Raising Taxes Is No Way to Fund an Infrastructure Bill

(Bloomberg Opinion) -- With the Covid-19 relief bill behind us, attention is turning to infrastructure — a longstanding priority for President Joe Biden’s economic recovery program. A big infrastructure bill would achieve multiple goals at the same time: putting Americans to work, raising wages, strengthening the economy, improving industrial competitiveness and speeding the transition to green energy. Given the confluence of all of these urgent goals, Congress should not balk at the borrowing needed to pay for the bill.

Traditionally, American infrastructure bills have been a grim necessity that maintain the existing economy without really improving it. Civil engineers will warn that our roads and bridges are decaying, and after years of that the federal government will lob a pot of money at the problem, along with a smattering of new construction projects. The roads and bridges get patched into passable condition, some construction workers get jobs, and the system creaks along for another few years.

Biden’s bill will almost certainly be different. The ambitious plans laid out by his campaign amount to nothing less than a transformation of the U.S. economy. Biden’s biggest goals include a massive shift toward green energy, promotion of domestic manufacturing and an emphasis on caregiving jobs that are expected to provide mass middle-class employment in the coming decades.

It’s not yet clear how much of this will actually make it into an infrastructure bill. The first big question is whether Biden will use the reconciliation process in the next fiscal year, which begins Oct. 1. That would allow infrastructure to get around the filibuster, eliminating the need to find 10 Republican senators who support it. Given that not even one Republican senator voted in favor of Biden’s Covid relief bill, despite the fact that it was popular with Republican voters, suggests that reconciliation is probably the way to go (unless the Democrats can convince their party's centrists to pass filibuster reform).

Using reconciliation will limit the bill to fiscal measures, meaning that a lot of the regulatory efforts Biden wants — for example, mandating higher fuel-economy standards — might have to be stripped out and addressed in separate legislation.

But the spending items will be the really crucial part. Speeding the transition to green energy is the country's most important economic task because it combines the existential imperative of fighting climate change with the economic promise of cheaper energy. The amazing decline in the cost of solar and batteries promises to spark a productivity revolution in many other sectors of the economy — including manufacturing — but it will require big investments in order to realize that potential.

For example, a modernized electrical grid will help transport energy from place to place, reducing intermittency and creating robustness against disasters like the recent winter storm outages in Texas while making electricity cheaper in general. A network of charging stations for electric vehicles will speed the replacement of internal combustion cars (another Biden goal). These networks are so big, and used by so many different players in the market, that it’s difficult for a single private company to make the necessary investments; hence, government has a big role to play. In addition, government can boost the transition of U.S. electric power to solar and wind by providing matching funds for private investments in these technologies; doing so accelerates the learning curve that reduces renewable costs even further and allows the Biden administration to put its thumb on the scale for energy sources that don’t exacerbate climate change.

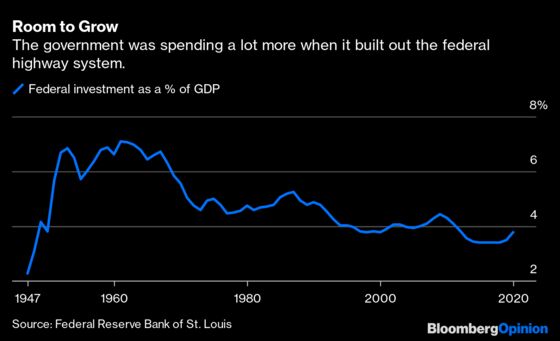

So it’s time to go big in terms of government investment. Biden’s plan would be the modern equivalent of the interstate highway system, which built denser economic connections between America’s far-flung regions, ultimately giving the economy a significant boost. That didn’t come cheap, though; interstate construction helped push government investment to 7% of GDP, compared to less than 4% today:

That will require a lot of government borrowing. Unfortunately, Senator Joe Manchin of West Virginia, a powerful centrist whom many regard as casting the decisive vote, has declared that any infrastructure bill should be financed by tax increases rather than by further deficits.

That's exactly the wrong approach. As I explained in a previous column, a transformational green infrastructure push is just the kind of thing we should be borrowing to fund. Not only is it a one-time expense, but it will yield an economic return in terms of cheaper energy that boosts the private sector for many decades to come.

Private companies borrow to fund big investments all the time; to demand that the government pay for the transition to green energy entirely out of tax revenues would be like insisting that companies pay for major capital projects out of current revenues. In other words, it makes no sense. Taxes are necessary for funding ongoing social expenditures, like Biden’s child allowance; they’re not the way to pay for big one-time investments.

In that sense, it’s fine to raise taxes to pay for road repairs; that’s an ongoing expense rather than a one-time outlay. This could come in the form of a gasoline tax hike, a vehicle-miles-traveled tax, or a carbon tax, all of which are now being proposed.

But Manchin should drop his insistence on full tax funding for the infrastructure bill. And Democrats should insist on going big. If they can find 10 Republican senators to go along with an ambitious green investment program, that’s great, but in the likelier event that's not possible they should just use reconciliation. The transition to renewable energy is too important to sacrifice on the altar of either austerity or bipartisanship.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2021 Bloomberg L.P.