Sorry, Percy Pig, Even Ocado Can’t Save Marks & Spencer

(Bloomberg Opinion) -- You might have thought the pandemic-driven surge in online shopping would have made investors wake up to the value of Marks & Spencer Group Plc’s partnership with digital supermarket Ocado Group Plc. But 18 months on from the tie-up, the British retail giant’s share price is still close to record lows.

On Wednesday, M&S said its share of the joint venture’s post-tax profit was 38.8 million pounds ($50.3 million).

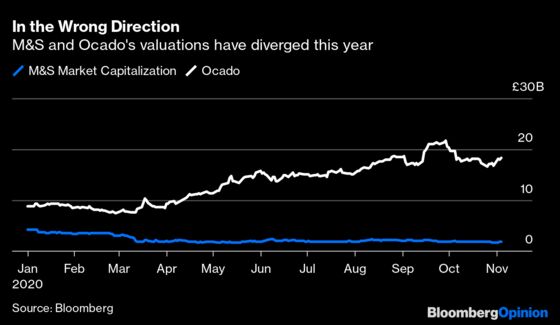

But that doesn’t seem to be reflected in the valuation of M&S, best known for its Percy Pig sweets, ready meals and underwear. Although its shares rose as much as 7% in early trading on Wednesday, its market capitalization has halved from about 4.2 billion pounds at the start of this year to about 1.9 billion pounds as of Nov. 4.

Meanwhile, Ocado’s valuation has doubled, from about 9 billion pounds at the start of the year to 18 billion pounds. On Monday it upgraded its profit forecasts for the current financial year, thanks to soaring demand for online groceries — now largely supplied by M&S.

There are a couple of reasons for this puzzling divergence between M&S and Ocado.

First, the joint venture only includes Ocado Retail, which plucks groceries from its warehouses and drops them off at U.K. customers’ doors. That’s a booming business right now, but it’s not what investors get excited about. They prefer Ocado Solutions, the online grocer’s technology arm, which has struck deals with retailers around the world, including the Kroger Co. in the U.S. and France’s Casino Guichard-Perrachon SA, to run their web operations.

Second, M&S’s food sales online may be less profitable than those from stores. In the year to March 28, 2020, M&S made an operating margin from its food business of 3.9%. In the seven months to March 1, 2020, Ocado Retail made an operating margin of 1.1%. Although this jumped to 8.6% in the six months to Aug. 26, that was due to the pandemic surge in online food purchases and an exceptional gain at Ocado Retail. M&S might not be able to count on those benefits in more normal times.

Despite these drawbacks, the British High Street stalwart deserves more credit. At least by getting into bed with with Ocado, it can defend its existing food business from rivals that had already built powerful digital capabilities. Who knows how bad things would be without the ability to sell food online, particularly as England faces another lockdown. In the U.K., the proportion of food purchased via the internet has almost doubled in the pandemic and is set to pick up further in the months running up to Christmas — traditionally a busy period for M&S’s party food and prosecco.

And M&S’s chairman, retail veteran Archie Norman, may be able to unlock more value from the Ocado partnership in the future.

Adding an online capability enables M&S to one day spin off its food arm into a separately listed company. This group would combine a quality grocer with a best-in-class online delivery service — quite a compelling proposition for investors.

According to analysts at Barclays, based on estimates for the year to March 2023, valuing each part of M&S separately could deliver total equity of 2.7 billion pounds, well ahead of its current market capitalization.

The tricky part of this kind of breakup would be what to do with its sluggish clothing and home furnishings business, which was struggling even before the pandemic. The fashion division might shrink naturally as the food unit grows, it could combine with another clothing retailer, or it could be reinvigorated as a smaller, nimbler company once free from its corporate parent.

But if M&S’s fortunes are increasingly driven by food — sold both digitally and physically — Ocado’s robots might still be able to ride to Percy Pig’s rescue.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.