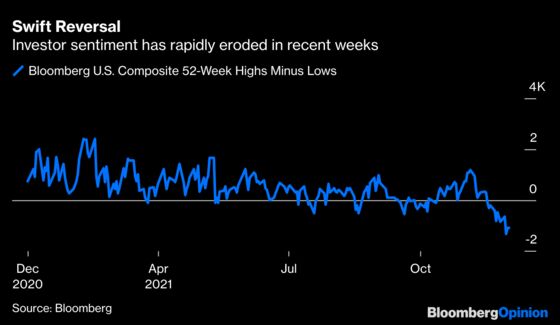

The same cannot be said of the stock market, where Munger traffics. So, despite the stock market having doubled from the early days of the pandemic in March 2020 to a record high, animal spirits are hard to find. Peeling back the cover of the Nasdaq Composite Index reveals far more stocks among its 3,598 members hitting 52-week lows than reaching 52-week highs. At minus 588 this week, that ratio has rarely ever been this negative. When the Nasdaq peaked in March 2000, the ratio was a positive 354. (The long-term average since the late 1990s is around positive 17.)

A Bloomberg index that tracks all equity markets tells a similar story, with stocks hitting new lows outnumbering those reaching highs by 1,309 this week. The average for that measure, which goes back to early 2002, well after the dot-come bubble deflated, is 81 in favor of those shares touching new highs.

This all suggests that there’s a lot more anxiety among investors than actual index levels and broad valuations suggest. And that’s a healthy development. It shows investors are becoming much more discriminating after a period when it seemed that even a monkey throwing darts at a chart of stocks could have been assured of landing on a winner.

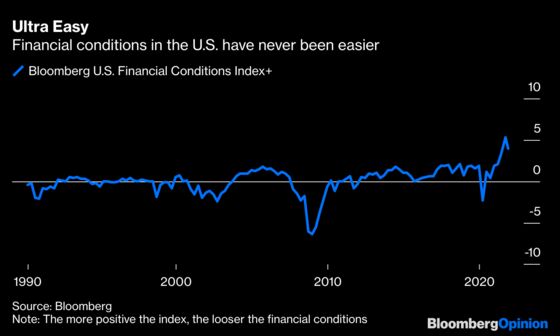

But is any dread warranted? Yes. The Federal Reserve is turning less dovish and is poised to wind down its pandemic-era monetary support faster than it envisioned because of high inflation rates. But that doesn’t mean it’s turning hawkish and tightening monetary policy. In fact, financial conditions are as loose as ever, and real interest rates are deeply negative. Neither will change much anytime soon. And, sure, much is unknown about the new omicron variant of Covid-19. What we do know, though, is that the economic impact of each new variant and wave has been less and less.

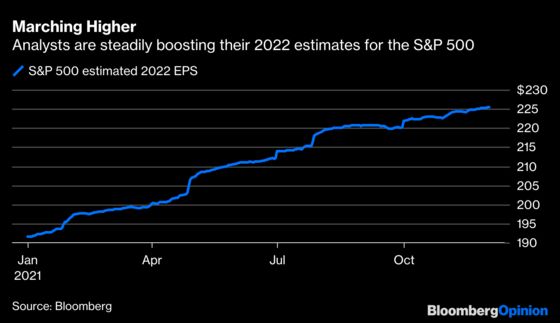

One big difference between the current stock market and the one during the dot-com boom is the quality of earnings. Despite the recent spike in inflation, companies in the last two quarters enjoyed their fattest profit margins since 1950, at around 15%, according to the Bureau of Economic Analysis. Margins were less than 5% at the turn of the century. And guess what? Analysts continue to increase their earnings estimates for this year and next. In January, members of the S&P 500 Index were forecast to generate profit of around $165 a share this year. That is now up to $210. The forecast for 2022 is $225 a share. As Jim Paulsen, Leuthold Group Inc.’s chief investment strategist, wrote in a research note this week, earnings “momentum is stronger than any point since at least 1990 and is perhaps more robust than any other time in post-war history.”

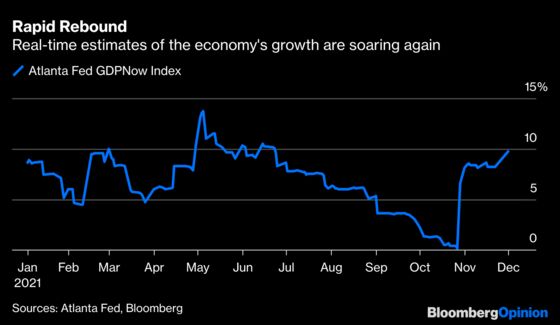

The earnings outlook is getting strong because the economy is becoming stronger. The Federal Reserve Bank of Atlanta’s widely followed GDPNow index, which aims to track the economy in real time, has soared since later October. It reached 9.74% this week, suggesting that economic growth is rapidly accelerating from the 2.1% annual rate of the third quarter.

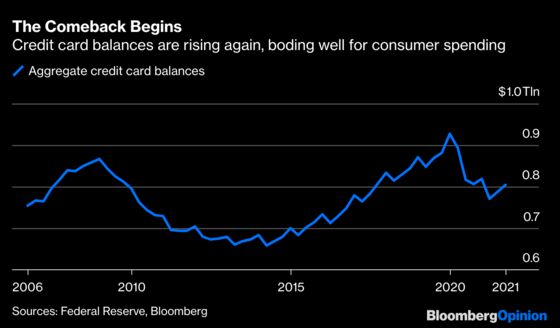

On top of that, consumer spending, which accounts for two-thirds of the economy, appears poised to accelerate. A survey by the Federal Reserve Bank of New York found that almost 27% of consumers said in October that they had applied for a credit card in the prior 12 months. That is the highest level since 2019 and well above the record low of 16% recorded a year ago, according to Dow Jones. Any sign that consumers are willing to incur debt suggests confidence is high. Indeed, the government’s monthly jobs report released Friday found that employment in the household portion of the survey — which differs from the survey of employers because it captures those who are self-employed and part-time workers — surged by 1.14 million in November, the most since October 2020.

How much of a potential tailwind from consumer spending are we talking about? Although credit card balances jumped by about $17 billion in each of the past two quarters, New York Fed data show they remain about $123 billion lower than at the end of 2019. That’s a lot of dry powder.

In sum, we have historically strong corporate earnings momentum, a booming economy and consumers who are ready to spend. Perhaps best of all, investor sentiment appears deeply negative. Why is that good? As Munger should know, his partner Buffett is fond of saying something to the effect that it’s wise for investors to be fearful when others are greedy, and greedy when others are fearful. That’s proved to be not such a crazy idea.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the executive editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.