(Bloomberg Opinion) -- Of all the problems an upstart company can have, Peloton Interactive Inc. has a relatively good one: It can’t meet booming demand for its home-fitness products.

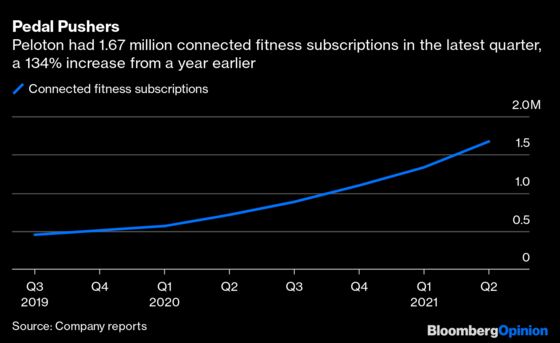

In releasing its latest earnings on Thursday, Peloton said it would shell out an incremental $100 million on air freight and expedited ocean freight as part of steps to speed up the time between the placement of an order and its delivery, which has elongated since the pandemic. So even as the company reported explosive growth in revenue and subscriptions and bumped up its full-year guidance for those figures, it lowered its full-year estimates for gross margin. That gloomier margin outlook dragged down its shares some 8% in after-hours trading.

This is a weird reason for the Peloton faithful to get skittish. Presumably, the stock has been pumped up nearly 700% since mid-March because of a belief that the pandemic has expanded the long-term addressable market for at-home workouts. Shouldn’t investors brush off the near-term hit to gross margin in exchange for grabbing customers that can be locked into the Peloton ecosystem as paying subscribers for years to come?

It's possible investor reaction reflects a sense that the production delays mean Peloton is squandering a crucial moment before vaccines are widely distributed to win over homebound consumers. That is more understandable. Analysts at Oppenheimer & Co. estimated in a January research note that the pandemic has led to about 4.4 million gym membership cancellations and that Peloton has snared 12.6% of those “free agents” whose fitness dollars were up for grabs. That’s a meaningful achievement, and this window of opportunity won’t stay wide open forever. But the raised sales guidance suggests Peloton continues to make inroads despite the supply crunch. It is right to move quickly to make the most of this singular moment, not only with this planned logistics spending but also its recently announced agreement to acquire Precor, which gives it U.S.-based manufacturing capacity.

There are reasons to be skeptical about Peloton. There’s a legitimate risk investors are overestimating how much the pandemic has changed its long-term prospects. Many people will want to return to gyms and fitness studios when it is safe to do so.

More broadly, Peloton is sometimes compared to Netflix Inc. because both are innovative subscription models that bring an on-demand service into the home. But Netflix relies on a TV and Wi-Fi that consumers likely already have. Peloton requires making space in your home for a hulking 135-pound, or even 430-pound, machine. Its constraints for adoption are simply different.

Speaking of the Netflix comparison, the aforementioned Oppenheimer research note includes a table of financial data of “comparable companies” that includes the streaming giant as well as Roku Inc., Match Group Inc., Spotify Technology SA and Wix.com. In each case, I understand the parallels and see how they are instructive, but all of those companies also have significant contrasts with Peloton. That underscores an important point: One reason Peloton shares have flown so high in the last year is that its unique model makes it difficult to benchmark them against anything else, especially for retail investors looking for shiny objects of the stay-at-home moment.

None of this is a knock on how Peloton executives are running their business. As I’ve noted before, the company is wise to branch away from bikes into treadmills, which have a larger potential audience. It has made smart use of its app – a subscription-based suite of workouts that can be done without its bikes or treadmills – as a marketing funnel for its flagship products. Its churn rates have been compared to those of utility companies, a commendable testament to customer satisfaction.

But there’s no denying its impressive recent performance has been achieved with the help of tailwinds that are going to fade. And the company’s valuation was already quite rich before Thursday’s business update. There a plenty of reasons to be cautious about Peloton. However, the gross margin pressure resulting from its attempts to improve customer service is not one of them.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2021 Bloomberg L.P.