Roche Has a $5 Billion Chance to Lead on Drug Prices

(Bloomberg Opinion) -- One of the world's biggest drugmakers is betting on some very expensive medicines.

On Monday, Roche Holding AG said it will buy Spark Therapeutics Inc., a Philadelphia-based biotech firm focused on potentially curative one-time treatments that modify human genes, for $4.8 billion. Spark's first medicine, Luxturna, can stave off blindness in people with a rare eye disease. Its late-stage hemophilia gene therapies could help people live without a lifetime of expensive infusions.

Roche agreed to pay a 122 percent premium to Spark's Friday share price. That's aggressive, but Roche can more than afford it. The Swiss drug giant generated $15.7 billion in free cash flow last year and has a pristine balance sheet. There's reportedly another bidder, which might explain the lofty valuation. On the face of it, though, the deal does make sense.

Acquiring Spark makes Roche a big player in gene therapy, while protecting its increasingly important hemophilia franchise and broadening its drug-development pipeline as sales of older cancer treatments erode. But there are unique pricing issues around these drugs that would pose a challenge for any buyer. Luxturna costs $425,000 per eye, and hemophilia therapies will likely make that price tag look cheap. It will require more than scientific success to make this deal work for Roche.

Gene therapies are pricey for a reason. For one, they're tough to make. But also, and perhaps more importantly, they may have a lifelong impact after as little as one dose, making them more valuable than even an effective medicine that must be taken for years.

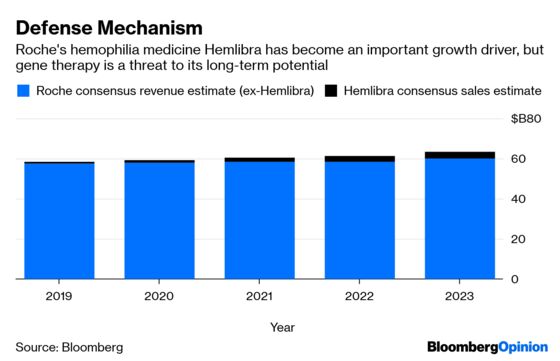

This is especially true in hemophilia. Roche's Hemlibra, which can treat particularly tricky patients and has become a major growth driver, costs more than $400,000 a year. One-and-done gene therapies could potentially erase that ongoing expense, saving the health-care system billions over time – and drugmakers want compensation for that value. The CEO of BioMarin Pharmaceuticals Inc. last week mentioned a potential price of $2 million to $3 million for its own hemophilia gene-therapy treatment. That would make it the most expensive drug ever.

Aggressive pricing is the wrong tactic, and not just because of the inevitable political backlash. The cost benefits of these medicines are still theoretical; there are concerns that their effects could wane. And with people changing jobs and insurers all the time, health plans may be reluctant to make the equivalent of a big investment that may benefit someone else in the crucial U.S. market. As crazy as it sounds, they may prefer massive annual bills.

Spark has tried to address these issues, offering discounts on Luxturna in some cases if patients don't hit vision targets. It's one of the more prominent examples of what’s known as value-based pricing. It's also working with the government to make installment payments possible.

That's a start, but Roche should take things further. That means bigger value-based discounts – 75 percent of $850,000 is too much to pay for a drug that doesn't work as expected – and fully embracing smaller payments over a longer period. This would go a long way toward salving insurer concerns.

Buying Spark signals that Roche is ready to make a significant commitment to gene therapy. The firm is rightfully concerned about Hemlibra being replaced, but almost $5 billion is a steep price for just an insurance policy and Luxturna's comparatively modest sales potential. Roche would benefit over time from creating a system where gene therapies are embraced for their value instead of hampered by their prices. The firm's robust pipeline and stable shareholder base will help it weather any near-term pain.

Roche has shown a willingness to sacrifice on price to reach more patients in the past. The Spark deal creates an opportunity for Roche to be an even bigger leader in pricing.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.