(Bloomberg Opinion) -- Given the recent spike in inflation rates, it may not seem as if $1 goes very far these days in the U.S., but it certainly does in the foreign-exchange market. And that brings up some unexpected issues for the Federal Reserve as central bank officials gather next week for their annual Jackson Hole symposium.

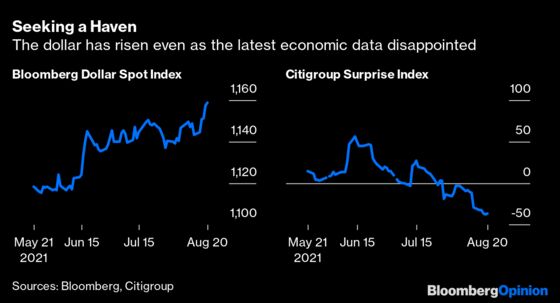

The greenback’s value during the past week rose to its strongest level of the year against its chief peers as measured by the Bloomberg Dollar Spot Index. It’s also now the best performer year-to-date based on the Bloomberg Correlation-Weighted Currency Indexes. Although the knee-jerk reaction might be to interpret the gains as a sign of confidence in the U.S. and its policies, the recent action seems to be anything but.

Putting aside the potential geopolitical harm to the Biden administration and its policies from the U.S.’s chaotic withdrawal from Afghanistan, it’s clear that the dollar’s strength is mostly about rising concern among investors about the durability of the recovery. Indeed, recent economic data has fallen short of estimates to a degree not seen since the early days of the pandemic in June 2020, and big Wall Street firms like Goldman Sachs Group Inc. are cutting their growth forecasts.

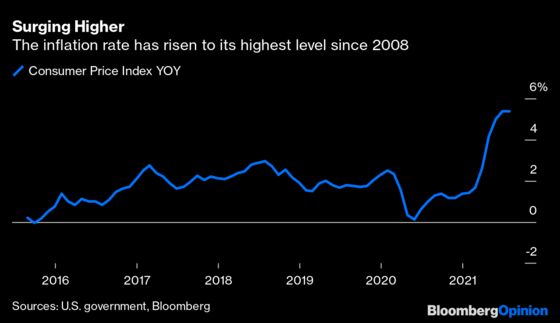

The problem for the Fed is that a stronger dollar tends to act as a drag on the economy by making exports less competitive while importing inflation. Those two effects increase the chances of a policy mistake. With inflation rates as measured by the consumer price index the highest since 2008, the central bank is under pressure to start pulling back on its unprecedented stimulus measures. Moving too soon could exacerbate a slowdown; moving too late could make it almost impossible to get inflation back under control.

Many economists and investors expect Fed Chair Jerome Powell to strongly signal at Jackson Hole — which he will attend virtually — that the central bank is ready to lay the groundwork for tapering its bond purchases. The thinking is that the Fed would then announce a formal plan at its next policy meeting, which starts Sept. 22, and then start tapering after the next meeting, which starts Nov. 3.

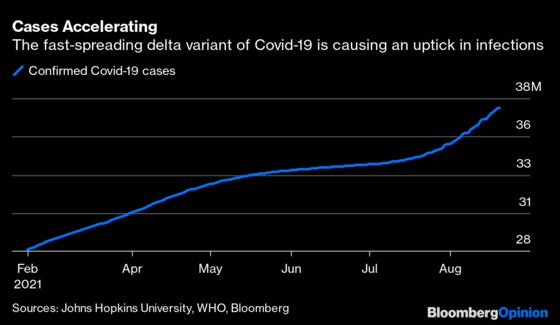

Powell, though, is worried about the more than 6 million Americans who are still out of the workforce because of the pandemic. He would probably rather wait until the September policy meeting to lay the groundwork for a tapering . By then, he would have seen the August jobs report, another CPI report, how the return to school is going and whether the highly transmissible Covid-19 delta variant had come under control. A rising dollar may give him cover to wait.

A stronger dollar is no friend to equity investors. S&P Global Ratings figures that 30% of the revenue among S&P 500 Index companies comes from outside the U.S. and that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. This wouldn’t be so concerning if the global outlook was improving, but it’s not. The World Trade Organization said this week that the global trade in goods is decelerating and may be at a plateau. Here’s what the Geneva-based group said about the situation:

“The outlook for world trade continues to be overshadowed by downside risks, including regional disparities, continued weakness in services trade, and lagging vaccination timetables, particularly in poor countries. Covid-19 continues to pose the greatest threat to the outlook for trade, as new waves of infection could easily undermine the recovery.”

There is no doubt, as former Treasury Secretary Robert Rubin declared in the mid-1990s, that a strong dollar is ultimately in the best interests of the U.S. That’s because it acts as a store of value, attracting the foreign capital that helps America service its budget deficit and keeps a lid on borrowing costs. Just this week, the Treasury Department said foreign holdings of U.S. Treasuries and related securities rose by $131.4 billion in the first half of 2021.

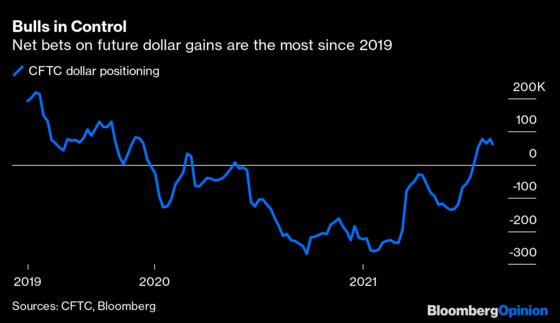

To be sure, the greenback’s 3.72% appreciation since mid-June as measured by the Bloomberg Dollar Spot Index pales in comparison to many of the big runs it has made throughout its history. Still, investors are betting the move higher may be just getting started. Positioning among hedge funds and other large speculators is the most bullish since the end of 2019, Commodity Futures Trading Commission data show.

The dollar has played a bit part in monetary policy in recent years, but if those hedge funds and other large speculators are right, that may be about to change.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.