(Bloomberg Opinion) -- Traders who make a living betting on mergers still won’t touch T-Mobile US Inc. and Sprint Corp.’s deal with a 10-foot pole. The wireless carriers may have been able to butter up two federal regulatory authorities by using the wonders of a 5G-powered America to distract from their deal’s likely competitive harm. Even so, merger-arbitrage traders live in a world of mathematical probabilities informed by laws and legal precedents, and on that basis, it’s hard to imagine that the judge presiding over a case brought by a group of state attorneys general opposing the deal will rule in the companies’ favor.

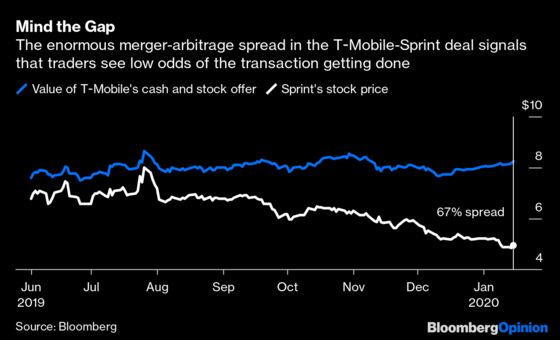

Lawyers for both sides each delivered closing arguments Wednesday, with a decision from U.S. District Judge Victor Marrero expected to come some time in February. Analysts largely view the odds as a toss-up, if not slightly tipped in T-Mobile and Sprint’s favor. But the equity market paints a meaningfully different picture: The per-share value of T-Mobile's offer is 67% higher than where Sprint's shares are trading, by far the biggest spread of any pending U.S. deal. The wide gap implies that traders see an extremely low likelihood that the transaction gets done, and Sprint options activity is sending the same signal.

Of course, this also means that if the companies do win in court, some traders popping antacids right now stand to make a substantial return. But for the most part, arbitrageurs have chosen to stay away.

“This is one of those seminal situations in merger arb history,” said Roy Behren, a portfolio manager for the Merger Fund at Westchester Capital Management, which oversees $4 billion of assets. He found T-Mobile and Sprint’s arguments persuasive — that together the companies will be able to build out a nationwide 5G service faster, and that Sprint doesn't have the capital or scale it needs to compete. But the potential downside is painfully large, and so it’s simply too hard to make a bet on what will happen. “We like the case, but that doesn’t mean we want to risk shareholders’ money on something where we don’t have a huge conviction,” Behren said in a phone interview.

The case may come down to Dish Network Corp. and its assigned role in ensuring the U.S. wireless market remains competitive. Makan Delrahim, the head antitrust enforcer at the Department of Justice, is placing incredible faith in Dish that it can fill the hole Sprint leaves behind and become a formidable new competitor to T-Mobile, AT&T Inc. and Verizon Communications Inc., even though it will most likely take years for Dish to live up to those expectations.

T-Mobile has relied heavily on the argument that its brand as the customer-first “Un-carrier” means it can be trusted not to raise prices in the meantime, Blair Levin, an analyst for New Street Research, wrote in a report this week. The idea is that with Sprint, it will be able to spread out its network costs across a larger subscriber base and thus keep plan rates low. But as the state attorneys general have noted, AT&T and Verizon have greater scale and higher prices.

Judges look at facts and precedent. Just as there was a compelling case to make against AT&T acquiring Time Warner last year in what amounted to a massive vertical consolidation of market power, it was hard to articulate this with facts and not just speculation about what might happen, because of the lack of precedent. The judge in that matter said early on, “I guess I have to get a crystal ball,” which judges do not like to do, and sure enough, he opted to stick with the facts as they were.

The Justice Department and Federal Communications Commission have already given their blessing, which carries weight and could mean Judge Marrero will, too. But then if they could look in a crystal ball and see the consequence of doing so, they may not like what they see. Even the stock market knows that the deal shouldn’t go through.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering the business of entertainment and telecommunications, as well as broader deals. She previously wrote an M&A column for Bloomberg News.

©2020 Bloomberg L.P.