(Bloomberg Opinion) -- Private equity firms, sitting on a record $388 billion of dry powder in Asia, may be about to get their reward for patience. Cash is king as corporate finances are stretched by the coronavirus outbreak. Having sat on their hands for much of the past year in protest at unappealing valuations, the virus-induced stock market meltdown is creating a potential parade of bargains. Blackstone Group Inc.’s reported plans to acquire Hong Kong-listed property company Soho China Ltd. may be just the start.

High valuations are the number one complaint of private equity firms devoted to the Asia-Pacific region, according to a Bain & Co. report last week. Prices hadn’t budged significantly before the outbreak even as economic growth slowed in China, the region’s top destination for such investments. That’s because owners and entrepreneurs have been spoiled for choice: More than 3,000 private equity firms are jostling to find opportunities in Asia.

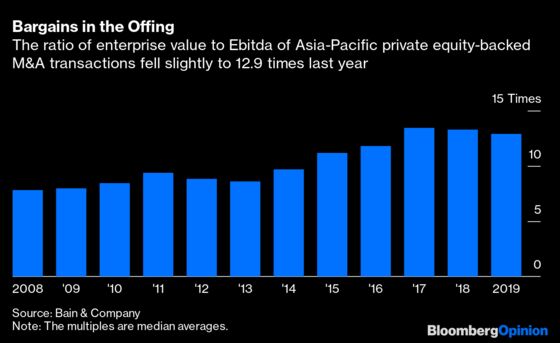

Deal prices eased only slightly last year, to a median ratio of 12.9 times enterprise value to Ebitda, from 13.3 times in 2018. Valuations remain above levels before 2017, according to Bain.

The MSCI Asia-Pacific Index has slumped 23% this year, opening up potential buyout targets in the public markets and dragging valuations of unlisted companies down in its wake. While tightening dollar liquidity threatens the financing that private equity firms need to make deals work, shrinking availability of credit may also weaken the reluctance of startup founders to yield control, which has been a hindrance to transactions, particularly in Southeast Asia.

Another positive from the market shakeout is a possible easing in the pace of activity by Masayoshi Son’s SoftBank Group Corp. That would come as welcome relief to fund executives who see the conglomerate’s $99 billion Vision Fund as pumping up private valuations and crowding out other investors. With SoftBank shares having fallen more than 40% in Tokyo from its February high, Son’s focus has switched to shoring up his own company’s valuation via a $4.8 billion share buyback announced last week. SoftBank is also grappling with challenges at portfolio companies such as WeWork and Indian startup Oyo, as my colleague Tim Culpan has noted.

Not all private equity firms are positioned to profit from the rout. The biggest are in the strongest position. New York-based Warburg Pincus, for instance, raised $4.25 billion for a China-Southeast Asia fund in five months last year, exceeding its target. By contrast, smaller and newer funds spent an average of 22 months on the road and raised only 60% of their goals, according to data from Bain and Preqin.

Baring Private Equity Asia and TPG Capital are examples of other firms with well-known names and track records that have successfully raised multibillion-dollar funds. Blackstone closed a $7.1 billion real estate fund last year that was the biggest ever in that sector. And few would bet against KKR & Co. being able to complete a $12.5 billion fundraising that it started for its fourth Asian buyout fund in November. Meanwhile, sovereign wealth and pension funds started playing safe with their private equity investments a couple of years ago, leaving them with plenty of firepower.

The divergence between strong and weak will widen. Less financially robust private equity firms may struggle to rescue cash-strapped portfolio companies as credit tightens. Even bigger players are likely to reassess previously hot industries or regions. Money has poured into Vietnam and Southeast Asian neighbors on bets that they would benefit as the trade war forced a supply-chain shift out of China. The pandemic has put that thesis in doubt. “People are questioning the whole Southeast Asia-China nexus as a theme,” said Winston Ma, a former executive sovereign wealth fund at China Investment Corp. who’s now an adjunct professor at New York University.

Chinese consumer companies, a magnet for private equity money in the past couple of years, are also likely to suffer a loss of favor. Efforts to curb the coronavirus prompted restaurant chains from McDonald’s Corp. and Yum China Holdings Inc.’s KFC to shut outlets. While giants such as Citic Capital Holdings Ltd. and Carlyle Group LP, which bought most of McDonald’s China business in 2018, can ride out closures, other restaurants may not be so lucky.

Cash alone won’t guarantee success. As long as the pandemic lasts, it will be difficult for private-equity executives to visit potential investments, putting a damper on due diligence and limiting dealmaking. For every great deal made by a cash-rich private equity firm during a financial crisis, there are others that came a cropper. Finding the genuine bargains amid the rubble will be key.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2020 Bloomberg L.P.