(Bloomberg Opinion) -- Few outside of Iran will weep at the violent demise of Qassem Soleimani. The oil market, never sentimental, joined those cheering the sudden end of the leader of the Quds Force of the Islamic Revolutionary Guard Corps, albeit for different reasons. Will its peculiar brand of excitement last?

One possible clue is the market’s reaction to another major escalation: September’s attack on Saudi Arabia’s Abqaiq oil-processing facility. Brent spiked 15% the next trading day, only to fall below its pre-attack level within about two weeks. Friday’s reaction to Soleimani’s assassination was more muted, and Brent is now below where it closed last week. Having absorbed one game-changing attack that didn’t change the game a few months ago, the oil market appears to think this latest one fits that mold, too.

It makes more sense to view them on a continuum rather than as discrete events, though. Like the attack on Abqaiq, Soleimani’s death represents a major escalation in a pattern of them. Geopolitical risk is building by accretion, and at a pace that would have sent oil prices into triple digits not so long ago.

That it isn’t now relates largely to the impact of U.S. tight-oil production on inventories and, more importantly, expectations. Supply is seen as abundant enough to absorb whatever comes its way. Shale is just one fundamental change to have ripped through global energy in the past decade. Another is the changing U.S. role in the Middle East as it steps back from supporting the global trade and security order in general (in part because of shale-inspired dreams of “energy dominance”; everything’s connected).

This upending of preconceptions about energy and geopolitics is a risk factor in itself.

Start with Washington. There is enormous dissonance between President Donald Trump’s long-held position of avoiding more wars and suddenly taking out a figure of Soleimani’s importance. While the attack on Abqaiq amounted to a declaration of war, its effects were largely confined to how quickly a piece of infrastructure could be repaired. The implications of Thursday’s strike are far more open-ended.

Some within the U.S. administration may see this as a way to shock Iran into backing off; others might wish to goad Tehran into all-out war to settle scores stretching back through the Iraq War all the way to the hostage crisis. Indeed, the recent attack on the U.S. embassy in Baghdad seems the real trigger for retaliation.

Iran’s leadership may also have 1979 in mind. Having just brutally squashed protests at home, Supreme Leader Ali Khamenei will not want to appear weak and risk encouraging the sort of dissent that felled the Shah. With the economy reeling from sanctions — it shrank by more than 9% last year — “the Iranians have almost nothing to lose at this point,” says Helima Croft, head of global commodity strategy and research for the region at RBC Capital Markets. Retaliation, even if it invites further retribution, seems inevitable.

What form that takes is also unclear and likely multi-pronged. One battlefield will be the country where Soleimani was killed: Iraq. Any disruption to oil operations there should register immediately with the market. Iraq was by far the least compliant of any OPEC member in terms of supply cuts last year. If it were to tip into OPEC’s select club of involuntary cutters alongside Venezuela and Libya, then it would boost the group’s effort to support prices. Besides the potential for violence, an Iraqi government caught between Washington, Tehran and its own domestic unrest may push to remove the last of the U.S. military presence from the country. It’s far from clear Washington would resist much, given Trump’s broader desire to disengage.

We also shouldn’t forget the rest of the neighborhood. Saudi Arabia and the Gulf states all host U.S. troops Iran might target (along with shipping in the Strait of Hormuz). Any such action would likely spark retaliation in kind. Saudi Arabia, in particular, has the Abqaiq attack fresh in its memory, and the U.S. decision to kill a seemingly untouchable Iranian military leader might embolden Iran’s regional rival to step up its own response.

The final piece of the puzzle is thousands of miles from Baghdad. Geopolitical premiums in oil are essentially free money for U.S. exploration and production companies. The sector has been crushed by the late realization that the past decade’s stupendous gains in production came at the expense of investors (see this).

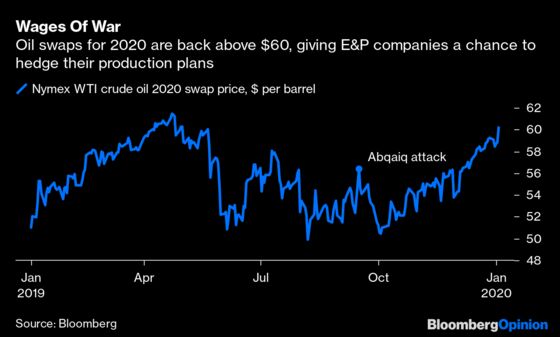

A big question arising from the latest trouble in the Middle East is whether higher oil prices blunt the impulse to be more disciplined on drilling. Nymex crude oil swaps for 2020 have leapt back above $60 a barrel, higher than they got in the wake of the Abqaiq attack and back to levels seen in May, before the big summer sell-off. The potential for hedging, along with the fact that the most leveraged E&P stocks topped the sector leaderboard on Friday morning, suggests the temptation to backslide is there, at least.

Since the Abqaiq attack, sentiment in oil markets has been bolstered by the OPEC+ meeting and signs of a thaw in the U.S. trade war with China. The latter is especially important, as it would underpin demand; whereas controlled cuts from OPEC+, while cosmetically appealing, are also manifestations of a fundamentally loose market. Uncontrolled cuts, taking oil supply off the market altogether, are a different matter. Continued escalation in the Middle East could push oil out of its prevailing range toward $80. Much depends on the newfound discipline of U.S. producers.

Beyond this, consider the bigger picture. Having shrugged off numerous provocations, including Abqaiq, Washington decided to retaliate now and with unexpected ferocity. A broad policy of stepping back, pre-dating Trump, invited Iranian adventurism; and yet the U.S. has demonstrated that, even with a much-reduced presence, it can deploy enough force to upend things if it chooses. Besides climate change, the single biggest risk to the oil market is its reliance on a fractious region where U.S. security relationships were one of the relative constants. Now, Washington is more of a spoiler, and a capable one at that. Soleimani’s explosive end is the opposite of business as usual.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.