(Bloomberg Opinion) -- Diamondback Energy Inc.’s stock air-dropped earlier this month after the company shocked investors with disappointing earnings and production problems. It doesn’t help that oil prices have been in the doldrums since June and 2020 looks dicey. So it can hardly be surprising that, in its latest sale of 10-year debt, Diamondback was forced to pay up with a yield of … 3.55%.

Those bond vigilantes are merciless.

OPEC may regard America’s frackers as its nemesis, but the true enemy of the oil exporters’ club has been U.S. capital markets (see this). The latter’s willingness to adopt a venture-like role of financing an enormous, and largely loss-making, grab for market share in global oil and gas has been the critical force of the past 10 years. The tumult of that decade in energy markets suggests we can hardly expect the next one to be placid. So Diamondback’s ability to secure funding through 2029 at a spread to Treasuries of less than 2% seems like further confirmation that OPEC’s real arch-enemy remains as defiant as Monty Python’s Black Knight.

The Black Knight is showing some signs of fatigue, however.

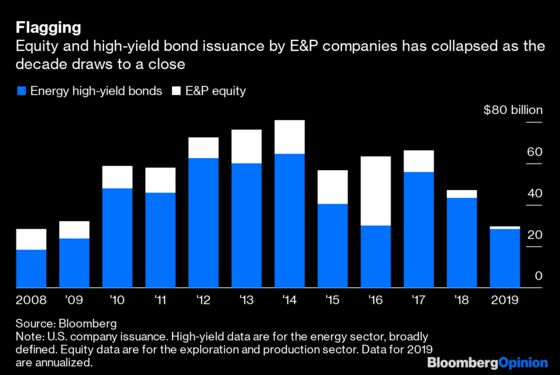

The energy high-yield bond market has tightened severely again; at 785 basis points, the option-adjusted spread to Treasuries is at its widest in more than three years (before the initial supply cuts from OPEC+). Likewise, on the equity side, the SPDR S&P Oil & Gas Exploration & Production ETF is trading close to its lowest level since it launched in 2006. Haynes and Boone LLP, which tracks bankruptcies in the sector, noted in its latest report that the pace had picked up this year, with the majority of filings happening since May.

That Diamondback was able to issue $3 billion of new bonds at very attractive rates anyway gets at something going on beneath the headline collapse in sentiment. Namely, the gap between haves and have-nots when it comes to leverage in the shale patch appears to be widening. Diamondback is a high-yield issuer; but, rated Ba1 by Moody’s Corp., it is scraping investment grade (and has recently been upgraded to investment grade by Standard & Poor's). With net debt of 1.8 times Ebitda, its leverage isn’t low but also isn’t high by the standards of the sector.

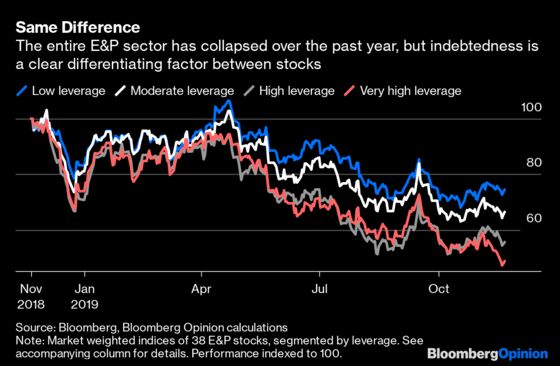

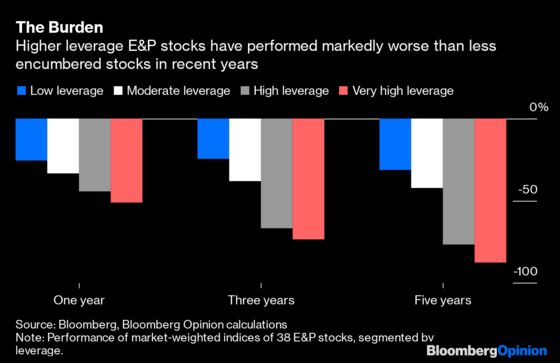

The gap between the four groups really opens up in May, coinciding with oil rolling over after a spring rally. While leverage may have changed for each of the companies over time, the relative performance over the past year fits with the longer picture.

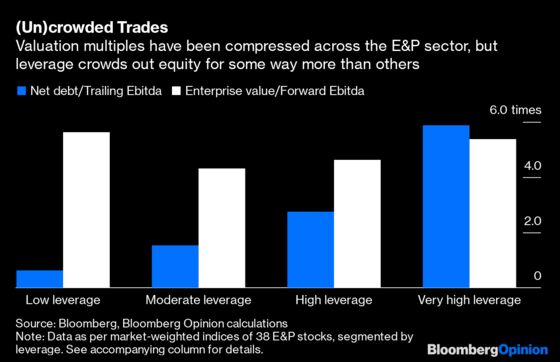

Despite markedly different performances, the broad sell-off in E&P stocks has compressed average valuation multiples for the groups into a narrow range. Crucially, however, the spread between those multiples and reported leverage tells the story of where the vast majority of the equity value in E&P has migrated:

The leverage gap between E&P companies, and the growing disparity in their access to capital, should curb the anticipated growth in U.S. oil production in 2020. It also suggests conditions for consolidation in shale-land — largely elusive until now — are ripening. That said, given the market’s reaction to acquisitions so far, valuations will likely need to drop lower before larger companies with better balance sheets take the plunge (ConocoPhillips’s recent analyst day certainly suggests so).

Looking at all this, you might expect that when OPEC members gather in two weeks’ time, they could conclude it’s best to hold off and let this all play out. The only problem? Most of them aren’t in great shape either.

Updated to add Diamondback’s S&P credit-rating upgrade.

The four groups are: as follows. Very high leverage (net debt >3x Ebitda) comprising Antero Resources, Chesapeake Energy, Comstock Resources, EQT, Laredo Petroleum, Noble Energy, Oasis Petroleum, Range Resources. High leverage (2-3 x Ebitda) comprising Apache, Callon Petroleum, Carrizo Oil & Gas, CNX Resources, Matador Resources, QEP Resources, Southwestern Energy. Moderate leverage (1-2x Ebitda) comprising Berry Petroleum, Centennial Resource Development, Cimarex Energy, Continental Resources, Diamondback Energy, Diversified Oil & Gas, Jagged Peak Energy, Marathon Oil, Murphy Oil, Northern Oil and Gas, Parsley Energy, PDC Energy, SM Energy, SRC Energy, Talos Energy, W&T Offshore, WPX Energy. Low leverage (<1x Ebitda) comprising Cabot Oil & Gas, Devon Energy, EOG Resources, Magnolia Oil & Gas, Pioneer Natural Resources, Riviera Resources.The aggregate data presented are weighted by market cap in each group. Four companies (one in each group) have been removed due to their outsized weighting. They are (in order of leverage from high to low): Occidental Petroleum, Concho Resources, Hess, ConocoPhillips.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.