(Bloomberg Opinion) -- Why do tech firms seem to delight in making things tougher for themselves?

TeamViewer is planning a Frankfurt initial public offering by the year-end that may value the German maker of remote computer access systems at between 4 billion euros ($4.4 billion) and 5 billion euros. The proceeds will go into the pocket of private equity firm Permira Holdings LLP, its owner of five years.

With the company growing at a ripping pace – 37% so far this year – and boasting healthy profitability, it should be an attractive proposition for investors. But I’m equivocating for a reason. The problem lies in the metrics it provides. Rather than talking simply about revenue and profit, in a Wednesday press release it proffered “billings” and “cash Ebitda”. The former totaled 142 million euros ($158 million) in the first half, while the latter hit 74 million euros.

Billings is a fairly common measure in cloud computing. Cash Ebitda, less so. Ostensibly, both are intended to give a clearer representation of the company’s earnings by ensuring that only business from a particular time-frame is booked in that period.

That has something to do with the fact that TeamViewer switched its business model in the middle of last year, moving from selling licenses to subscriptions. The problem is that neither earnings metric is well defined, or indeed defined at all, at least so far. So while it appears that the company is performing strongly, investors will need to review the IPO prospectus carefully when it surfaces.

Technology companies have an unhappy penchant for non-GAAP or -IFRS metric, many of which make “cash Ebitda” look pretty straightforward. Uber Technologies Inc. discloses “core platform contribution profit”. Lyft talks about “take rate”. Twitter has simply “adjusted earnings”. There’s good reason to be cautious: shares all three of those companies have struggled to exceed the price at which they were first sold to the public. Investors have been burned by software firms with opaque metrics before.

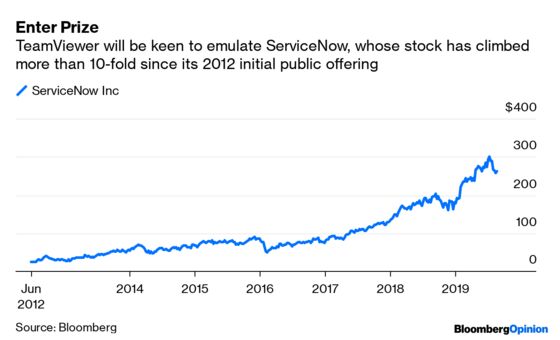

The most pertinent point of comparison is ServiceNow Inc. Like TeamViewer, it has a subscription-based offering which targets a discrete slice of the enterprise – in the U.S. firm’s case, company help-desks – and leans on non-GAAP subscription billings as a metric. Its enterprise value of some $49 billion is equivalent to about 13 times 2019 billings.

Based on the midpoint of its reported valuation range, TeamViewer will have an enterprise value of roughly 17 times its anticipated billings. It may be able to justify that higher valuation on the basis that it’s already more profitable than ServiceNow. But we won’t know for sure until we have more exhaustive earnings numbers.

TeamViewer looks like a promising business. It will need to do more to prove it.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.