(Bloomberg Opinion) -- Canceling student loans as a way of getting relief out to Americans who are struggling financially is a hot topic these days as Congress dickers. Speculation is rising that President-elect Joe Biden will issue an executive order to cancel a portion of the $1.7 trillion in student debt outstanding after he takes office in January. One-time forgiveness of these loans would alleviate some hardship now, but it won’t solve the root problem, and it is drawing attention away from other important policies to support students.

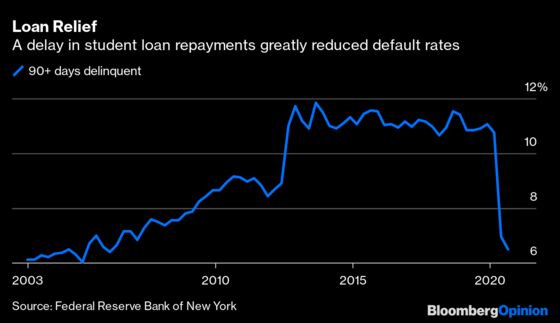

Last year ended with one in 10 loans in default, with much higher rates among some groups such as Black borrowers. Default rates fell by almost half this year as Congress delayed repayments from the start of the pandemic through the end of 2020. But forgiving and forgetting this debt is only a one-time fix. The lasting solution would be to make sure the higher education and training that students get is worth the extra debt, and that their degrees actually lead to better paying jobs.

On its own, debt is neither good nor bad. It depends on the return on the investment. For many students, the bump in income obtained by their education is more than enough to pay back the debt. For others, the investment does not pay off and repayment is a hardship. The government already has policies that would raise the return on an investment in education if pursued more vigorously. Moreover, Biden and could strengthen these programs without Congress. These actions wouldn’t generate headlines like zeroing out hundreds of billions of dollars in loans would, but the payoff for students would add up over the long run.

So, what should Biden do? First, give students better information they can use to decide which school to attend and what to study. The College Scorecard—launched during the Obama administration and a recently expanded by current Education Secretary Betsy DeVos—is a data-driven tool that provides completion rates, salaries after graduation and the costs of everything from certificates to bachelor’s degrees. But numbers aren’t enough; researchers have found that only information about salary after graduation (but not completion rates or cost) had only a small effect on students' choices. More efforts are needed to make the tool more user friendly and provide counseling to teach students and their families how to best use it.

Second, hold schools accountable. The Gainful Employment program attempted to do this by cutting off federal student aid to for-profit degree programs and any certificate programs that leave students with high debt relative to the income they receive after graduating. But the Trump administration rescinded this regulation even though it was working as intended. It should re-instated and expanded.

All educational institutions, not just private for profit schools, must be held accountable. Jordan Matsudaira and Lesley Turner, economics professors Columbia University and Vanderbilt University, find that 77% of public institutions have at least one poorly performing undergraduate program, but in most cases these programs co-exist with many others that benefit students. As a result, it’s tough to know where exactly to draw the line at the institution level. Schools that serve students with less preparation, often from disadvantaged backgrounds, should not be penalized. Cutting off access to education would hurt those students. However, offering programs that do not pay off for students is worse, so oversight must be targeted.

Third, and the least likely to make news, the Biden administration must clean up the servicing of student loans. Analysis by progressive think tank Center for American Progress explains, the system of private servicers is overly complex and the government government struggles to hold them accountable. Servicers do not have sufficient incentives to help students cut their borrowing costs or place them in less onerous repayment plans. Well intended programs are pointless if not administered properly. That was a painful lesson with the problems surrounding mortgage servicers during the financial crisis.

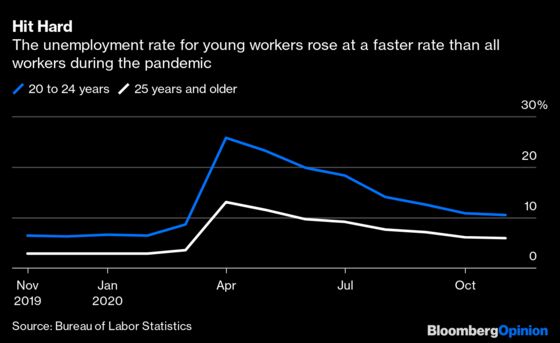

The Biden administration can pursue these three policies on its own, but Congress must do its part by supporting the recovery with vigorous economic relief. Good paying jobs—especially for workers just starting their careers—have taken a hit. The unemployment rate among adults ages 20 to 24 peaked at over 25% in April and remained above 10% last month. Many workers fortunate enough to keep their jobs had their wages cut and promotions put on hold. Less income means more hardship.

The vaccine is on the way, but bills are piling up and the careers of young workers are in jeopardy of falling off the rails before they start. For now, the forbearance on student loans must be extended into 2021 and a plan must be devised to allow borrowers to make up missed payments gradually. But the programs are there for lawmakers to ensure that higher education and training pays off for everyone.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Claudia Sahm is a former Federal Reserve economist and creator of the Sahm rule, a recession indicator.

©2020 Bloomberg L.P.