(Bloomberg Opinion) -- The arrival of vaccines carries hope that an end to the pandemic may be in sight. But even after the health crisis is brought under control, governments will have to continue dealing with the economic consequences.

Two primary concerns have emerged: The first is addressing the inequalities caused by lockdowns and other social-distancing measures. The pandemic has caused a deep bifurcation in the economy, with some able to work comfortably from home while others have had to close shop. As a result, many clerical workers saw their savings rise, while others — waiters or stagehands, for example — ended up on government support.

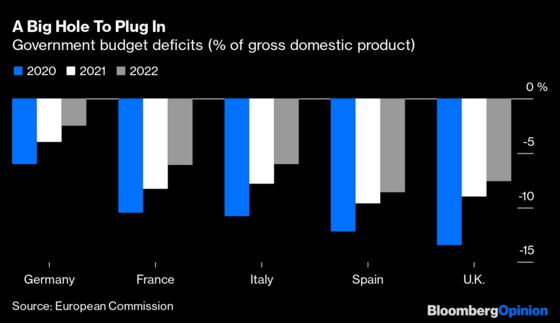

The second issue is how to improve the state of public finances, which have deteriorated as a result of huge increases in public spending and sharp drops in tax receipts. The European Commission expects the euro area as a whole to run a budget deficit this year equal to 8.8% of its gross domestic product, with some countries such as France, Italy and Spain, hitting double figures. In the U.K., the deficit is projected to amount to 13.4% of GDP.

A growing number of economists are recommending a one-off wealth tax as a tool to help solve both of these problems. However, if governments decide to raise more revenue by taxing rich people’s property and bank accounts, they’d be wise to avoid rolling it out too soon. Otherwise it could help deepen the ongoing slump.

Last week a high-profile report suggested that a one-off 5% wealth tax in the U.K., aimed at households owning 1 million pounds ($1.4 million) or more, could raise 260 billion pounds (about $350 billion). That’s the equivalent of raising VAT by 6 percentage points. A more selective measure, aimed at households with more than 4 million pounds in assets, would still bring in 80 billion pounds. In its latest World Economic Outlook, the International Monetary Fund has also recommended higher taxes on richer individuals — including taxing high-end property, capital gains and wealth — to reduce public debt.

I’m generally skeptical of the case for wealth taxes, for both conceptual and practical reasons, as there are more effective means at reducing inequality. However, I can see why a government would want to introduce a one-off levy on the rich after an extraordinary shock such as a pandemic or a war. These events have drastic effects on the economy and affect some individuals far worse than others.

The main problem right now is that it’s too soon to be talking about a wealth tax. The pandemic is still in full swing across Europe. Economies are suffering as governments maintain strict Covid restrictions. Although the U.K. and other governments are thinking about how to raise extra revenue in the future, they needn’t worry about this for now. They can still borrow at very low rates thanks to central banks capping sovereign bond yields with quantitative easing. A wealth tax would simply depress spending at a time of shrinking economic output.

What’s more, the pandemic hasn’t affected even “the rich” equally. Yes, 2020 was an excellent year for most tech companies such as Amazon.com Inc. and their shareholders. But if you own a hotel on the Amalfi Coast in Italy, the past few months have been a washout. Would it be fair for the government to hit those wealthy individuals who’ve had to close down their businesses and suffer heavy losses? Perhaps it would be better to tax those on fixed incomes, such as pensioners and employees who’ve been able to easily work from home. Wouldn’t they be more in debt to society?

A wealth tax would only hit the right target after the economy has recovered: Only then will we have a more representative view of the state of individual finances.

There will be a time for redistribution. But, for now, governments must focus on ensuring effective vaccine distribution and supporting the economy via well-targeted measures and effective public investment programs. Let’s think about growth now — and come back to that wealth tax later.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2020 Bloomberg L.P.