(Bloomberg Opinion) -- Who knew there was investor appetite for subordinated Greek bank debt?

Because of the relentless hunt for returns in yield-starved Europe, Piraeus Bank SA, one of Greece’s big four lenders, has been able to brave the European capital markets for the first time since the financial crisis.

Piraeus isn’t opting for senior bonds, and is instead plumping for Tier 2 subordinated debt (which sits midway in the capital structure between top-rated debt and equity-like capital). This means the notes would be fully subject to investor bail-in rules, where bondholders take a financial hit should the bank fail.

While the bank has been bolstering capital by offloading bad loans and selling assets, this issue will help it meet its commitments to the European Central Bank. Last year, the ECB asked the company to raise much as 500 million euros ($560 million) as part of its strategic recovery plan. It’s notable, nonetheless, that the lender has found plenty of takers despite all the well-known risks around the Greek banking system.

Piraeus has raised 400 million euros from the 10-year subordinated security, with an issuer call option after five years. The very high 9.75% coupon was clearly attractive to buyers, but it carries danger signs too. Paying that much interest to bondholders will be a heavy burden for the bank’s business to support.

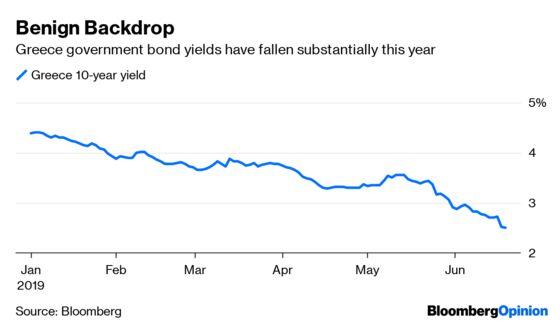

Indeed, this might be a deal too far for wiser investment heads (regardless of all the hedge funds piling in here). Just because government yields are plunging doesn’t mean credit risk is improving; it usually means the opposite. In fairness, this issue is for bank capital specialists only but there’s always a deal that corrects the market’s over-enthusiasm for the diciest assets.

The offer would have been unthinkable a year ago, and comes courtesy of a sustained decline in Greek sovereign yields, with five-year yields falling below their Italian equivalents, and a sixfold rally in Piraeus Bank's share price since February. It helps that imminent national elections are expected to deliver victory to the pro-business New Democracy Party. For Piraeus, it makes sense to strike now and the books were more than twice covered.

Still, a big leap of faith is required to believe that that this ultra-high risk, CCC-rated junk bond will be repaid at that call date in five years time. Investors won’t want a repeat of what happened when Italy’s Banca Monte dei Paschi di Siena SpA issued a similar bond in January 2018. That now trades at close to half its initial value.

Piraeus’s non-performing loans make up more than half of its total lending, despite its offloading of 500 million euros of them to private equity buyers this month. Even after the share price rally, the stock only trades at a price-to-book ratio of less than 0.2. The path to easing the bad debt burden will be arduous.

As part of Piraeus’s strategic plan, the bank sees non-performing loans dropping to about 9% of the total by 2023, which requires the elimination of 21 billion euros of exposure. It has signed an agreement with Intrum AB, a Swedish debt collection specialist, to help manage its bad debt pile. However, the speed at which Greece’s lenders will be able to clean up their loan books is uncertain. The government and the Greek central bank have two separate, not entirely complementary, initiatives to help banks do this but they’re still obtaining European Union approvals.

Piraeus’s plan to improve its fee income by 33% by 2023 looks ambitious too. As the biggest private lender to SMEs in Greece, its growth is tied ultimately to the country’s nascent economic recovery.

A shareholder group that includes the EU-backed Hellenic Financial Stability Fund – as well as John Paulson, Vanguard, Blackrock Inc. and Schroders Plc – offers some reassurance. While success would be another important milestone in Greece’s long road to recovery, you’ll have needed nerves of steel to jump on this one.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.