Saudi Aramco's IPO Birthday Party Crashed by the UAE

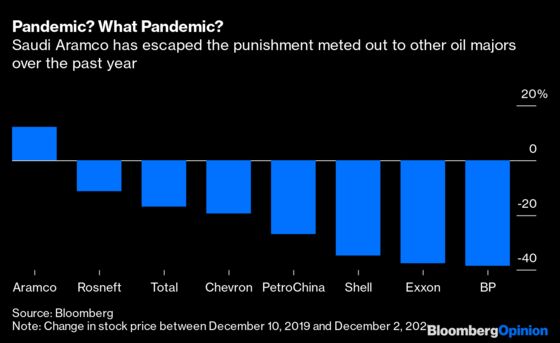

(Bloomberg Opinion) -- The word “pandemic” didn’t appear among the risk factors in the prospectus for the world’s biggest IPO, Saudi Aramco’s, which marks its first anniversary this weekend. It turns out that didn’t matter: Despite Covid-19’s savaging of the oil market, shares of Saudi Arabian Oil Co. now trade 12% higher than where they debuted. Others haven’t fared so well.

To put that gain in perspective, the $200 billion or so added to Aramco’s market cap during the worst-ever slump in oil demand is bigger than the current market cap of Exxon Mobil Corp.

Yet the unusual nature of that resilience makes it weaker than it appears. And this is reinforced by the coincidence of the anniversary with a meeting of OPEC+ that was overshadowed by disagreement between Saudi Arabia and the United Arab Emirates.

Aramco isn’t quite at Crown Prince Mohammed Bin Salman’s magic $2 trillion level (it hit that briefly soon after the IPO), but its premium has expanded this past year. Even at the start, Aramco’s $1.7 trillion valuation looked rich (see this and this). One global catastrophe later, it looks even richer.

Aramco’s scale and low costs enable it to ride out the storm better than everyone else. Free cash flow of $51 billion through the third quarter was more than double the combined total for all seven of the peers in that chart.

But the increase in absolute and relative valuation despite an inarguable deterioration in financial performance and macroeconomic conditions points to a big reason for Aramco's apparent invincibility: its miniscule, domestic-only float.

Saudi Arabia pulled back from earlier plans for an international listing. Foreign money managers wouldn’t buy the $2 trillion headline valuation prestige demanded. Saudi citizens, who are long oil by default, were provided access to loans to participate, akin to borrowing money so you can fill your 401k with shares in your employer.

The ouroboros-like dynamic has continued. In June, Aramco completed its acquisition of the 70% of chemicals giant Saudi Basic Industries Corp. previously owned by the state for $69 billion. It’s notable that the deal was completed at all, let alone at its original price, despite the intervening pandemic. Forecast 2020 earnings for Sabic collapsed by more than 75% between announcement and closing.

Similarly, the $75 billion annual dividend touted for the IPO goes mostly to the state, and even mighty Aramco now borrows to cover it (and likely will keep borrowing for a few years if consensus forecasts are prescient) . The company isn’t struggling anything like a similar borrower, Exxon, but the $93 billion swing in its balance sheet is striking.

Saudi Arabia’s approach with its national oil champion stands in marked contrast to that of its neighbor and (usually) close partner, the UAE. The rift that has opened up between the two on OPEC+ policy is rooted in this.

Both countries have shaken up their oil sectors in recent years as prices crashed and speculation about peak demand mounted. Saudi Arabia erred on the side of a big splash, but in a small pool, with the Aramco IPO. The UAE has taken a more nuanced, but in some ways more far-reaching, approach.

Rather than list shares in Abu Dhabi National Oil Company, or Adnoc, on the domestic market, the state has carved out deals to bring in both domestic and foreign investors for specific subsidiaries. This summer, it raised $10 billion by selling a 49% stake in a network of gas pipelines to a consortium of heavyweight funds, including Global Infrastructure Partners, Brookfield Asset Management Inc. and Ontario Teachers’ Pension Plan. That followed deals in recent years including a $4 billion sale of a 40% stake in Adnoc Oil Pipelines to KKR & Co. and BlackRock Inc.; a $5.8 billion sale of a stake in Adnoc’s refining unit and a $550 million sale of 5% of its drilling business to industry buyers; an IPO of its fuel distribution arm, raising $850 million; and awards of drilling concessions to foreign oil companies.

The proceeds are north of $20 billion, which compares quite favorably with the $29 billion raised in Aramco’s IPO. More importantly, the UAE raised this cash by targeting individual assets toward the specific types of investors, both domestic and foreign, most likely to pay up for them, all while maintaining control. At the same time, Adnoc is investing heavily in boosting its oil-production capacity — hence its growing frustration with the OPEC+ supply cuts. The UAE’s opportunity cost of restraint is effectively subsidizing many weaker members of the group.

All of this represents a fundamental change in the UAE’s approach, says Ben Cahill, a senior fellow at the Center for Strategic & International Studies, a think tank. “They’ve decided to produce more oil now and capitalize all parts of the value chain,” he says. Such a strategy would be consistent with positioning for the threat of peak oil demand. “The old concept of keeping oil in the ground for future generations is now questionable,” Cahill adds. Similarly, it makes sense to reduce exposure to energy infrastructure that may be nearing the end of its useful life. The overall concept is ultimately bearish for oil and OPEC+, though not necessarily for the UAE’s revenue if it raises capital and also wins market share.

Aramco’s IPO was ostensibly driven by similar thinking around diversifying the economy. Yet the offering itself, along with the first year’s resort to raising more quasi-sovereign debt to effectively funnel cash to the state, leave much to be desired on this front.

As has always been the case, Aramco’s commercial imperatives can clash with its national obligations, which include facilitating Saudi Arabia’s role as the de facto leader and swing-producer of OPEC. This dual identity is a hindrance to capitalizing fully on its value — with an international listing, for example — as opposed to enjoying the symbolism of a high headline value. And as the UAE treads further along a divergent path, that tension only becomes more apparent.

Aramco's dividend payments to public shareholders are guaranteed for five years after the IPO. The state's dividend is not and Aramco could, in theory, reduce that if necessary. In practice, that would add pressure to the government's finances, since Aramco's royalties, taxes and dividends provide the majority of public revenue.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.