British Billionaire Mike Ashley Shows How Not to Set CEO Pay

(Bloomberg Opinion) -- If you own a large retailer and you’re trying to make your future son-in-law chief executive officer, offering him a potential 100 million-pound ($137 million) bonus is probably not the best way to get other shareholders on board.

Yet that is what’s being proposed at Frasers Group Plc.

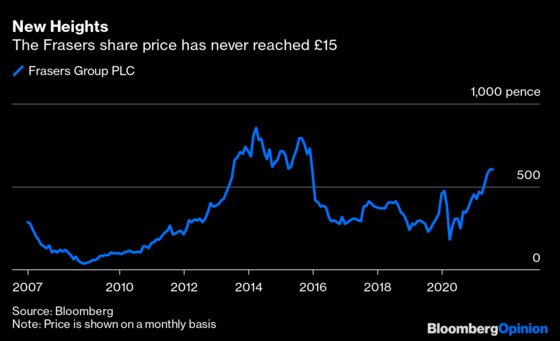

The British owner of the Sports Direct and House of Fraser chains said earlier this month that Mike Ashley, founder and majority shareholder, was preparing to hand over the CEO role to 31-year-old Michael Murray, the man engaged to his daughter Anna. On Wednesday, Frasers said Murray could receive 100 million pounds worth of shares if he succeeded in raising the stock price to 15 pounds. The shares closed at 656.5 pence, up 1%, on Thursday.

When the succession arrangement was announced, I argued that Murray’s pay package should resemble that of any external appointment. The proposed large bonus doesn’t fit that bill. Murray’s remuneration should reward him for the value he delivers for all shareholders, not just Ashley. Although the incentive has the potential to enrich all investors, Ashley would be the biggest beneficiary. He has a 65% stake in Frasers.

The 15-pound target is certainly a stretch, and Murray has just more than three years to achieve it, whereas five years is a more usual timeframe. If he assumes the CEO role — and his appointment has not yet been finalized — he would start in May next year. The stock price would then have to be at 15 pounds for 30 consecutive days before Oct. 7, 2025.

Frasers shares have never achieved this level before. The closest they came was at less than 10 pounds — at 922 pence in April 2014.

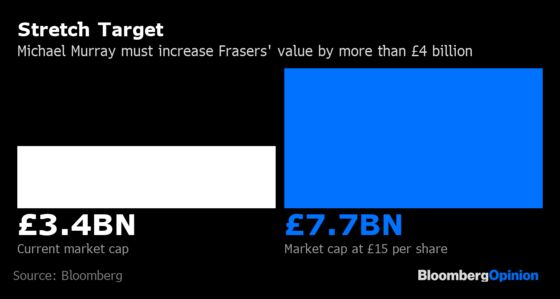

Should they reach 15 pounds, Frasers’ market capitalization would increase from 3.4 billion pounds to 7.7 billion pounds. Murray’s 100 million pound bonus would be about 2% of the value created.

But how can minority investors be sure that the value creation is driven by Murray? Ashley, who built the business, will remain an executive director and his majority shareholding means he will continue to be in the driver’s seat. There’s also a risk that Frasers reaches the share price target due to factors outside of Murray’s control, such as takeover interest. Just look at the bidding frenzy around U.K. supermarkets right now. The circumstances could make it hard to justify rewarding Murray so richly.

Frasers executives have typically had low base salaries, with the potential top-ups through big share-based incentives. But the same can’t be said for Murray: The group also proposed a 1 million pounds a year salary. Even if it deducts this from a 100 million-pound pay-out, his annual salary would still be more than that of Steve Rowe, the CEO of Marks & Spencer Group Plc, a retailer with almost three times the sales of Frasers. (As CEO, Ashley does not receive a salary.)

The proposed bonus for Murray will be put to shareholders at Frasers’ annual meeting next month. If it gets a frosty reception, it would not be the first time the company’s pay plans have run into trouble. Shareholders twice voted against Ashley sharing in a 200 million-pound employee and management bonus pool. They eventually approved it in 2014, only for him to pull out of the arrangement two weeks later.

It’s worth remembering that Frasers has led the way in rewarding employees throughout the organization. In 2013, thousands of staff of Sports Direct, as the company was then known, shared 135 million pounds worth of shares. They received another 43 million pounds in 2017, and last year Frasers put in place a new 100 million-pound reward program, contingent on the share price reaching 10 pounds. It would be a shame to undermine this system with a controversy over outsize executive rewards.

Given Murray’s closeness to his family, Ashley should abstain from the votes on his pay at the annual meeting.

But perhaps the easiest way for Frasers to avoid a row with investors over this or any future arrangements would be for Ashley to buy out minority shareholders. I’ve long said that the group would be best run away from the glare of public markets. If Ashley wants to introduce private equity style remuneration, then he should have a private ownership structure too.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2021 Bloomberg L.P.