(Bloomberg Opinion) -- Asset managers face “tough industry conditions with flows difficult to come by and fees under pressure,” says Standard Life Aberdeen Plc Chief Executive Officer Keith Skeoch. He’s not wrong; but competitors are weathering the ongoing storm far, far better than his firm is this year.

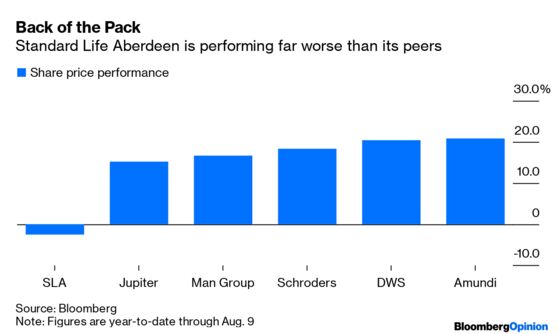

As the chart above shows, SLA’s performance this year is dismal, with its shares languishing at their lowest level since March. Last week Skeoch made his first solo outing at the top of the greasy pole, unveiling the company’s first-half performance five months after Martin Gilbert was moved to the vice chairman role following a couple of years as co-CEO of the firm he and Skeoch created in a merger. The numbers didn’t look good.

With $577.5 billion pounds ($700 billion) of assets under management at mid-year, it isn’t just the declining pound that’s prevented SLA from joining the $1 trillion club. Net outflows in the first six months of the year were 15.9 billion pounds; in the past two years, clients have pulled more than 87 billion pounds from the firm. The merger has turned out to be more of a distraction than a savior.

It’s not a good look when, a few minutes into your earnings conference call with analysts, you’re touting the recent appointment of a new head of human resources as one of the key leadership changes that will steady the ship. Asked on a media call on Wednesday about low morale at the company, Skeoch acknowledged that merging two different cultures has not been easy. “It’s something we take seriously and we’re working really hard at.”

Lackluster performance by SLA’s portfolio managers has taken its toll on customer appetite for its funds. By the end of June, 47% of the assets managed by the firm were trailing their benchmarks on a one-year basis. While that’s an improvement on the 53% that were underperforming at the end of last year, it’s not exactly going to help the sales force when pitching to customers, even though the three-year performance improved to 65% of assets beating their benchmark.

The most significant number associated with SLA, though, may be its market capitalization. At a smidgen over 6 billion pounds, its core business is valued at just 800 million pounds once you discount what it calculates are its 900 million pound stake in Phoenix Group Holdings Plc, the 1.5 billion pounds it has invested in HDFC Asset Management Co. and the 2.8 billion pounds it owns of HDFC Life Insurance Co.

The first stake arose from SLA’s February 2018 decision to sell its insurance business to Phoenix. SLA views it as a strategic holding, along with its 30% ownership of India’s HDFC Asset Management. But the latter has to increase its publicly-traded float to a minimum of 25% in the next two years, up from about 14% currently; SLA says it is likely to participate in that process. The 23% holding in India’s HDFC Life is deemed non-strategic and has already been reduced by more than 6% by sales earlier in the year (although SLA says it’s obliged to hold 9 percentage points until March 2021).

So let’s indulge in a game of fantasy M&A. Even at its reduced market capitalization of 6 billion pounds – down from almost 10 billion pounds a year ago – SLA would be a mouthful for even the most cash-rich of private equity buyers, especially after building in a takeover premium.

But there’s 5.2 billion pounds ($6.3 billion) worth of publicly-traded assets on the balance sheet. And while it would take time to find buyers for those shares, it isn’t too much of a stretch to envisage a couple of private equity firms viewing SLA as a break-up candidate and teaming up to dismember the firm.

Skeoch said last week that he’ll “remain focused on ensuring that we unlock the value of the assets on the balance sheet.” If he doesn’t get a wiggle on, he may find that others are more than willing to take SLA off the market and liberate those stakes for themselves.

To contact the editor responsible for this story: Stephanie Baker at stebaker@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.