Public Pensions Throw Their Weight Around in Private Debt

(Bloomberg Opinion) -- Pension funds are the ocean liners of global markets. In the U.S. alone, state and local retirement funds have $4.57 trillion in assets. Across the developed world, the pool of money is close to $30 trillion. That means any change in their investment allocation, no matter how incremental, can create a seismic shift in certain corners of finance.

The hedge-fund industry, for example, swelled over the past two decades in no small part because of eager pension managers. Local officials banked on star investors delivering outsized gains to help the retirement funds meet their lofty annual return benchmarks, which in some cases exceeded 7%. According to data from Pew Charitable Trusts, U.S. state pension funds had a 26% allocation to alternative investments in 2016, up from just 11% in 2006.

Of course, with more hedge funds came fewer ways for them to profit — and pensions took notice. In September 2014, the California Public Employees’ Retirement System rocked Wall Street by announcing that it would divest the entire $4 billion it had across 24 hedge funds and six hedge funds of funds. In 2016, New Jersey’s pension fund cut its $9 billion hedge-fund allocation in half and New York City’s retirement fund for civil employees exited its $1.5 billion portfolio. More than 4,000 hedge funds have been liquidated in the past five years. With even some of the most well-known managers calling it quits, hedge funds are clearly in retreat.

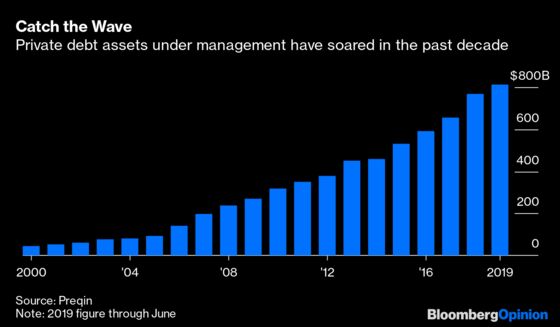

The market for private debt and direct lending is trending in precisely the opposite direction. Managers are raising money hand over fist, as they have in each of the past few years. Assets in private-credit strategies now total more than $800 billion — doubling from 2012 and up from less than $100 billion in 2005. By and large, it’s been simply too hard to pass up yields that sometimes crack double digits when typical junk bonds offer just 5%.

Not surprisingly, public pension funds want in on the action. An overwhelming majority of private-credit investors expect them to pour money into the asset class in the next three years. While that may sound like good news for the industry in the short-term, it could be an early indication that it’s game over for the booming market as we know it.

Bloomberg News’s Fola Akinnibi and Kelsey Butler talked to Al Alaimo, who oversees credit investments for Arizona’s $41 billion State Retirement System. He’s aiming to boost direct lending to 17% of the portfolio from about 13.6%. They also noted that the Ohio Police & Fire Pension Fund and the Teachers’ Retirement System of the State of Illinois are increasing their private-debt exposure. More broadly, 281 U.S. public pensions were involved with private credit in 2019, up from 186 in 2015, according to Preqin data. And they’ve increased their median allocation to 2.9% from 2.1%.

Now, that’s far from a huge stake. And pensions are something of an ideal candidate to invest in illiquid private debt, given that they have long time horizons and aren’t vulnerable to investor withdrawals, in contrast to Neil Woodford’s flagship fund and Natixis SA’s H2O Asset Management.

That doesn’t mean that they can’t get into trouble, though. As I wrote in August, Alabama’s pension funds got caught up in the bankruptcy of luxury movie and dining chain iPic Entertainment Inc. The state’s pensioners now own and operate the theaters, for better or worse. Marc Green, the pension’s chief investment officer, recently told The Wall Street Journal that working through distressed investments has paid off before and iPic may yet be a winner for the Retirement Systems of Alabama.

It’s worth heeding the lesson from the struggles of hedge funds: What worked before might not continue to work in the future, especially if more money is chasing the same strategy. “We wish there were fewer people in the marketplace,” Alaimo said about private debt.

Of course, that’s true for any market. But it’s especially risky for private credit and direct lending because handing all the power to borrowers gives them an opening to lower yields and weaken creditor protections. If that sounds familiar, it’s because that’s also what happened in the leveraged-loan market as investors flocked to the floating-rate securities during the Federal Reserve’s tightening cycle. For now, looser covenants aren’t necessarily deal-breakers, but without some balance, they could lead to steeper losses in an economic slowdown.

A survey of more than 60 private-credit managers by the industry trade group Alternative Credit Council revealed expectations for the market to further expand and deliver strong returns. Curiously, just 23% said they expected recovery rates to be lower than historical averages over the next three years, while 42% predict they’ll be higher. That might be the case if the economy ramps back up, or slows down but avoids an actual recession. But it seems naive to think private debt will fare better than before when managers are fighting one another for deals and sitting on hundreds of billions of dollars, just waiting for a chance to invest.

That dynamic isn’t likely to change soon, especially now that pension-fund behemoths are setting their sights squarely on private debt. For those that have been in the market for years, like the Arizona retirement system, it just means keeping tabs on existing managers to make sure they don’t veer into weaker deals.

For those trying to catch what might be the back end of the wave, it’s not so simple. Without proper caution and foresight, they might find themselves quickly navigating troubled waters.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.