(Bloomberg Opinion) -- In my first column this year, I picked on fixed-income exchanged-traded funds, arguing that without the Federal Reserve’s unprecedented intervention in corporate credit markets, it’s unclear whether these relatively new vehicles for investing in bonds would have survived the liquidity crunch of March 2020.

Unsurprisingly, this didn’t sit well among those in the $5.5 trillion ETF industry. After getting an earful from several ETF defenders, I’m now convinced that talk of an “illiquidity doom loop” in ETFs was misplaced and that the Fed stealthily came to the rescue of the more entrenched fixed-income portion of the $18.2 trillion mutual-fund industry. And I’ll go one step farther: The lessons learned from the coronavirus crisis will accelerate the rise of ETFs and diminish mutual funds even faster than previously anticipated.

Just consider the stark difference in fund flows. ETFs took in a record $502 billion in 2020, according to Morningstar Inc. data, while investors pulled $289 billion from open-end mutual funds, easily breaking 2018’s record of $169 billion. It’s the fourth year in the past six that the funds have lost money. “But it is too soon to count out mutual funds as an investment vehicle,” Morningstar analysts Tony Thomas and Supreet Grewal wrote in a report.

That’s true when looking at the next year, or five years, or probably 10 years. Mutual-fund management is a massive business, with vast amounts of passive money flowing in each year through 401(k) retirement plans. ETFs haven’t caught on as an alternative for a number of reasons, ranging from their tax treatment to bureaucratic inertia. Mutual funds won’t suddenly disappear — but the point at which they lose their asset advantage to ETFs is fairly close at hand.

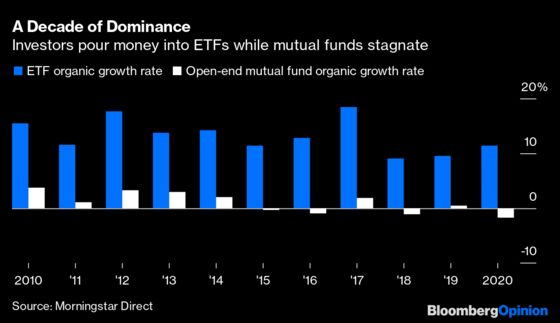

The best way to show this is the “organic growth rate” of U.S. ETFs and open-end mutual funds. This metric, in effect, reflects the annual growth of the two investment vehicles if the price of every stock, bond and other financial asset were unchanged from the previous year. It strips out the built-in asset advantage enjoyed by mutual funds that’s behind the almost $2 trillion increase in their total assets in 2020, even amid record outflows.

There’s simply no contest — and it hasn’t been close for quite some time.

Given the frenetic trading in shares of GameStop Corp. and other “meme stocks,” it might be tempting to conclude that the rise of no-fee trading for ETFs (but not mutual funds) among Robinhood and other discount brokerages is responsible for the disparity. That’s certainly part of it. ETFs can trade at any point when equity markets are open; open-end mutual fund shares don’t trade on an exchange. ETFs have no minimum investment, and some brokers even allow purchases of fractional shares; many mutual funds require thousands of dollars to invest.

The knock on ETFs, captured by the “illiquidity doom loop” phrase, is that their convenience would come at a steep cost during periods of market stress, especially for funds that own illiquid investments. This, of course, is precisely what happened in March 2020. At one point, about 70 fixed-income ETFs traded with at least a 5% discount to their net asset value, and 16 traded at a discount of 10% or greater. Many of them were marketed as tracking a benchmark.

That certainly sounds like a bad thing. But there’s reason to think this is actually a safer structure than mutual funds, even if the price shocks can seem extreme.

Open-end mutual funds price daily at their net asset value, or NAV. For equity funds, this is straightforward, given that stocks trade on an exchange and there’s a centralized accepted price. This is not as easy for fixed-income funds because many bonds will go days or even weeks without trading. Morningstar analysts attempted to quantify just how subjective corporate-bond pricing can be and found that March 2020 took this guesswork to new heights, “with large groups of bonds showing price-spread percentages in ranges of between four and nine percentage points and still numerous outliers pricing even wider than that.”

This kind of pricing, in effect, worked to mask the underlying volatility in the portfolio — exactly the type of wild swings that were on full display in ETFs. The huge discounts to NAV for some fixed-income ETFs most likely better reflected the true demand in the market, given that the ETFs actually changed hands at an agreed upon price, unlike the majority of bonds. This couldn’t last forever; eventually fixed-income mutual funds would have to reflect the market in their share prices.

Which brings us back to the Fed. On March 23, it unveiled the Primary Market Corporate Credit Facility and Secondary Market Corporate Credit Facility, among others, which immediately thawed the bond market and marked the bottom of the rout in stocks and other risky assets. Within days, fixed-income ETFs went from trading at steep discounts to changing hands at a premium. ETFs, it seemed, were saved.

But ETFs could have theoretically survived for weeks or months while trading below their NAV. This happens all the time among closed-end funds, after all. Open-end mutual funds, on the other hand, are entirely at the mercy of flows. If they’re hit with a sudden wave of redemptions, they have no choice but to sell some of their assets into the open market to raise cash — even if that market is almost entirely broken.

That kind of worst-case scenario for mutual funds happened in the run-up to the Fed’s credit intervention. In the week ended March 18, investors pulled a record $35.6 billion from U.S. investment-grade bond funds, a record $12.2 billion from muni mutual funds, $2.91 billion from high-yield funds and $3.45 billion from those tracking leveraged loans.

If the Fed didn’t step in, I’m confident this vicious cycle would have lasted for weeks, if not months, and might have either taken out some mutual funds or at least forced some to halt redemptions. Again, this comes back to the structure. If you know a fund manager will need to sell assets to raise cash and anticipate they’ll shed their highest-quality, most-liquid bonds to do so, thereby causing the value of the fund to sink, then there’s a clear advantage to being the first one out the door. Of course, investors could also stampede out of ETFs, but rather than having to immediately sell bonds at rock-bottom prices, ETFs can just trade at a discount that will probably self-correct eventually.

Two years ago, my Bloomberg Opinion colleague Barry Ritholtz interviewed Matt Hougan, former chief executive officer of Inside ETFs, for his Masters in Business podcast. “If the ETF came first, the SEC would never approve the mutual fund structure,” Hougan argued. “The only bond funds that have blown up have been bond mutual funds because they have to redeem out in cash … people worry about bond ETFs blowing up. What they should be worried about is in a bond-market crisis, corporate-bond mutual funds blowing up and having real issues.” That nearly turned out to be prophetic.

The final nail in the coffin for mutual funds might be the Cathie Wood phenomenon. For years, ETFs have been more or less synonymous with low-cost indexing while star investors stuck to mutual funds. Wood, founder of Ark Investment Management, changed all that with actively managed strategies focused on buzzwords like “innovation” and “next generation.” People are clearly willing to pay for performance — ETFs with expense ratios of 61 to 80 basis points had their best month ever in January, taking in about $16 billion, according to Eric Balchunas at Bloomberg Intelligence. That wasn’t far off from inflows into ETFs that charge 10 basis points or less. Now active ETFs are popping up everywhere, even in mutual-fund dominant industries like municipal bonds.

With pressure coming from all sides, it’s hardly surprising that the asset-manager arms race is heating up. But this consolidation is more about bulking up for survival than a bet on a mutual-fund revival. The biggest prize out there is State Street Global Advisors, in no small part because its more than $3 trillion under management includes a suite of ETFs that account for about 16% of U.S. market share.

Put it all together, and it’s at least worth contemplating a market without mutual funds within many of our lifetimes. Again, there are deeply rooted structural reasons why this won’t happen overnight. But a decade of treading water as markets raced to new highs portends a difficult future. It’s an ETF world now.

It's worth noting that Collective Investment Trusts (CITs) have made inroads in displacing mutual funds in some 401(k) plans in recent years. CITs are offered only to certain qualified retirement plans, are not regulated by the SEC and tend to invest with a tax-exempt strategy in mind.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.