(Bloomberg Opinion) -- Billionaire investor Bill Ackman, founder of hedge fund Pershing Square Holdings Ltd., is reloading on his bearish bet on corporate credit, according to the Financial Times. That makes sense.

Credit spreads — the premium charged for riskier company bonds above government debt — have largely returned to pre-Covid levels, even before a working vaccine has passed approval. In some cases they’re at record lows amid the euphoria on the Pfizer vaccine. As the recovery becomes increasingly priced in, why not hedge for potential bumps in the road?

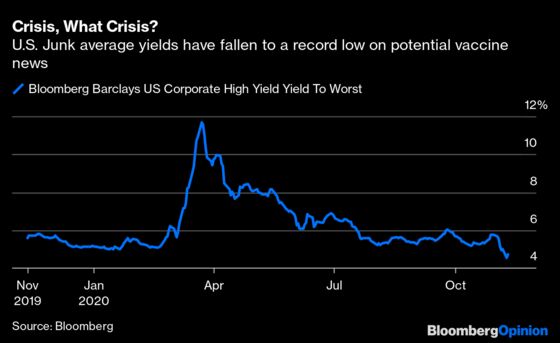

It helps for Ackman that he’s reloading after a major win: His fund banked $2.6 billion after taking exposure in March to credit default swap indexes — a form of insurance — on $70 billion or so of corporate debt. That paid off as the spread spiked (see chart below) during the first wave of lockdowns; Pershing exited the trade at the right time and rotated into stocks.

His exposure this time is less than a third of the size of the March bet, but the pricing levels are similar. According to Ackman, “The same bet is available on the same terms as if there had never been a fire.”

The risk-to-reward ratio looks promising given where credit spreads are again, although he appears relatively optimistic about the prospects for the economy and the stock markets. This wager looks more like a prudent hedge against the fund’s equity exposure than the home run of earlier in the year. “I hope we lose money on this next hedge,” he says.

What has changed since March is the coordinated monetary and fiscal stimulus around the world, which goes way beyond even the financial crisis. The next few months will be challenging, nonetheless, and could even led to complacency on virus risks.

Will government and central bank appetite for endless support persist if a vaccine is delivered? The most perilous time for corporates might be their reemergence into a post-virus world without the same financial backing.

The banking sector is alive to these risks. Jennifer Piepszak, chief financial officer of JPMorgan Chase & Co, said on its quarterly earnings call that she expected to see corporate delinquencies tick up in early 2021 and write-offs later in the year. The U.S. lender isn’t assuming further stimulus after the end of this year and will assess its reserves for loan losses accordingly.

Central bankers are also evaluating what type of economy emerges in 2021 with or without a medical resolution. Klaas Knot, governor of the Dutch central bank, said this week that the European Central Bank is facing “a major call” at its next policy meeting Dec. 10. The second wave of the virus in Europe has wiped out any expectations of growth in the fourth quarter. As loan forbearance and guarantees taper off, Knot remarked that we will get to see who is swimming naked. Central bank bond-buying has only dipped a toe into corporates below investment grade, so riskier high-yield companies will feel the pressure most.

Policy makers have been dynamic in their financial response to Covid but there can be no assurance this will persist. The calm after the storm is when the reckoning really comes, and credit spreads are priced too close to perfection. It’s a smart move to hedge your bets.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.