Brexit Is a Sideshow for Pound Traders. Covid Is the Main Event

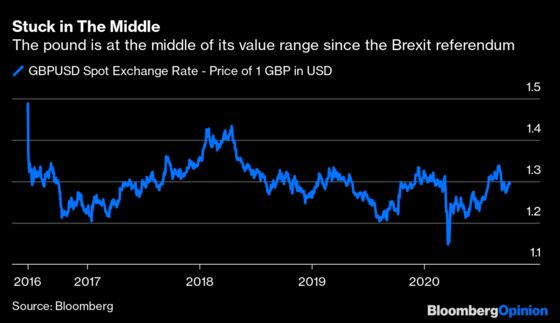

(Bloomberg Opinion) -- The recent strengthening of the pound toward $1.30 reflects rising market expectations of a post-Brexit trade deal between the U.K. and the European Union. Analysts from Citigroup Inc. were brave enough to say the chances are as high as 80%.

But even if you’re confident that Boris Johnson and Brussels will put aside their considerable differences and reach agreement over the next few weeks, would this really be such a golden moment for sterling assets? A pandemic-riddled British economy that’s staring at a second wave of lockdowns suggests otherwise.

U.K gross domestic product fell by a record 20% in the second quarter. While it rebounded in the third quarter, that doesn’t leave it in the same place. Growth is expected to be pretty flat over the next two quarters, meaning the economy is unlikely to recover to pre-Covid levels until 2022 at the earliest.

Until there’s a lasting relaxation of domestic freedoms, the consumer-supported British economy will struggle. During the pandemic, consumption as a proportion of GDP has dipped to about 60%, from close to 65% before, according to Bloomberg economist Dan Hanson.

Anything beyond “no deal” — and the implementation of World Trade Organization tariffs — will at least lift some of the pessimism that has swirled around Britain since 2016. But even a stripped-down trade deal, with minimal tariffs and quotas, would be a long way from the current U.K.-EU trading arrangement. Any relief rally for the pound and sterling-denominated assets is likely to be limited in its scope.

It’s similar for U.K. equities, as many of the companies in the FTSE 100 rely heavily on foreign earnings, which will be crimped by a stronger pound. Private equity buyers may be pushing up prices just now as they sniff around for bargains, as my colleague Chris Hughes highlights, but that’s being driven by sterling’s very cheapness. That demand may be capped by a rising pound.

The big technical reason for doubting that sterling will go much higher is found in the Gilt market, which has been given over to emergency pandemic funding. The market forecasts close to half a trillion pounds of Treasury issuance in the fiscal year to March 2021, nearly twice the previous record of 285 billion pounds ($369 billion) in 2008.

This supply onslaught is driving expectations for another 100 billion-pound slug of Bank of England bond purchases. Two of the BOE’s nine-member Monetary Policy Committee, Silvana Tenreyro and Jonathan Haskel, are willing to add more monetary stimulus and explore the benefits of negative rates. They’ll pick up support if the economy fails to recover.

Printing more money in this way will only ever lessen its value. Charging to park monies in a currency via negative rates would be another deterrent.

The value of the pound is therefore linked far more to the relative strength of any Covid recovery than any Brexit deal. Regardless of the success of EU negotiations, there will have to be substantive financial and economic reasons for overseas investors to buy sterling assets. The pound’s giddy heights before Brexit will be a steep mountain to reclaim.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.