What's Another Quarter Really Worth to Saudi Aramco?

(Bloomberg Opinion) -- January will mark the fourth anniversary of Crown Prince Mohammed Bin Salman’s bombshell announcement that Saudi Arabia would sell shares in its enormous national oil company. And after the latest delay to that process, January may also be when those shares actually get sold.

The meandering IPO process for Saudi Arabian Oil Co., or Saudi Aramco, has accelerated this year. Which makes the latest delay, mere days ahead of the expected launch, feel especially abrupt. One reported rationale for this is apparently so the bankers can incorporate third-quarter numbers into the valuation. You may recall this was a particularly eventful three months for Aramco, what with an unprecedented strike on critical oil facilities in mid-September. Even so, it feels like an odd reason to slam on the brakes now.

The third quarter was, if anything, a lackluster one for Big Oil. Consensus earnings estimates for the international majors have been drifting down since July and dropped sharply in the past two weeks. Brent crude oil averaged about $6.50 a barrel less than the prior quarter, and benchmark petrochemical margins were also lower. Refining margins perked up a bit, but they account for a small fraction of Aramco’s profits anyway. Plus, even before the explosions at Abqaiq disrupted supply, Aramco’s crude oil production was averaging the same sub-10 million a day level it has held since March.

The added twist here is September’s attack. There’s an argument that Aramco must demonstrate to prospective investors that it came through this trial-by-missile without too much damage to its financials. Holding off a bit longer lets the company print a set of results displaying such resiliency (not to just the explosions but also that weak commodity backdrop).

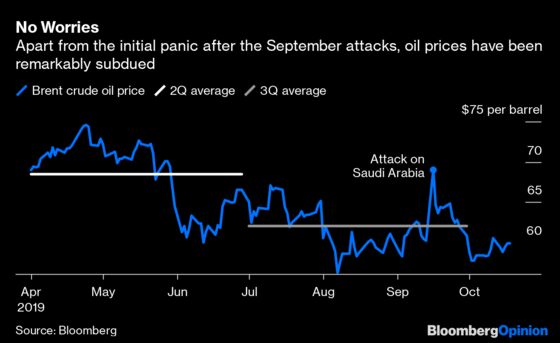

On the other hand, it doesn’t feel like there’s a ton of trepidation out there about Aramco’s ability to absorb the attacks. We know this because oil prices are lower now than they were before the missiles began flying:

Oil prices wouldn’t be kicking their heels around $60 if there was widespread belief Aramco had been crippled for an extended period of time. The paradox here is that a big reason for the weaker commodity backdrop in the third quarter is Aramco’s rapid action to calm nerves by maintaining supplies to customers and working around the clock to repair damaged infrastructure.

That will have come at a cost to Aramco, obviously, so it could still be argued investors need evidence that wasn’t too steep. But subdued oil prices and Aramco’s own announcements point to the disruption being temporary. Moreover, as I wrote about here, favorable changes to Aramco’s royalty rates and the institution of a five-year preferred payout policy for minority shareholders mean such temporary effects wouldn’t really impact the all-important outlook for dividends anyway.

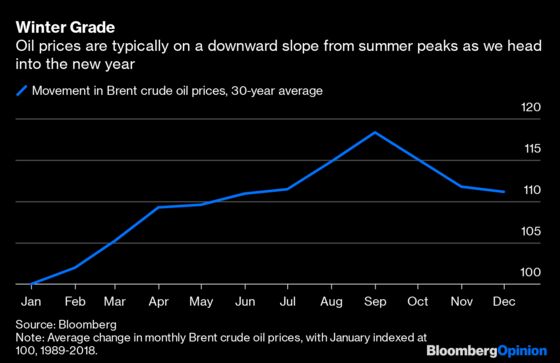

Delaying the IPO also carries potential costs. Arresting momentum for any IPO is to be avoided if possible, especially when it carries a certain déjà vu. Plus, the turn of the year is seasonally weaker for oil prices, looking at long-term averages:

These are just optics, obviously. The price of oil on any given day really shouldn’t affect the valuation of a company with 60-odd years’ worth of reserves. It is long-term oil prices and risk assessments for the global economy, Saudi reform efforts, climate change and strife in the Middle East that really move Aramco’s needle.

And yet optics have always been a central element of this IPO, part of a bigger sales pitch for the country as a whole. Getting to the $2 trillion valuation the prince boasted of almost four years ago, however, has clearly been an obstacle to getting it done and one reason why Aramco appears set for a domestic, rather than international, debut. Compiling another quarter’s numbers isn’t likely to change that. On the other hand, it provides a bit more time to perhaps persuade some more strategic or Saudi investors to pitch in at a level that is acceptable to the one shareholder that really counts.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.