(Bloomberg Opinion) -- Saudi Aramco’s no-doubt-hefty IPO prospectus isn’t due out for several days yet. But OPEC’s own annual tome, the World Oil Outlook, dropped Tuesday — and it reads like an essential preamble.

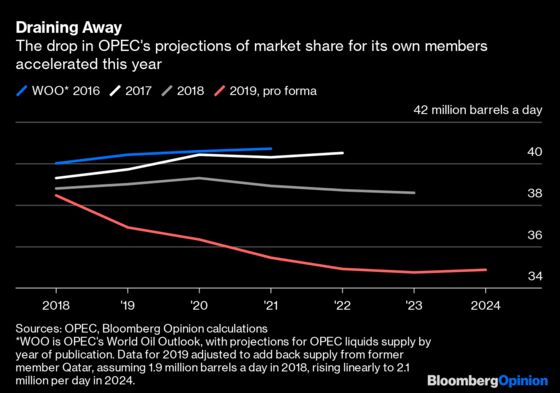

The oil exporters’ club remains optimistic about long-term prospects for its favorite fuel and its own fortunes. The medium-term outlook borders on despair. Total liquids supply from the group — including crude oil, natural gas liquids and others — is expected to fall by 2.2 million barrels a day through 2023, to just 32.7 million barrels a day. Comparisons with previous estimates are complicated by Qatar having left OPEC this year. Still, even adjusting for that, this year’s projection for OPEC’s output in 2023 is about 3.9 million million barrels below what was anticipated this time last year, equivalent to wiping out the United Arab Emirates’ current production. This accelerates a trend in OPEC’s estimates for its own supply in recent years.

These numbers mask a deeper problem. It is notable that OPEC hasn’t broken out its projections for production into its constituent parts this year, as it did last year. Instead of separate lines for crude oil, NGLs and other liquids, we just get a “total OPEC liquids” number. Still, using last year’s figures and assuming all of Qatar’s growth will come in the form of non-crude oil, the latest projections imply OPEC’s higher-value crude oil production dropping by roughly another 2 million barrels a day by 2024.

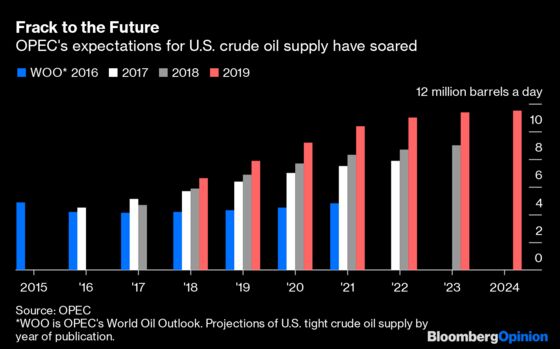

The culprits are — what else? — lower expected demand and, especially, strong growth in non-OPEC supply, particularly from U.S. tight oil. Crude oil production from U.S. shale is now expected to rise above 10 million barrels a day in 2021. OPEC’s forecast was less than half that just three years ago.

This is why shares in Saudi Arabian Oil Co. are being pitched more like medium-term bonds than equity. As the timetable for Aramco’s IPO has sped up, its state owner has announced one inducement after another, designed around one big marketing point: Your dividend is safe through the early 2020s, come what may (see this, this and this).

Getting Aramco’s valuation anywhere close to even the reportedly adjusted range of around $1.6 trillion to $1.8 trillion requires an oil price assumption of at least $70 a barrel and a dividend yield not much higher than 5% — and that assumes crude oil production averaging 11 million barrels a day (you can see the assumptions I use in more detail here).

There is a distinctly rose-tinged hue to those assumptions already, and OPEC’s latest medium-term projections turn them positively pink. If OPEC’s market share is set to drop from 35% today to 31% by 2024, then the burden of supply cuts will tend to fall heaviest on its de facto leader — just as it does today. And using my assumptions, every half-million-barrel-a-day change in production shifts Aramco’s annual free cash flow by about $5 billion; every $5 move in the oil price changes it by $8.5 billion, below $70 a barrel.

OPEC may be wrong about the future, of course; perhaps it’s overestimating the frackers today just as it underestimated them in years past. For Saudi Arabia, however, this is irrelevant. Selling equity is an exercise in stoking optimism and soothing any concerns. The mere chance that the global oil market ends up looking like OPEC’s vision for the next five years is reason enough for Aramco to literally throw money at the issue.

Qatar produced about 1.9 million barrels a day (including non-crude oil) in 2018 and OPEC expects that to reach almost 2.1 million a day by 2024. Adding the latter figure to OPEC's projected total supply in 2023 results in a pro-forma figure of 34.8 million barrels a day, which is about 3.8 million barrels a day below the projection given in last year's World Oil Outlook, before Qatar left the group.

The recently announced change in royalty rates mean the impact is reduced when oil is above $70 a barrel and especially above $100.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.