Rishi Sunak Is Having the Wrong Conversation on Tax

(Bloomberg Opinion) -- Britain’s Chancellor of the Exchequer Rishi Sunak has enjoyed the kind of popularity usually reserved for rock stars and royalty. Urbane without being aloof and one of the government’s best communicators, he has put the full weight of the Treasury into cushioning the economic blow of the pandemic and preserving jobs.

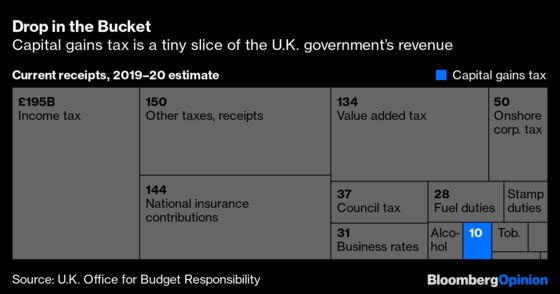

Now he has to figure out how to pay for it amidst the largest decline in annual GDP for 300 years. The announcement Tuesday night of a review into capital gains tax is the first sign the government is looking for ways to plug the gap. Only, it’s not a hugely encouraging one.

There is logic in rethinking the CGT, which is imposed on the gains from sales of second homes, stocks and works of art. Capital gains in the U.K. are taxed at 20% (or 28% from property sales) for higher-rate taxpayers and 10% for basic rate taxpayers, while top earners pay 45% income tax. That puts unearned income at a significant advantage to earned income.

The Resolution Foundation, a think tank that aims to improve standards for the least well off, published a report in May arguing that half of all taxable capital gains are now related to people’s jobs — think performance bonuses for investment fund managers in the form of “carried interest” or share options schemes — rather than arm’s length investments. Tax policy has fallen behind the way income is structured, the think tank argues, benefiting the wealthiest but short-changing the Treasury.

The main case for keeping a lower tax on capital gains has always been that it encourages risk-taking, which promotes the efficient allocation of capital, entrepreneurialism and economic growth. Lower capital gains taxes mitigate the problem of “lock in,” when investors hold onto assets to avoid paying taxes.

These days, though, there are grounds for asking which policies really encourage entrepreneurship and which merely amount to a tax shelter. A lenient CGT regime should not be a way to avoid income tax.

Britain needs to both encourage risk-taking and investment, but also find ways to finance a major public spending program that lies at the heart of the government’s rebalancing agenda. The CGT isn’t going to plug the hole, but the fact that it is under the microscope shows just how fraught the alternatives are.

The core problem for the Tories is political. This is a party for whom low taxation has been an article of faith since tax cuts in the 1980s under Margaret Thatcher freed the economy and fueled growth and investment. However, two factors have challenged that orthodoxy. The first was the Conservative election victory, delivered largely with the votes of poorer, former Labour Party supporters in the Midlands and north of the country; the second is the way the pandemic has radically changed priorities and created an enormous hole in public finances.

Those former “red wall” voters were on Boris Johnson’s side of the Brexit debate, convinced by the promise that the U.K. would “take back control.” But they were also won over by Johnson’s pledge to rebalance the British economy, leveling up, as he repeatedly put it, by spending heavily on infrastructure, healthcare, policing and other public services. If exceptionally well managed, such investment could make Britain a fairer, more prosperous place.

At the same time, Johnson promised the Tories’ traditional base of middle class homeowners that he would be faithful to at least the low-tax tenet of Conservative doctrine. The biggest pledge in the Tory manifesto was a “triple tax lock” — that is, no increases in income tax, National Insurance or value added tax. The promise was a salve to fiscal hawks, but it also perpetuated a false narrative that a massive increase in public-service spending would not require additional revenue raising. This conceit can’t last.

The Chancellor could try to increase headline taxes through a back door by applying them to a wider range of income or expenditure. But the scope here is limited. More likely, he’ll have to find other revenue sources.

Some kind of wealth tax — though called something far friendlier — seems inevitable. The question is what this government will consider wealthy. An American taxpayer must earn over $518,000 to pay the top tax rate of 37%, while in Britain the 40% income band kicks in at over 50,000 pounds ($63,000) of income.

There are worries that Sunak will decide to eliminate the capital gains tax exemption on main homes, ending a bonanza for many homeowners as years of low interest rates drove up purchases and property values. That would be brave, but hugely unpopular. It would also penalize many (Conservative-voting) older people, whose home is their pension.

A better approach might be to change Britain’s outdated and regressive current system of property taxes, which are levied according to a number of bands by local councils but based absurdly on 1991 property values.

Another target is corporate taxation — or rather, corporate tax avoidance. In the election manifesto, Johnson scrapped a planned reduction in corporate tax to 17% from 19%, which would have cost the Treasury 6 billion pounds. The problem is that many companies find ways to avoid tax altogether. The solution isn’t to milk corporate “fat cats,” a favorite trope of the left in Britain, but to create a fairer tax system in which companies cannot use numerous loopholes to avoid taxes.

In its fiscal sustainability report this week, the Office for Budget Responsibility concluded that, given the fiscal damage caused by the pandemic, “it seems likely that there will be a need to raise tax revenues and/or reduce spending” to return public finances to health.

Not all of the new spending has to be paid for now. One-off measures such as the generous furlough scheme, which is being tapered, can be covered over time through low-cost borrowing. But if the post-Brexit, pandemic-era U.K. economy is going to be smaller, then the resulting structural deficit presents a more immediate problem.

Ultimately, a review is just that, and Sunak may decide not to change CGT much. Nor is the Autumn budget inevitably the moment of truth: If Britain’s economy continues its current trajectory and the pandemic is not under control, he may postpone the tough decisions. That will at least keep him popular a little longer. But a reckoning is coming that will require the Conservative Party to make choices it has so far avoided.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Therese Raphael is a columnist for Bloomberg Opinion. She was editorial page editor of the Wall Street Journal Europe.

©2020 Bloomberg L.P.