Diversifying Your Portfolio Isn't Zesty, But It Works

(Bloomberg Opinion) -- When the story of this era in financial markets is written, it will be said that many investors were overtaken with fanciful notions of money growing to the moon, leading them to make costly mistakes that could have been avoided with simple steps to safeguard and grow their savings. But this era is not over yet, and it’s not too late to get on the smart side of history.

The idea of growing money gradually but reliably with a diversified portfolio is becoming frighteningly passe. Billionaire investor Mark Cuban may have kicked off the trend a decade ago when he declared that “diversification is for idiots.” A parade of highflying investments has reinforced the message in recent years, conditioning investors to believe that big, concentrated bets are a quick and reliable way to get rich. Bitcoin, for instance, is up more than 10 times since crashing in 2018. Shares of electric carmaker Tesla Inc. surged more than 10 times in just more than a year from 2019 to 2020. Meme stocks GameStop Corp. and AMC Entertainment Holdings Inc. have risen well above 10 times this year.

It seems a lot of investors are looking for a 10X these days. One company, an online commercial real estate exchange with a regular rotation of off-peak television ads, has even named itself Ten-X, never mind that the tag bears no discernible relationship to its business. It should go without saying that expecting money to multiply that quickly is laughable. Investors would be fortunate to grow their money at 7% or 8% a year over an investing lifetime, which is as much long-term growth as the average professionally managed endowment can hope for. And at that rate, it takes 30 to 35 years for money to grow 10 times.

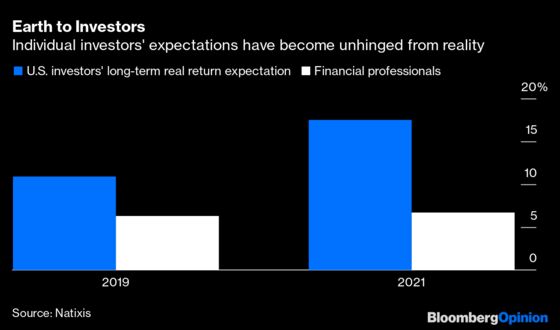

Expectations about what a diversified portfolio can achieve have also become silly. In its latest survey of individual investors, French lender Natixis SA reported that U.S. investors expect their portfolios to generate a long-term return of 17.5% a year after inflation, a big jump from the already unrealistic 10.9% they expected in Natixis’s 2019 survey. With the possible exception of early stage venture capital, I’m not aware of a single asset class that has produced a long-term return that high.

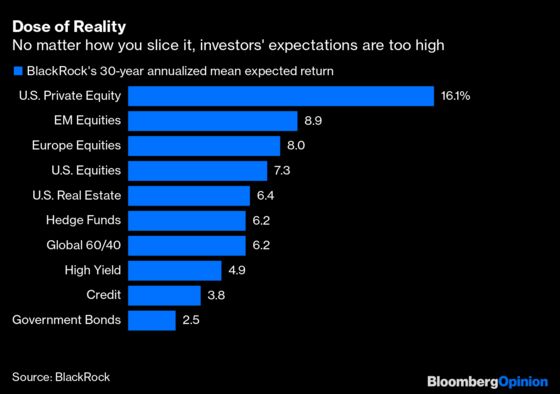

And there’s no reason to believe the future will be different. But don’t take my word for it. BlackRock Inc., the biggest money manager on the planet, publishes its expected returns for a wide variety of investments and over multiple periods. Its highest mean expected return over the next 30 years, the longest period it considers, is about 16% a year from leveraged buyouts. Every other asset class has an expected return of less than 10% a year, and roughly half are less than 5%. Good luck constructing a portfolio that produces a 17.5% return after inflation.

The results are likely to be even more modest in the medium term because many assets are expensive, and elevated valuations are often a drag on future returns. So it’s not surprising that BlackRock estimates even lower returns for most asset classes over the next five or 10 years. On the brighter side, as BlackRock’s estimates show, investors can enhance their expected returns by increasing their exposure to non-U.S. stocks, which are less popular than U.S. stocks and therefore more reasonably priced. Even so, the most investors can expect is still somewhere in the range of 7% to 8% a year, or 5% to 6% after inflation, if the bond market’s inflation forecast of roughly 2% a year can be trusted.

Magical thinking may even be penetrating index investing. Since 2016, most of the money invested in exchange-traded funds, which overwhelmingly track indexes, has gone to U.S. large-cap funds. Investors have handed $1.7 trillion to U.S. stock ETFs and just $440 billion to foreign ones, according to Bloomberg Intelligence, most of it going to large caps. It’s probably not a coincidence that the six stocks that dominate the S&P 500 Index and account for a quarter of its weighting — Apple Inc., Microsoft Corp., Amazon.com Inc., Facebook Inc., Alphabet Inc. and Tesla Inc. — have averaged a total return of 41% a year over the past five years. Their size and success have made U.S. large caps the best performing major asset class in public markets in recent years. Now U.S. large caps are also the most expensive, which is probably why BlackRock sees them generating just 6% a year over the next five years.

None of this is new, of course. Investors tend to get carried away during periods of technological innovation, and this is undoubtedly one. Some of the excitement is warranted, as it always is. But like earlier periods, there will be many more losers than winners and it’s nearly impossible to tell them apart in advance, which makes big, concentrated bets a dicey game. Marc Andreessen, one of the most successful venture investors ever, has spent an entire career navigating a minefield of startups where the failure rate may be as high as 75%. His advice to ordinary investors? “Put it in an S&P 500 Index Fund. Don’t get fancy.”

There’s little harm setting aside some play money to chase the next 10X. The real danger is that investors will gamble away their future in the misguided belief that profits earned over a lifetime of disciplined investing can be achieved overnight. The smarter path is as boring as it is obvious: Invest in a diversified portfolio of low-cost funds — and try to remember that money doesn’t fly, it crawls.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2021 Bloomberg L.P.