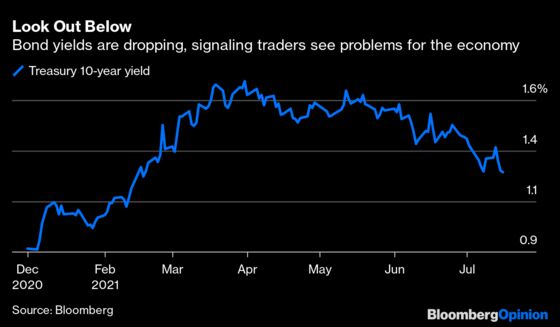

(Bloomberg Opinion) -- Mystery solved? There’s no bigger question in financial markets than why U.S. government bonds — the benchmark for all markets worldwide and the ultimate “risk free” asset — have managed to rally in the face of faster inflation and a booming economy.

At 1.30%, the yield on the 10-year Treasury note is down from the high this year of 1.77% at the end of March and about half a percent less than where economists surveyed by Bloomberg last month expected it to be this quarter. For those keeping score, yields have now dropped three consecutive weeks and eight out of the past nine.

This week we moved closer to the answer, which increasingly seems to be that looks can be deceiving.

Let’s start with the monthly consumer price index report put out by the Labor Department on Tuesday. Core CPI, which strips out volatile food and energy prices, rose 4.5% in June from a year earlier. The increase was biggest since the early 1990s and exceeded the estimates of all 46 economists surveyed Bloomberg News.

Rising inflation rates are like kryptonite for the bond market because they erode the value of fixed-interest payments over time, making the securities worth less. (At negative 3.20%, so-called real yields haven’t been this low since 1980. But we all know what happened next, which is that inflation decelerated, sparking a bull market in bonds that is arguably still going on today.)

The gains in the inflation numbers are less menacing when you take a closer look and find that, according to the economists at BNY Mellon, more than half the increase came in just seven categories: new autos; used autos; vehicle rentals; admissions to events; food away from home; airfare; and lodging. As the economists pointed out in a note to clients, the first three items are specific to the semiconductor shortage that is hurting the auto industry, and the rest are clearly associated with the economy’s reopening.

In that sense, bond traders appear to be in the camp of those who think the current high rates of inflation are transitory and will reverse soon.

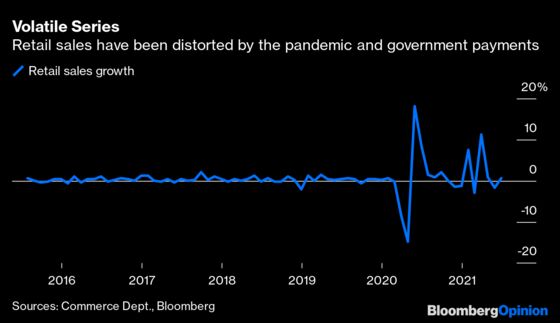

It’s a similar story with retail sales, which the Commerce Department said Friday rose 0.6% in June. The median estimate of economists surveyed by Bloomberg was for an increase of 0.3%. The gain looks less impressive when you consider that the drop in sales for May, originally reported as a decline of 1.3%, was revised lower to a decrease of 1.7%. In other words, June’s beat was attributed entirely to May’s revision.

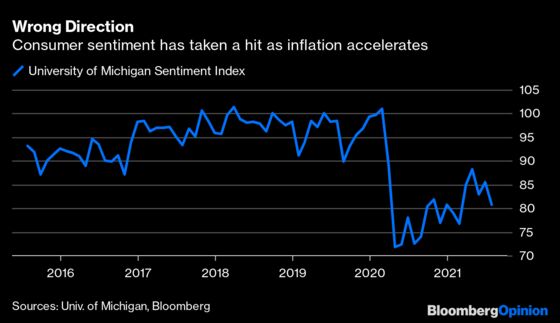

An even more troubling report came soon after the retail sales data, when the University of Michigan’s preliminary consumer sentiment index for July fell short of estimates by a wide margin. At 80.8, the index fell below the median estimate of 86.5, resulting in the biggest disappointment in at least a decade.

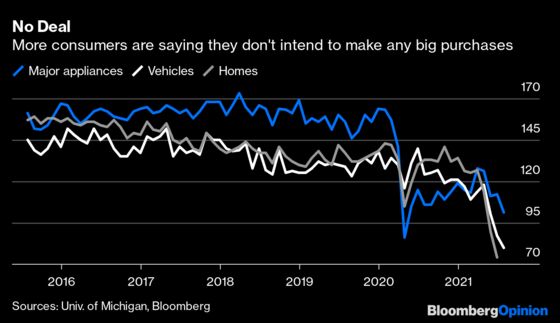

The takeaway is that inflation is generating a bit of sticker shock, foreshadowing a slowdown in consumer spending, which accounts for about two-thirds of gross domestic product. The percentage of consumers who think it’s a good time to buy a household item fell to the lowest since the early days of the pandemic in April 2020, while the percentages of those who think it’s a good time to buy a vehicle or a house plunged to the lowest since the early 1980s.

Here’s how Rubeela Farooqi, the chief U.S. economist at High Frequency Economics, put it in a research note to clients:

Momentum in household spending, which has been driving growth will likely decelerate in the third quarter, even as job growth restores incomes, but savings diminish and fiscal support expires.

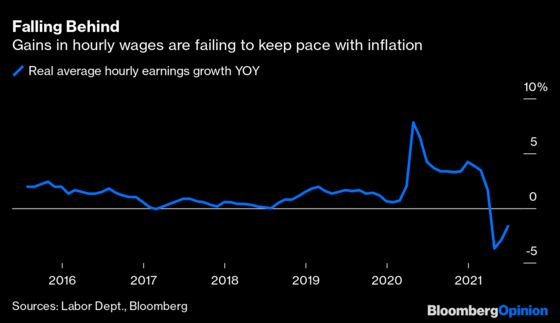

Not only that, it’s hard for consumers to get excited about spending when wages aren’t keeping up with inflation. The CPI report showed that real average hourly and weekly earnings fell in each of the past three months.

To be clear, at any one time many factors are influencing bond yields. My Bloomberg Opinion colleague John Authers in a column this week included a list of five very good reasons yields are falling, the majority of which have nothing to do with current or expected future economic conditions. (My personal favorite is that Treasuries are very attractive to investors in other developed markets where yields are still largely negative. The dollar’s strength this year seems to support that idea.)

No one is saying that the economy is about to roll over. But evidence is mounting that consumers are experiencing some sticker shock because of faster inflation and are pulling back. A slowdown in spending in coming months will make current forecasts by economists for continued strength in the second half of 2021 look a little too generous. Don’t forget that there are some 6.76 million fewer workers on payrolls compared with those just before the start of the pandemic.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.