(Bloomberg Opinion) -- The seemingly never-ending saga of Puerto Rico’s unprecedented bankruptcy took another turn during the weekend. In what’s being hailed as a big step forward for the commonwealth, it reached a tentative agreement with Aurelius Capital Management, Autonomy Capital and other investors who own $8 billion of the island’s bonds.

The move is certainly significant. For one, it appears to end the push to invalidate entirely some of the island’s general-obligation bonds. Also, Aurelius is infamous on Wall Street for spending more than a decade in court fighting Argentina for repayment on its bonds, so the fact that it seems to see the limits of a hardball strategy is reason to believe the finish line could be in sight for Puerto Rico. Bloomberg News’s Michelle Kaske reported the details:

The potential deal with the commonwealth’s financial oversight board brings together rival bondholder groups that had been divided in the past year over whether debt Puerto Rico sold in 2012 and 2014 is invalid. Aurelius and Autonomy, which hold securities sold in those years, joined the tentative agreement, which other bondholders signed in June, according to a securities filing.

...

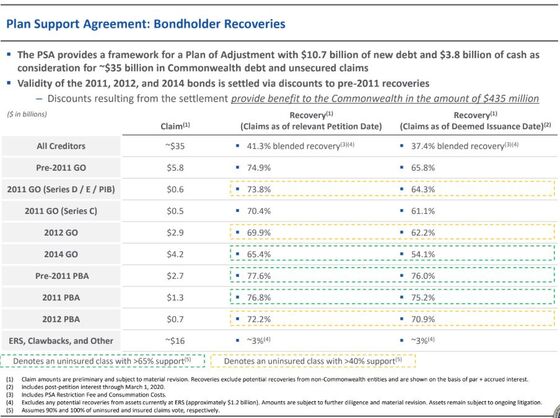

The potential deal would cut Puerto Rico general obligations and debt guaranteed by the commonwealth to $10.7 billion from $17.8 billion, about a 40% reduction. The overall plan slashes debt and non-bond claims to $11 billion from $35 billion, a $24 billion reduction.

For the casual observer, it’s easy to get bogged down by the numbers. A year ago, Puerto Rico managed to reduce $17.6 billion of sales-tax bonds to $12 billion through a debt exchange. Is that a good or bad deal? It depends who you ask. The one thing just about everyone can agree on is that the island had way too much debt in the first place. It’s unclear whether the cuts negotiated by Puerto Rico’s financial oversight board will be deep enough in the long run for an economy that’s still trying to bounce back from Hurricane Maria in 2017.

Yet for all the back-and-forth, one large part of Puerto Rico’s debt stack isn’t getting much attention, even though it’s facing the steepest losses and is a crucial component for making the entire restructuring plan work.

The oversight board’s revised agreement shows $16 billion of debt marked as “ERS, Clawbacks, and Other” that would receive a recovery rate of just 3%. The category includes bonds issued by the Puerto Rico Convention Center District Authority, the Infrastructure Financing Authority and the Highways and Transportation Authority, among others. Although these securities were always known to be junior to the commonwealth’s general obligations, I doubt investors expected they would be effectively wiped out.

The way the new proposal is structured, a huge chunk of debt reduction is coming at the expense of these junior creditors, who notably haven’t agreed to the terms, said Brad Setser, a former U.S. Treasury economist and now a senior fellow at the Council on Foreign Relations. To him, the current iteration of the restructuring hinges on the idea that the court, in a proceeding known as Title III, will use the deal with general-obligation investors to “cram down” the rest of the debt that isn’t part of a consensual agreement.

“The striking thing was the result of the mediation was basically a sweeter deal for the G.O.-PBA group, at the expense primarily of the junior bonds,” Setser said in a phone interview. “This is much more aggressive than the Detroit settlement. This really does make full use of Title III and the cram-down provisions, with the board more or less using the G.O.s as their confirming class.”

In Detroit’s bankruptcy, certificates of participation recovered about 14% of what they were owed, compared with 74% for unlimited-tax general obligations. Interestingly, Aurelius was among the holders of the subordinated debt in that case.

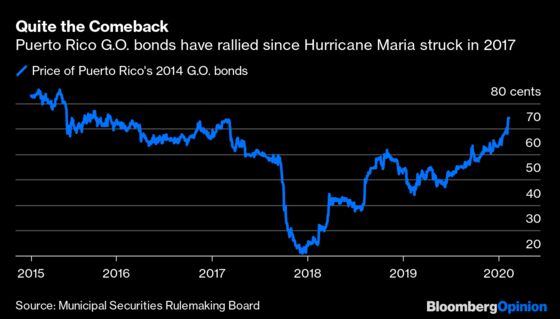

Now, Puerto Rico G.O. investors are on the verge of receiving a similar payout to those in Detroit, thanks to the tight squeeze on junior debt. Through new bonds and a cash payment, those holding 2014 G.O. debt will recoup 65.4 cents, up from 35 cents; 2012 G.O. bonds will get 69.9 cents, up from 45 cents; and earlier dated G.O.s will get somewhere between 70.4 cents and 74.9 cents. The bonds have climbed steadily higher in secondary-market trading.

Unfortunately, Puerto Rico doesn’t have a way out except for collective pain. Without question, the Wall Street machine played a crucial role in saddling the commonwealth with much more debt than it could ever hope to repay. Mutual-fund managers loved the high yields and triple tax-exempt interest, while bankers and law firms were happy to rake in fees and invent new ways to borrow. But elected officials aren’t blameless either. They promised too much and pushed off tough choices until it was too late. That brings us to the tragic current situation.

With where things stand on the island, it’s hard to see how junior bondholders could make a case for a better recovery. The plan has some caveats around that 3% rate, noting that it “excludes any potential recoveries from assets currently at ERS (approximately $1.2 billion). Amounts are subject to further diligence and material revision. Assets remain subject to ongoing litigation.”

That doesn’t mean they will give up trying, though. “The Oversight Board’s brazen disregard for bondholders’ lawful priorities and liens imperils investor confidence in Puerto Rico’s credit profile and sets precedents that threaten the broader municipal finance market,” a group of bond insurers said in a statement. It “risks embroiling Puerto Rico in many more years of protracted litigation.”

Still, going any higher would just saddle Puerto Rico with more debt. That’s likely a nonstarter when economists are openly pondering the risk of a second bankruptcy. Paying a few pennies on the dollar might come off as a shockingly low figure, but at this point, investors shouldn’t expect anything else from Puerto Rico.

PBA refers to the Puerto Rico Public Buildings Authority. The debt it issued is commonwealth-guaranteed, so it's grouped in with general obligations.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.