Reckitt Can Still Make it to the Glaxo-Pfizer Party

(Bloomberg Opinion) -- There's a party in the pain relief aisle and Reckitt Benckiser Group Plc hasn't been invited.

GlaxoSmithKline Plc and Pfizer Inc. said Wednesday they would combine their consumer healthcare businesses into a new joint venture.

Both Reckitt and Glaxo had looked at Pfizer's consumer health unit, which makes Advil, earlier this year. Both walked away.

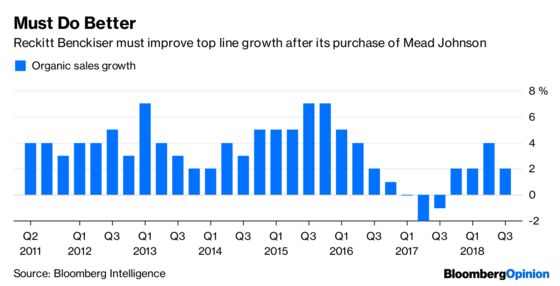

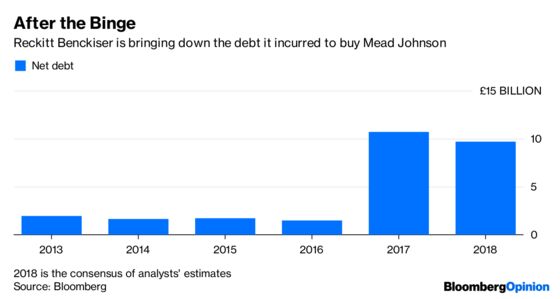

Reckitt had good reason to turn it down. The company still had to fully digest its 2017 acquisition of baby products maker Mead Johnson, and really needed to bring down debt. Still, the ideal scenario was that Chief Executive Officer Rakesh Kapoor would return for the Pfizer business – or at least part of it – once these tasks were complete.

That dream now looks dead, as Glaxo has outmaneuvered its rival. It will have 68 percent of the combined business, and Pfizer will have 32 percent.

To make matters worse, Reckitt now faces a more muscular competitor. The combined group will have annual sales of about 10 billion pounds ($12.7 billion) and be the leader in categories including pain relief, respiratory treatments, vitamins and minerals as well as digestive, skin and oral health.

The company’s shares initially fluctuated on Wednesday, but were up 0.3 percent midmorning. That's partly because not all investors were so keen on Reckitt adding Advil, which would have increased its exposure to cheaper competitors and required it to take on even more debt.

But this may also reflect the fact that all is not lost. Glaxo said it plans to list the new business on the stock market within three years. That paves the way, further down the line, for some kind of combination with Reckitt's own health business, which includes Nurofen and Strepsils, and has annual turnover of about 8 billion pounds including infant nutrition. There’s scope for a sort of pill-packet roll-up, if you like.

That timing could work just as well for Kapoor. Reckitt has made a good start – net debt is forecast to be 2.7 times earnings before interest, tax, depreciation and amortization, according the consensus of Bloomberg estimates. That's below the 3 times at which investors generally start to get nervous. But Mead Johnson’s operations are proving troublesome. In the third quarter, disruption at a plant in the Netherlands that makes baby formula shaved 70 million pounds off of its revenue.

At least now the parent has more time to fix this. And in the meantime, Reckitt could engage in some corporate restructuring of its own. Its hygiene and home business could be worth about 20 billion pounds, assuming a 25 percent takeover premium, according to Martin Deboo, an analyst at Jefferies. With Alan Jope set to succeed Paul Polman as CEO of Unilever in January, the Anglo Dutch consumer good group could be a potential acquirer.

So the party might not quite be over for Kapoor.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2018 Bloomberg L.P.