(Bloomberg Opinion) -- Rising bond yields have been unkind to growth stocks. Their impact on the special purpose acquisition companies has been downright cruel. The SPAC boom has become the Spacpocalypse. Nobody should be surprised.

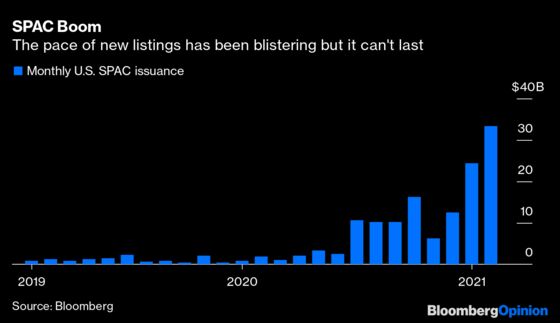

SPACs are listed cash-shells that merge with private businesses in order to take them public. They’ve become the dominant way for a company to raise equity finance in the U.S. — well over 200 new blank-check companies have raised a mind-boggling $70 billion so far this year, according to data compiled by Bloomberg.

The trend has attracted a laundry list of financiers, celebrities and sports people. There’s so much money sloshing around, and it’s been so easy and fun to reap riches with them, that sponsors no longer bother to give them imaginative names. A recent one is simply called Just Another Acquisition Corp.

As with every mania, prices became divorced from fundamentals. Now, the hangover’s kicking in: The IPOX SPAC index fell 20% since a February peak, meeting the technical definition of a bear market.

Given what’s happening in the bond market, investors have become unwilling to pay through the nose for speculative stocks. A future stream of earnings is worth less in today’s money if a higher discount rate is applied; higher rates also provide investors with other options for their cash.

Dozens of SPACs are now trading below the $10 price at which they sold shares. That’s more like how things should be. In a “normal” market, SPACs would sell for roughly the per-share value of the cash they hold, at least until they’ve announced a deal. Yet until recently many SPACs were immediately trading at a large premium to their cash holdings. That didn’t make much sense. Was it really likely they’d all find attractively priced deals that would justify paying so much?

Churchill Capital Corp. IV ($CCIV to its boosters on social media) traded as high as $65 before it revealed the terms of its deal with Lucid Motors Inc. Its shares have since fallen more than 60%.

Even with prices crashing like this, SPACs have so far been able to keep raising capital. However, their IPOs are no longer massively oversubscribed. If freshly minted SPACs stop “popping” when they start trading, hedge funds will become a lot more discerning about which ones they furnish with money. As I’ve explained, arbitragers often flip SPACs for a quick profit and aren't long-term shareholders. Falling prices could also make life harder for SPACs trying to complete acquisitions.

“The SPAC market has taken a real beating,” serial SPAC launcher Palihapitiya said on his podcast on Saturday. “If you have one or two more months of this where all of a sudden bonds look better… you’ll have a bunch of busted IPOs or mergers.”

With SPACs soaring too far for their own good, other hedge funds have begun shorting them, borrowing and then selling the stock in expectation the price will fall so they can buy it back cheaply and pocket the difference. SPACs that have completed deals and thus no longer enjoy downside protection are a favorite for the shorts. (Until a merger has gone through, shareholders can elect to redeem their SPAC holdings for cash and the interest that’s accrued.)

“Once they become operating companies, you’re seeing certain [ex-SPAC] securities that have bubble-like characteristics,” Jonathan Segal, co-chief investment officer of Highbridge Capital Management LLC told a JPMorgan Chase & Co. podcast last month. “We’re finding ways to make money on the short side in that space, and I think others probably are too.”

Muddy Waters Capital LLC launched a short attack on XL Fleet Corp., a commercial vehicle supplier, last week, while Hindenburg Research recently targeted Clover Health Investments Corp. Hindenburg didn’t actually short Clover, fearing a GameStop Corp.-like reprisal. Even so, Clover shares are trading more than 20% below the level at which the Palihapitiya SPAC it merged with sold shares.

Former SPACs have also announced disappointing financial results: Nikola Corp., which Hindenburg targeted last year, said it would produce fewer than 20% of the electric trucks it had planned to build this year. I’ve warned before about how the optimistic forecasts SPACs make may lead to disappointment.

There’s also been a broader reality check in early-stage electric vehicle stocks, one of the sectors that’s been most favored by SPAC sponsors. Quantumscape Corp. and Hyliion Holdings Corp., two former SPACs I’ve written about, have lost more than two-thirds of their value since peaking last year. It underscores what academics who’ve studied SPACs have been saying for a while: the performance of SPACs post-merger is often disappointing.

There are other factors signaling the end to this bull run. With all the money flowing into the sector, SPAC sponsors have become less generous: typically the blank-check units sold at IPO come with share warrants conveying the right to purchase the stock once it reaches a certain price. However, some SPACs have stopped including them, depriving the hedge funds of their free lunch. Insiders have been selling too: Palihapitiya sold a large chunk of Virgin Galactic Holdings Inc. stock last week.

The SPAC market has gone through cooling off periods before. The good news is that there’s less risk of losing money with SPACs trading closer to the value of the cash they hold. However, wannabe Wolfs of Wall Street still hoping to launch theirs could find they’re too late. The party’s over, at least for now.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2021 Bloomberg L.P.