‘People’s Fear Gauge’ Separates Truth From Turbulence

(Bloomberg Opinion) -- The next time it seems as if the sky is falling, pull up the trading volume in the SPDR S&P 500 ETF Trust (ticker: SPY) for a reality check.

Last Wednesday was one of those days. The S&P 500 Index was nearing a 3% drop, and it looked as if maybe this could be the Big One. It felt different this time. The yield curve had just inverted, which has a near-perfect record of predicting a recession. All was lost. Yet, late in the day, SPY’s volume was still a sleepy $38 billion, about half of what it tends to experience during intense sell-offs. SPY’s lackluster volume didn’t jibe with hardly anything else going on. Not the price drop, not the headlines, not the Twitterverse. It was pretty much alone in its quietude.

But the low volume turned out to be prescient — showing then in the darkest of hours what now seems obvious in retrospect: Traders and investors simply weren’t that concerned. The moderate volume also suggested that even the smallest catalyst would trigger a rebound. And it did. The market went up on Thursday after Wal-Mart earnings. It then rose 1.5% on Friday, too.

Wednesday provided yet another example of how SPY’s volume is truly a reliable fear gauge and a decent leading indicator. I’ve been using it for about a decade, and it’s proved to be a trusty tool in measuring the depth and breadth of fear as well as how much of the noise out there is, well, just noise.

The reason it works so well as a fear gauge is that SPY is the undisputed king of liquidity, with trading volume of about $20 billion a day on average — multiple times more than any other equity with an unparalleled amount of options tied to it as well. SPY has grown to be something of a sun in the middle of the equity solar system, with its volume acting as a thermometer of market activity and nerves.

It’s arguably a broader, more democratic version of the Chicago Board Options Exchange Volatility Index, or VIX, to which it is highly correlated. But unlike the VIX, which only measures activity of professional institutional investors, SPY measures the activity of all types of investors and is a fixture in portfolios. Because of its liquidity and low cost, it is used as a replacement for — and has attributes of — futures, single securities and mutual funds. Nothing has a broader and more diverse base of both domestic and foreign user base — institutions, traders, hedge funds, advisers and individual investors. From Bridgewater to Aunt Edna, everyone plays in this sandbox.

And when bad news hits, SPY tends to be the first thing many investors reach for, especially when they get blindsided and have no time to run analysis or want to quickly tweak their exposure, or get short the market, without disturbing their other investments. In addition, when implied futures funding costs rise, it tends to chase more traders to SPY, lifting its volume. If and when the fear spreads beyond the itchy-trigger-finger trading crowd to the steadier-handed advisers and retail investors, volume will start to boom in SPY.

The threshold that tends to separate major freak-outs (my technical term) from the more short-lived, garden-variety sell-offs that tend to have quick rebounds is $60 billion. On days when the volume surpasses that amount, the market has a negative return on average in the following month.

There have been no days above $60 billion this year. This is in contrast to last year, when there were a few — namely around “Volmageddon” in February, when SPY traded $80 billion and $93 billion on back-to-back days. The fear was for real and arguably foreshadowed what ended up being the first down year in the market in a decade. Although 2018 couldn’t hold a candle to 2008, which is still the undisputed champ in $60 billion-plus days.

Over the past 10 years, SPY’s volume has also highlighted the difference between a sell-off related to geopolitics, earnings, trade or whatever President Donald Trump has tweeted most recently and one related to the Fed. The first tends to be like a flesh wound while the other is akin to an existential crisis. It seems that as long as the market thinks the Fed has its back, sell-offs tend to be short-lived regardless of the breathless headlines.

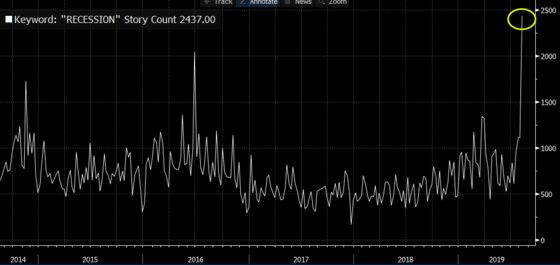

But what made last Wednesday a new kind of test for the “People’s Fear Gauge” is that the media coverage was so especially dark this time around. This was more than just the usual Trump tweet or trade war-type hysterics. This one involved the “R” word thanks to the inverted yield curve. In fact, the media mentioned the word “recession” much more last week than it had in years. My Bloomberg Opinion colleague, Mohammed El-Erian, even worried that these “alarmist headlines” could cause real damage to investor psychology and the economy.

But it turned out people largely ignored it all. The SPY volume sent a clear signal, but then the flows and the subsequent rebound backed it up. I also did an informal Twitter poll that showed that three-fourths of investors did nothing to alter their portfolios over the past few weeks.

This showed a clear disconnect between investors and the media. So, who’s right? I’ve heard some say investors are too used to buying the dip and leaning on the Fed and are missing the signs of a significant correction. I’ve also heard some say that the media has lost its effect on investors by overplaying the negative too much. Maybe it’s a little bit of both.

Whatever the truth, SPY’s volume can be a reliable in-the-moment way to measure the gap.

Concerns have also been raised about the possible manipulation of the VIX by monster trades. The Cboe has attempted to refute them. But I’m not here to take down the VIX, just to share my discovery of a complementary gauge.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Eric Balchunas is an analyst at Bloomberg Intelligence focused on exchange-traded funds.

©2019 Bloomberg L.P.