WFH Divides Real Estate Into the Good, Bad and Ugly

(Bloomberg Opinion) -- “Work from home” and lockdowns have carved up the real-estate sector into a handful of winners and many more losers. The resulting split into the good, the bad and the ugly presents a challenge for investors who expect diverging valuations to revert to historic averages in 2021.

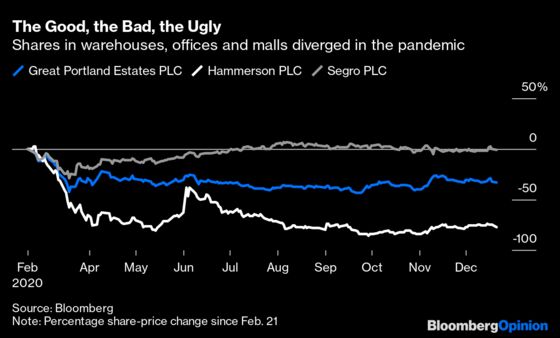

As the pandemic took hold, investors hoovered up shares in warehouses and logistics centers that facilitate the socially distanced economy. Mall owners were abandoned. Between the two extremes, offices suffered, but not as much as feared.

Many workers in finance, law and professional services adapted to remote working. Their firms’ revenues proved surprisingly resilient. That’s meant haggling over the rent hasn’t been a top priority.

Still, the Sunday atmosphere that persists in financial centers during the working week makes it hard to be overly optimistic for offices just yet. Real-estate stocks focused on London offices have fallen by about a third, and they trade close to a 25% discount to their most recent reported net asset value. A discount below 20% would be more usual, so the valuations anticipate office values will fall further, but not collapse.

The new strain of Covid identified in the U.K. has reinstated tougher lockdowns and closed restaurants and non-essential stores again. That makes it harder for mall operators to vacate the ugly spot on the podium. The curbs will immediately turn off tenants’ income and hit rent collections.

Even with the U.K. and Europe embarking on Covid-19 vaccine campaigns, mall owners such as Unibail-Rodamco-Westfield — owner of the popular Westfield sites — and Hammerson Plc trade at discounts of about 50%-80% of NAV. That too anticipates further asset writedowns — savage ones.

How might these valuations revert back to real estates’ historic low double-digit (or smaller) discounts to NAV? Either share prices must adjust, or underlying values must move — or a mixture of both. It’s hard to assess what might happen because there are two big unknowns.

One is whether people will simply head back to the office when the pandemic is under control. The longer governments have pushed a WFH-where-possible policy, the more expectations have risen that flexible arrangements will stick. Some corporate tenants are already seeking less space, to turn homeworking into a cost cut. Still, the savings aren’t huge as a percentage of total staff expenses, and some employers will probably see a drop in the person-per-square-foot ratio as good for morale. Frustratingly for investors, long leases mean the picture will remain fuzzy for a while.

The other uncertainty is the sustainable level of rents in retail and leisure. The pandemic forced shoppers online, diners to takeaways and fitness fanatics to home gyms. Existing trends rapidly accelerated. The resumption of office working would support city centers, but malls have a harder job preventing the online journey becoming one way. Their owners face the cost of making locations more attractive while servicing high debts. But if vaccines truly bring back some semblance of normal life, an indication of where consumer habits are settling could emerge in 2021.

It’s easier to see rents and values of offices and retail premises getting worse before they get better. But expectations for these sectors are low already. Indeed, “safe haven” logistics properties could lose some appeal if investors buy back into malls and offices, Bloomberg Intelligence analyst Susan Munden points out. Such a rotation could gain pace if investment strategists are right in predicting investors will shy from from chasing pricey growth stocks next year and buy equities that look cheap and are exposed to a recovery.

The gap between share prices and actual property values will narrow eventually. But with the virus becoming more menacing, and vaccine distribution slow, equity investors’ pessimism is going to be hard to turn.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2020 Bloomberg L.P.