Contrarian Investors Should Love Emerging Markets

(Bloomberg Opinion) -- Emerging markets get no respect. They account for about two-fifths of global gross domestic product and a quarter of global stocks by market value, and yet they’re a fraction of most U.S. investors’ stock portfolios. If there’s ever a time to give emerging markets another look, this is it.

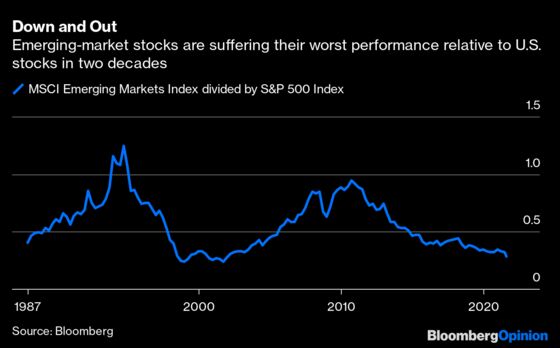

That’s because emerging-market stocks are lagging behind those in the U.S. by the biggest margin in two decades. The last time they were beaten this badly was when a wave of crises in developing countries slammed their stock markets during the late 1990s while dot-com mania lifted U.S. stocks to historic heights.

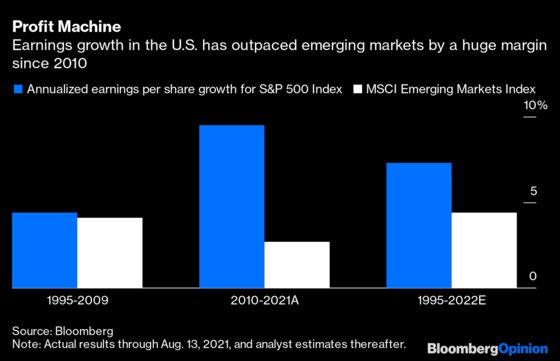

This time it’s about profits. U.S. companies have increased earnings at a record rate in recent years while earnings growth in emerging markets has barely budged. Since 2010, earnings per share for the S&P 500 Index has grown 9.5% a year, compared with just 2.7% for the MSCI Emerging Markets Index. It wasn’t always this way. From 1995 to 2009, the first year for which numbers are available for emerging markets, earnings grew at roughly the same pace in developing countries as in the U.S., about 4% a year.

Given the sharp divergence in earnings growth since 2010, the U.S. may seem like the better place to invest, even when all available earnings numbers are considered. Earnings growth, after all, is a key component of stock returns, and the U.S. is producing more of it. Assuming analysts’ estimates for this year and next are reliable, the S&P 500 will have grown earnings 7.3% a year from 1995 to 2022, compared with just 4.4% a year for emerging markets. If U.S. companies were to maintain that lead, all else equal, expected returns would be 2.9 percentage points a year higher in the U.S. than in emerging markets.

But earnings growth isn’t the only driver of stock returns. Dividends and valuations play a role, too. When all three variables are considered, emerging markets appear to be the better bet. Analysts expect a dividend yield of 3% from emerging markets, compared with 1.5% for the S&P 500. When combined with earnings growth, the advantage for U.S. stocks shrinks to 1.4 percentage points a year.

Stocks are also much cheaper in emerging markets. They trade at 12 times next year’s earnings, whereas the comparable price-to-earnings ratio for the S&P 500 is 20 times. That valuation gap tips the scale in favor of emerging markets. One way to compare price to expected payoff is to take a ratio of P/E to the sum of expected earnings growth and dividend yield (the lower the ratio the better). Based on the previous numbers, that ratio is 1.7 for emerging markets and 2.3 for the S&P 500.

And that may be the best case for U.S. stocks because it assumes U.S. companies will continue generating higher earnings growth and commanding much higher valuations than those in emerging markets, both questionable assumptions. It’s not obvious why earnings growth should be higher in the U.S. Investment in research and development, for instance, has been shown to boost growth, and emerging-market companies spend as much on R&D as a percentage of sales as companies in the U.S. In fact, they may soon spend more, as R&D investment in emerging markets has grown at more than three times the U.S. rate since 1995.

If anything, it’s more likely that earnings growth in emerging markets will outpace the U.S. in the years ahead. Developing economies are growing faster than the U.S., a tailwind for their companies, particularly as they grab market share in their countries from American companies. Also, given that recent earnings growth has been unusually high in the U.S. and strangely low in emerging markets, the roles may reverse for a while, bringing earnings growth between them closer to parity.

The valuation gap between emerging markets and the U.S. could also narrow. The U.S. is rightly perceived as the safer place to invest, so it makes sense that investors are willing to pay more for U.S. companies. But how much more? The difference in P/E ratio based on forward earnings has averaged 4.7 times since 2005, the longest period for which numbers are available, and has rarely been as wide as it is today. If the gap were to close, it would be another boost for emerging markets relative to the U.S.

All of that may explain why the consensus among big money managers is that emerging markets will deliver higher returns than the U.S. in coming years. Value stocks in emerging markets may perform even better. With a price tag of just 9 times forward earnings, they could credibly be called the most despised stocks on the planet.

Contrarian investors have taken note. Boston based money manager GMO estimates that emerging-market value stocks will return 3.2% a year after inflation over the next seven years, compared with a negative 8.2% a year for U.S. stocks. Rob Arnott, founder of index provider Research Affiliates, has said that half of his liquid investments are invested in value stocks from developing countries.

It’s worth noting that the last time emerging market stocks performed this badly relative to the U.S., they went on to beat the S&P 500 by 14 percentage points a year from 2000 to 2007, and value stocks won by 15 percentage points a year. They did it by paying a higher dividend yield than U.S. stocks, generating nearly four times the earnings growth as U.S. companies and expanding their valuations while that of the S&P 500 was cut by more than a third.

I’m not suggesting investors replace their U.S. stocks with ones in emerging markets. But developing countries now account for about 12% of the MSCI All Country World Index, a widely followed gauge of the global stock market. Stock portfolios that allocate less than that to emerging markets should ask why — and it won’t be easy to answer.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2021 Bloomberg L.P.