Slack Poised to Join Cloud Valuations Soaring Into Thin Air

(Bloomberg Opinion) -- Slack Technologies Inc. couldn’t have picked a better time to go public. Investors have lost their minds about software companies.

Earlier this year, I wrote about how stock buyers were willing to pay handsomely to own shares of fast-growing companies that sell cloud software to businesses. As investors had grown antsy about the FAANGs — the elite technology superpowers such as Apple Inc. and Google parent company Alphabet Inc. — the software PUTIN stocks, as I semi-apologetically called them, were ascendant. Since then, investors have warmly greeted new stock listings by even more business software firms including Zoom Video Communications Inc., Pagerduty Inc. and CrowdStrike Holdings Inc.

I went back to my self-selected cohort of 17 business software firms that included Salesforce, Adobe, Atlassian and ServiceNow. The median stock multiple of my cohort, which I had to adjust slightly because of acquisitions, didn’t budge much since the February analysis.

The median market value adjusted for cash and debt was about 10.3 times a blend of revenue estimated in the next year, compared with 9.8 times in February. The price-to-earnings multiple of the S&P 500 index has also increased since then. What really stood out was the top-tier companies in my PUTIN index have grown even more bubbly.

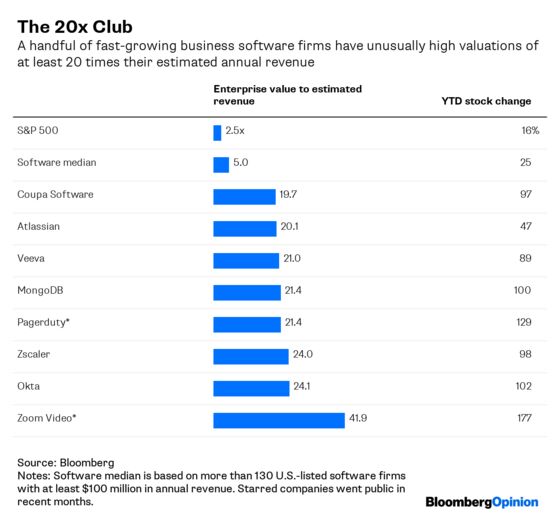

Look behind the velvet rope to find the 20x Club, the most popular hot spot in stock markets. More than half a dozen software firms now have enterprise values that are more than 20 times expected revenue in the next year, according to Bloomberg data.

That is — to put it mildly — not normal. Relative to revenue, buying a share of pharmaceutical software firm Veeva Systems Inc., a member of the 20x Club, is four times the price of Alphabet, one of the dominant companies of this generation.

Some of the members of the 20x Club are newly public, and it’s not unusual to see young companies with stock market values that are a bit out of whack. But 20x Club members also include Veeva, Atlassian Corp., Okta Inc., MongoDB and other companies that have been public for 18 months or more. As corporate-messaging service Slack plans to list its shares Thursday in a not-IPO, it may join this elite crew. A valuation for Slack of $17 billion or so would work out to an enterprise value to forward revenue in the ballpark of the 20x Club.

There are understandable reasons these business software firms, which are relatively unknown by normal humans, have become darlings of the stock market and technology investing. Something real and seemingly permanent is changing in how companies large and small buy technology.

Companies are desperate to modernize their technology so they don’t get left behind and can take advantage of growth opportunities, and that has made them open their wallets to buy new types of internet-friendly, easy-to-use software that promises to help make their marketing spending more efficient, catch cyberattacks before they cripple systems or enable seamless communications among far-flung employees.

I’m not yet convinced that these young cloud software companies can ever grow as large as their investors believe, particularly if an economic downturn forces companies to rationalize their technology budgets. But software truly is eating the world, and that has accrued to the benefit of both titans such as Microsoft and relative newcomers like the members of the 20x Club.

At the same time, investors are desperate for growth, and business software firms are delivering it in spades. They can also be relatively easy to understand — they sell software in exchange for cash — and businesses have proved to be relatively reliable consumers, unlike people and their tendency to flit from one hot internet thing to the next. And now that superstar tech companies have run into regulatory problems, been hit with tariffs or otherwise have more question marks than before, a bet on a company selling software that an antitrust lawyer would never notice suddenly looks like a good idea.

The question is what that promise costs. As stock buyers pay more relative to a company’s revenue, any wobble in growth can result in a crash, and investors’ room for error narrows when stock prices are already high relative to a company’s financial prospects. High stock valuations may also deter some needed consolidation in business software. It has become fashionable not to care about valuation, but there can be a high price to bubbles in share prices.

Of course, I could have called a bubble in business software stocks at multiple points in the last decade and it would have been accurate in the moment yet completely wrong. An index of mostly business software companies, the BVP Nasdaq Emerging Cloud Index, has more than quintupled since 2013, compared with a 74% gain for the S&P 500 over the same period.

It’s true that 10 years into an unprecedented bull market in stocks, unusual valuations are par for the course. Maybe the bubble for business software firms will never end, or stock prices of these highflying software firms will deflate slowly rather than blow up. Maybe. Or there may be a high price to pay for software companies in an unprecedented stratosphere.

No, I am not sorry at all. I will say, however, that the "U" in PUTINs, Ultimate Software Group Inc., was sold in May to an investor group. My acronym is broken.

Yes, these software companies tend to be valued as a multiple of revenue rather than profits. In many cases they don't have profits.

Bloomberg Beta, the venture capital arm of Bloomberg Opinion parent Bloomberg LP, is an investor in Slack.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.