Why Go to Paris When You Can Buy Hermes in Hangzhou?

(Bloomberg Opinion) -- Even as China makes its way through a bumpy Covid-19 recovery, the country’s big spenders are splashing out. Luxury brands should pay close attention to where their cash is going. Right now, that’s at home.

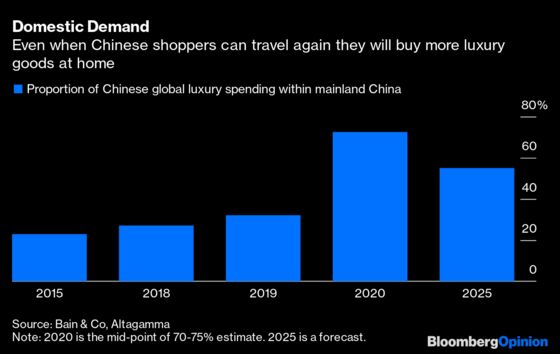

The share of Chinese consumers’ high-end purchases made in mainland China more than doubled from 32% in 2019 to over 70% in 2020, according to Bain & Co. Luxury auto sales were resilient through the latter half of last year. Pricey and ultra-premium alcohol remained in demand. Fine wine prices, driven by Chinese buyers, were up 4% in the last quarter of 2020.

With the government promoting a so-called “dual circulation” policy, to generate demand and supply at home, consumer confidence is likely to stay strong. So even when Chinese shoppers can travel to Paris and Milan again, domestic spending won’t revert to pre-pandemic levels.

This has significant implications for the big luxury brands.

Soaring demand in China means they can get more out of stores that hadn’t been generating good returns. Outlets in cities like Chengdu, where companies may have struggled to drive footfall before the pandemic, are now proving to be useful routes for reaching local consumers.

There may also be room for further investment. Analysts at Jefferies found that just three European fashion and leather goods brands — Louis Vuitton, Gucci and Burberry Group Plc — had locations in each of China’s top 25 luxury cities. Other groups might look into planting their flags or building stores outside of the biggest cities.

But they will need to tread carefully. Despite the boost in China, 2020 was the worst year for luxury in modern history. The major houses may be reluctant to invest in swaths of new outlets. Any outlay must be targeted.

One location where it would make sense to expand is the duty-free hub island of Hainan. Analysts at Bernstein estimate that the number of international luxury brands there has increased by 80% over the last six years. Expect more to follow. Michael Kors-owner Capri Holdings Ltd. said recently that Hainan was “on fire,” while Gucci-owner Kering SA said the region was booming.

The island is supposed to become a free-trade port by 2025. And Beijing has been relaxing rules there to allow greater spending. Last month, China’s finance ministry, along with customs and tax authorities, said that shoppers at offshore duty-free stores could get their products mailed to them. That followed a move in July to raise the limit for duty-free purchases. All of these changes are expected to drive up spending.

In January, duty-free sales on the island totaled 3.7 billion yuan ($571.8 million), down from the previous month but up on the year. Although there were fewer tourists after a busy fourth quarter of 2020, more stores opened and the number of shoppers rose on a monthly basis, according to Goldman Sachs Group Inc.

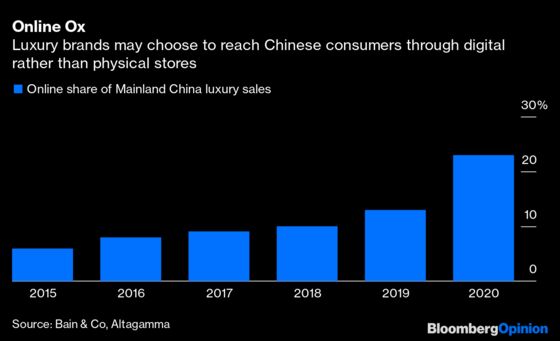

In addition to this offline push, luxury groups will need to boost their online capabilities to reach China’s emerging middle class and Generation Z shoppers. Working with a major online retailer — such as Alibaba Group Holding Ltd.’s Tmall Luxury Pavillion or JD.com Inc. — could be beneficial. Farfetch Ltd. too is pushing further into China after a strategic partnership with Alibaba and Cartier-owner Cie Financiere Richemont SA.

More spending within China is a crucial opportunity for luxury. But it also means fewer Chinese tourists splashing out on Hermes bags in Paris or Burberry trench coats in London.

If glamorous shopping is no longer the prime driver of Chinese travel, European stores will have to adapt — or close. They could move to destinations frequented by local customers, leaving flagship sites to focus less on generating sales and more on offering branded experiences. Ralph Lauren Corp. already has chichi bars inside stores. And Kering said recently that it plans to open more restaurants in its Gucci boutiques around the world.

The shifts will favor the industry’s biggest players: LVMH Moet Hennessy Louis Vuitton SE, Kering and Richemont. They can afford to keep flagship stores open in Europe even if they are taking in less money, while also investing in the best locations in China and in expensive marketing campaigns on WeChat and Douyin featuring top Asian influencers.

But some smaller groups will benefit too. Salvatore Ferragamo SpA and Burberry, for example, have the most Chinese stores, according to Jefferies’ analysis. Elevated domestic spending could bolster their turnaround plans, which, so far, have had mixed results.

The Chinese luxury landscape is changing. Last year, we called it revenge spending. Now it’s clear this is here to stay.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2021 Bloomberg L.P.