Russian Miner’s IPO Could Fill In London’s Gold Hole

(Bloomberg Opinion) -- Over two decades, Africa-focused Randgold Resources Ltd. earned a reputation for running efficient operations in tough places, with lustrous shareholder returns and a premium valuation to match. Since Mark Bristow's outfit agreed to merge into Barrick Gold Corp. in late 2018 to create a bullion mining giant traded in North America, there's been a space open on the other side of the pond for a midsize swashbuckler.

Nord Gold, owned by the family of Russian oligarch Alexey Mordashov, wants to fill that gap.

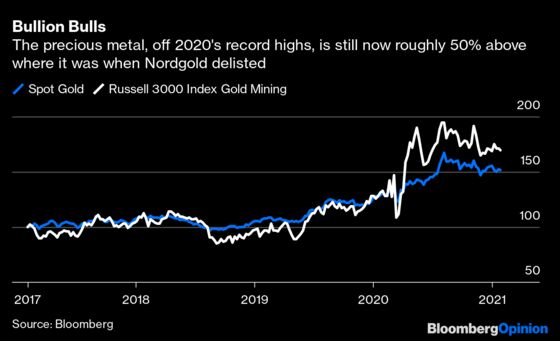

Set up in 2007 as a subsidiary of Mordashov’s steelmaker Severstal PJSC, Nordgold, as the company is known, has been in London before. A first effort to woo investors, then with global depositary receipts, was hampered by a lack of liquidity. It delisted in 2017 with an unimpressive $1.3 billion price tag. If Nordgold comes back, it will do so with annual production now at over 1 million ounces, a fifth more than in the last full year before the exit, and eyes on a premium London Stock Exchange listing with the healthy free float that requires. Meanwhile, gold prices are some 50% shinier. Add in Randgold’s departure — plus the promise of a sufficiently modest valuation — and 2021 looks brighter.

First, the good news.

Unusually for a Russian-owned miner, given most have tended to stick closer to home, U.K.-based Nordgold has followed a version of Randgold’s playbook from early on, eyeing Africa. Set up to dig for gold in Kazakhstan and Russia, the company went on to develop mines in Burkina Faso and Guinea, now accounting for almost half its total output. That’s added up to a reputation for building from scratch with competence, sticking to timetables and budgets in an industry that more often overshoots both. As important, it has been successful in acquiring smaller competitors and walked away last year from a frenzied bidding war for Cardinal Resources Ltd., discipline that was repaid with a profit.

Russia, meanwhile, remains one of the world’s most promising regions when it comes to gold, second in potential only to Australia. A decade ago, Randgold’s Bristow called it one of the last frontiers, under-explored as officials focused instead on oil and gas while entrepreneurs grappled with tough-to-process ore and tangled rules. Polyus PJSC’s development of Sukhoi Log, a giant deposit that alone accounts for more than a quarter of Russian gold reserves, should spark fresh interest.

If the offering does value the group at around $5 billion, the price mooted by the Wall Street Journal, it should appeal. Add in debt around the half-year levels to get to enterprise value, and that’s between five and six times a rough estimate of 2020’s earnings before interest, tax, depreciation and amortization, based on the full year’s production and a realized gold price of $1,779 per ounce. That would put the company shy of Russian heavyweight Polyus, at closer to eight times, but not far off the average of a wider group of peers. These include the likes of Canadian-listed Endeavour Mining Corp., also eyeing a London spot.

There is space and appetite for gold metal and miners, even if bullion is unlikely to continue testing the records it did in 2020 as the world shifts from pandemic panic to the prospect of a slow recovery. The question is whether Nordgold can convince investors that it’s the credible buccaneer to plug the Randgold hole. Others are vying for the crown, including Egyptian billionaire Naguib Sawiris’s Endeavour, with a more straightforward focus on Africa and a larger scale once it merges with Teranga Gold Corp. Nordgold boss Nikolai Zelenski and his team of advisers at Bacchus Capital will have to sell the merits of a diversified strategy, split between two main regions.

Randgold’s Bristow showed that even generalist investors, cautious after the disasters that followed the gold boom in 2011, can be won over with exploration success, a conservative approach and solid returns. Nordgold needs to beat off other pretenders to repeat the trick.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

©2021 Bloomberg L.P.