Rocket Internet's No-Brainer Is a Missed Opportunity

(Bloomberg Opinion) -- Investors in Softbank Group Corp. and Naspers Ltd. should see Rocket Internet SE as a cautionary tale.

Chief Executive Officer Oliver Samwer is evaluating a plan to take the Berlin-based startup incubator and venture capital firm private, according to a report in Germany’s Manager Magazin. For Samwer and his brothers, who are the biggest shareholders, the move is a no-brainer. For investors, it’s a missed opportunity.

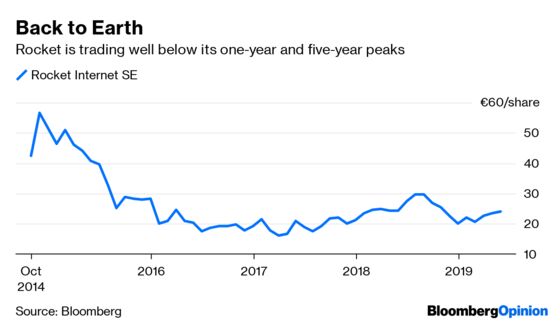

The Samwers own about 43% of Rocket, which had a market capitalization of 3.7 billion euros ($4.2 billion) before the Manager Magazin report. But combining the book value of the 200 or so startups in which it has invested, its three publicly traded investments and its net cash, gives it a valuation closer to 4.7 billion euros. On that basis, it’s trading at a 21% discount.

Rocket’s hefty pile of money would make a take private deal pretty straightforward: it was sitting on net cash of 3.1 billion euros in mid-May, according to a company presentation. Raising debt to fund a buyout should be straightforward.

The missed opportunity for investors lies in the deployment of that capital, or rather, the failure to do so. Rocket has sold down its stakes in Delivery Hero SE, Jumia Technologies AG and HelloFresh SE in the past year. That generated significant returns, but not much else. Some of those proceeds funded a buyback program, but far more is sitting unused on the balance sheet. Samwer told shareholders earlier this month that Rocket has “more capital than ideas,” and investors are the poorer for it.

If he’s right, then a management buyout makes some sense, since it would leave the private firm with a more manageable pile of cash to invest, and ease capital market scrutiny. But investors have every right to feel let down.

The question is what offer they should be willing to accept. Were the brothers to pony up 30 euros a share, as Berenberg Bank analyst Sarah Simon proposed last month, that would be pretty much in line with a 4.7 billion-euro book value, and also represent a 21% premium to the average share price of the past 200 days. Yet it would still leave Rocket with net cash of more than 500 million euros to invest in future prospects. Shareholders should be loath to agree to any lower bid.

If an offer materializes below that level, they should demand that the supervisory board return cash by other means. Normally they’d be clamoring for a new CEO, but the company’s ownership structure makes that difficult.

Rocket’s situation shows how hard it can be to demonstrate the underlying value of loss-making but fast-growing startups to public investors. Naspers and Softbank are both evolving into publicly traded venture capital firms, and all three trade at a discount to the book value of their investments. The model still needs to be proven.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.